My concern was obviously premature at the time, but it's been in the back of my mind ever since, and I'm starting to get worried again. Consumer confidence has jumped in the past year, and the demand for money has weakened more than at any other time in the current recovery. My concerns may again prove premature, but this is not a trivial issue and thus it bears close scrutiny.

According to both the Conference Board and the University of Michigan surveys, consumer confidence has risen significantly in the past year. It's not yet at all time highs, but it's certainly a good deal better that it has been for the past 8-9 years.

Small business optimism has surged since the November election. "Animal spirits" are on the rise.

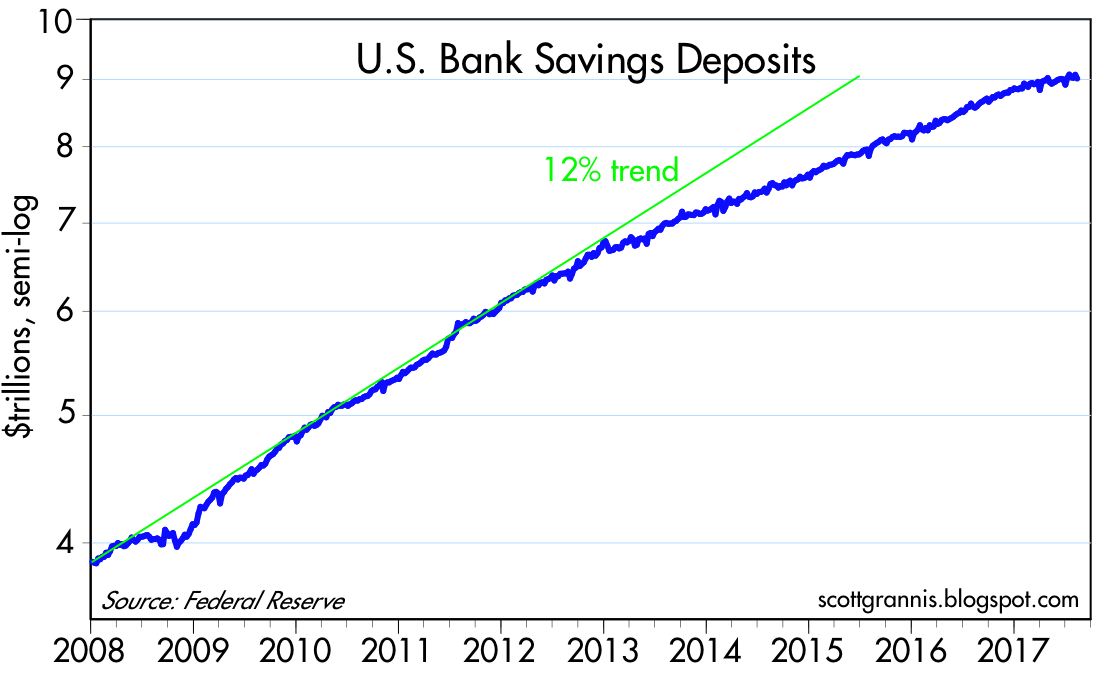

As the two charts above show, the growth of bank savings deposits has slowed significantly in the past 6-7 months, after growing strongly ever since early 2009. Recessions and economic turmoil almost always make bank savings deposits attractive, especially relative to riskier alternatives. Demand for safety typically declines in the latter stages of an expansion, when people's appetite for risk rises in line with rising confidence. So it's normal for rising confidence to be reflected in slower growth of bank deposits.

Bank savings deposits in the past six months have risen at an annualized rate of only 2.5%—that's the lowest rate so far in the current business cycle expansion. Since bank savings deposits comprise comprise about two-thirds of the M2 money supply, slow growth in savings deposits has been matched by a slowdown in the growth of the money supply, which has registered annualized growth 5.3% over the past six months, down from the 6-8% rates of growth that have prevailed over the past six years. Declining growth in the money supply doesn't mean, however, that the Fed has been tightening—more likely it means that the demand for money has been weakening.

The above chart is arguably the most powerful illustration of how strong money demand has been in the past 8-9 years: the ratio of M2 to nominal GDP. Nominal GDP is a proxy for national income, and M2 is arguably the best measure of readily-spendable money. Think of this chart as measure of how much money the average person wants to hold relative to his annual income. It's risen from 50% prior to the Great Recession to 70% today. That's huge, and one of the defining characteristics of the current business cycle expansion—a massive increase in the demand for money.

People now have parked an unprecedented amount of their annual cash flow in retail money market funds, small time deposits, currency and bank savings deposits—and the bulk of the increased money holdings are in the form of bank savings deposits. What's even more impressive, however, is that none of these vehicles pays much in the way of interest. People are holding lots of money not because they like the return on money, but because of its safety.

This huge increase in the demand for money also explains why QE wasn't inflationary. The banking industry, faced with huge infusions of deposits, was happy to lend all that money to the Fed in exchange for the new bank reserves that the Fed created via its QE operations. People wanted more money, and banks wanted more reserves (banks were very risk-averse, just as most people were), and QE effectively accommodated that change in preference. If the banks hadn't wanted to lend all that money to the Fed, but instead to the private sector (and assuming the private sector had wanted to borrow a lot more), the result would have been a massive expansion in the amount of money in the economy, and a lot more inflation. But that didn't happen, thanks to increased money demand.

We now may be on the cusp of a reversal in the huge increase in money demand. With increased confidence, the public is becoming less desirous of accumulating money balances. The growth of bank savings deposits has slowed significantly, and it is now less than the growth of incomes. People may now be desirous of decreasing their holdings of cash relative to incomes. But since cash can't disappear, the public can only accomplish a reduction in their relative holdings of money by bidding up the prices of other things. Less demand for money means a lower price for money and a higher yield on money, plus higher prices for things and eventually higher nominal incomes. That's another way of saying that a decline in money demand is likely to result in an increase in inflation—unless the Fed takes offsetting measures.

I note the recent rise in gold prices (+15% year to date) and the decline in the value of the dollar (-9% year to date). Both are symptomatic of an excess of money relative to the demand for it, and thus they could be evidence that the Fed is falling behind the inflation curve.

Much hangs on just how much and how fast the public's demand for money declines, and how fast and how much the Fed is able to offset that by raising interest rates and reducing excess reserves in the banking system. So far things look OK, but it certainly pays to keep an eye on these developments.