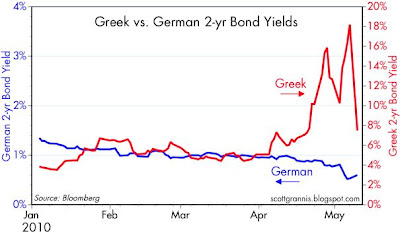

This collection of charts covers the range of the market's response to the emergence of the Greek crisis and its apparent resolution that came today in the form of a nearly $1 trillion bailout of Greece. Equity markets worldwide today rallied sharply, while the implied volatility of equity options fell significantly; the world breathed a huge sigh of relief as fear of another banking crisis subsided. Greek government bond yields fell hugely as the threat of a default faded, while German yields rose marginally as its value as a safe-haven was marginally diminished; Greece may be much less likely to default, but Germany has now taken on a significant new contingent liability by backstopping the Greek government. Greek CDS fell by 355 bps, but remain at levels that equate the risk of its bonds to that of junk bonds; investors are feeling much better, but they are far from being completely reassured that we've seen the end of the Greek problem. U.S. credit spreads fell, and are now only slightly wider year to date; Greece is unlikely to pose a significant problem to the U.S. economy. Currencies, curiously, were largely unchanged today; this may reflect the fact that the market had effectively discounted the likelihood that the ECB will eventually be forced to monetize some portion of Europe's added debt burden.

The way I see it, the bailout is equivalent to spreading the prospective losses to Greek creditors among a handful or so of major developed countries and the IMF (the U.S. is sharing in this because it supplies about 40% of the funding of the IMF's share of the bailout). Creditors with excellent reputations have tarnished that reputation somewhat because they are now on the hook for a portion of potential Greek losses, should they occur. Presumably, countries like Germany were persuaded to do this to themselves to avoid the potential fallout—in the form of bank failures—from a Greek default.

Whatever the case, the world's investors last week were feeling very uncomfortable holding Greek debt, and now the bailer-outers of Greece have effectively said they are willing to shoulder a significant portion of the default risk of Greek debt. The world is somewhat relieved because a festering source of systemic risk has been effectively socialized. It's similar to what we did in the U.S. with the housing market crash: e.g., the gargantuan losses of Freddie and Fannie became losses that will be born by U.S. taxpayers. This sounds a lot like "spreading the

The bailout of Greece doesn't eliminate the risk that Greece will fail to put its fiscal house in order, but it does place much greater political pressure on Greece to do so. Meanwhile it shifts the burden of the risk to other major players and buys everyone some time; if world economies continue to recover, there's a decent chance that growth will reduce government deficits.

So while this is not an optimal state of affairs, it is most likely better than what we had before.

14 comments:

The Total Put/Call Ratio 5 day

Moving Average is now 1.08...this

is three standard deviations from

the mean over the last year....the mean for the past year has been .86

Brodero,

It appears this is showing there is still a high level on anxiety among investors, which is also reflected in the vix. I think it is a good indicator to keep an eye on. Thanks for showing it.

Scott,

Another good post. Something else that will help Europe is a lower Euro. I still think it drifts slowly toward 1.15 to the $ over the next several months. The sovereign bond panic is over...for now. As long as the central banks are a threat to buy them the speculators can't get any traction. Also, Europe's banks are granted a reprieve (as are many of ours..C and JPM are two with more than a little exposure).

As you say, this buys time for Greece and the other PIIGS to dig into their budgets and cull as much fat as possible before they have to cut muscle..and they are going to have to cut some. I really think the riots in Athens were a massive gong that will reverberate throughout Europe. Most of the time it takes a crisis to bring about painful changes. Europe has just had one and over the next several quarters it will be worth watching to see if they got the message. If I had to bet right now (and I HAVE) I say they got it. Behavioral change is coming to Europe. It sure would be nice if OUR politicians could have the same wakeup call without going through something like Europe just went through. Unfortunately, I am not as confident. I think periferal, easy cuts will be made but it won't be enough. We will (as usual) need to endure a crisis and likely a gut wrenching national debate on whose oxes get gored for the good of the whole. I am NOT looking forward to it but I fear it is going to be necessary. Fortunatly, for the moment it is still 'out there' in the future somewhere.

I mentioned the panic is over. However the market correction likely is not. We should have a retest over the next few weeks..I believe the lows of last friday will easily hold but they will probably be approached. I will be looking to add some small positions on that retest.

Scott,

You have had a lot of experience in Latin America, Argentina in particular, and thus probably considerable opportunities to observe the workings of the IMF through their involvement there. I would be interested in your perspective on their approach to enforcing the conditions required of those who take their money.

Where I am going here is that I am suspecting that Germany knew from the get-go that Greece was going to be a tough addict to break and they feared dragging up old images of 'the bad German' if THEY had to be the enforcer. They also likely felt that France wouldn't or couldn't do it, and there was no one else who was not in nearly the same condition to make demands. Hence, the IMF.

So. IYO are they up to it? Can they be the heavy? And if so, how tough can they get?

John: The IMF can indeed play the heavy. Unfortunately the IMF can also offer bad advice. The IMF doesn't understand or appreciate supply-side policies, so they usually insist that countries with large fiscal deficits must raise taxes, and they have already said that in the case of Greece. The problem comes when the higher taxes weaken the economy; that in turn weakens investor confidence, and it becomes a vicious cycle. A weaker economy coupled with a weaker currency and less investment can cause the deficit to widen even as tax rates increase.

Some of the things the IMF will push Greece to do are good (cutting spending). They will push very hard. But the outcome is not guaranteed; even if Greece follows the prescription, the cure depends on how everything fits together and whether confidence is maintained.

So many variables are at stake that it is difficult to forecast the outcome with any degree of confidence.

On the positive side, though, is this: the global economy is expanding, and markets are moving up. Without a backdrop of growth, fixing the Greek/Eurozone problem would be a lot more dicey.

I think there is much more receptivity to market solutions than 20-30 years ago, globally. The whole playing field has shifted. I suspect we will see Greece et al reduce government spending as fraction of GDP going forward.

Oddly enough, it is the heavily socialized, administrative state of Germany that is emerging as a fiscally prudent counrty, while countries such as Argentina and Greece, where people are much more individualistic and ignore tax laws and regulations, that have emerged as basket cases.

Once again, it is a country's culture that determines fate. A China, a Germany, a Japan will inevitably prosper due to strong work ethics, savings rates and reasonable administration.

The USA, as always, is a dizzying mix of cultural norms, drawing (I hope) the best from around the world. If we can face down the spenders in either wing of our political parties, we may have a bright future too.

China in a bear market and Greece the canary in the coal mine. The game of hot potato continues unimpeded.

Ironically debtor nations are bailing out even bigger debtor nations. Seem logical right, wrong.

The pie keeps expanding but this is not the kind of pie you want for dinner.

A good analogy can be drawn from the morbidly obese. Many outsiders have the false notion these people could simply eat healthy, exercise, and lose weight.

However, as my brother a gastric bypass surgeon once told me, even if they ate 2,000 calories a day and exercised, they wouldn't lose much weight at all because that is what the body needs uses to maintain itself.

Essentially the morbidly obese need to starve themselves which is why diet is not really an option. Yes they must eat healthier but drastic measures are necessary to save the patient.

Debt is the same thing my friends. Once you reach the tipping point globally, drastic measures are necessary to re-balance the economies.

Everyone cannot be in massive debt and hope to grow their way out the problem at the same time. The sovereign debt trade is awfully crowded and China is not going to save the world.

Scott,

Thanks. That was precisely what I was looking for.

On raising taxes, one thing they can do (Benj brought this up in an earlier post) is do a better job of enforcing and collecting the taxes they have now. There seems to be a culture of tax evasion in Greece that is of epic proportions. It may be that they will need to fix this problem first, since the Greeks are not paying the taxes they owe now.

Glad to know you think the IMF will keep the pressure on. There has to be an enforcer or it is much less likely to happen.

One last thing. Your post shows a graph of the 2yr Greek vs German bond yields. If I am reading this correctly the German yield is something under 1% and the Greek yield is about 8% (down from 18% or so). So the 'spread' is something like 7 1/2%. It would seem to me that this spread would be a good thing to keep an eye on every other week or so stay fairly current on Greece's progress. Am I on base here or am I missing something?

Public,

You make some valid points. There is no doubt (to me) that the world's debt load is going to be a significant headwind to growth. The developed economies are facing years of fiscal austerity. From my perch however it need not end in a disaster if the correct policy choices can be made and adhered to. Just like it IS possible for morbidly obese people to lose weight IF they have the discipline, the will, and the time, so too can nations change their fiscal behaviors and regain investor's confidence. It is not necessary to completely pay off a debt, only get it to the point where it can be managed without economic stress to the country. I am still in the camp that believes these changes can and will be made.

You may very well be proven right in the end. Believe me, I see the risks. However I am still not convinced that it is how you bet.

John: the spread between 2-yr Greek and German bond yields is definitely the thing to watch for signs of progress. The smaller the spread, the better the outlook for Greece.

John I agree it is theoretically possible I just wouldn't put my money on Bernanke and Jintao to save the world.

Public,

Not a thing wrong with that. There are many times I have found myself taking long walks on the beach or through the countryside to relieve my stress or to flesh out my thoughts. Markets NEVER make it easy and there is ALWAYS a boogie man under the bed.

Thank you for challenging my contentions. PLEASE continue to do so whenever you feel it is warranted.

Benj,

I like your term 'a dizzying mix of cultural norms'. I have long believed that our cultural diversity is one one of our greatest assets. My wife and I frequently visit our daughter in NYC and I am always amazed at the incredible diversity of cultures that coexist is such close proxemity. I'm sure something similar exists in LA. In NY I honestly believe there is a community of people who are either immigrants or children of immigrants from every nation on the planet. That diversity in IMHO is a huge asset to a dynamic economy. It makes this nation so, so special. So many cities composed of so many different ethnic cultures all seeking a better life for themselves and their children is a powerful thing. I love to watch it when I have the opportunity.

John-

I love it here too. We take for granted how unbiased Americans are.

Post a Comment