Tuesday, September 30, 2008

Money market funds now guaranteed

One less reason to worry. Yesterday Treasury announced that participating money market funds will now be covered under its new guarantee program. Funds can participate by paying a nominal fee of 1 or 1.5 basis points, and that guarantees that their funds will never "break the buck;" which in turn means investors can count on redeeming their shares at $1.00. This makes money market funds virtually as safe as T-bills. It's reasonable to think that almost all funds (except those that invest in only Treasury securities) will participate, if only to maintain their competitive advantage.

Accounting reforms are coming

The SEC and FASB have indicated they are going to support liberalizing strict mark-to-market accounting rules and that could go a long way to alleviating the pressures on many banks that are holding distressed subprime securities. This is a "bailout" that works simply by injecting some common sense into the problem. Excellent!

Pulling back from the abyss

All the measures of fear, uncertainty and doubt have subsided, and the waves of selling that drove prices down yesterday are retreating. The sky hasn't fallen, even though Congress is taking a day or two off. Yesterday I should have remembered a favorite maxim: by the time the politicians figure out there is a crisis and pass laws to fix it, it's too late, probably unnecessary, and only tends to make things worse.

I'm also remembering that the eventual losses from subprime loans are indeed finite, and the bulk of them have been declared, absorbed, and written off. In round numbers (don't quote me on this), subprime loans totaled about $1.5 trillion. Even if you assume the absolute worst, that every single loan defaults and banks recover only half of the original loan value when properties are foreclosed and sold, the total losses can not be more than $750 billion. More realistically, the total losses can't be more than $500-600 billion, because obviously not every borrower will go bust and not every house will lose half of its value. I believe we've already seen the bulk of those losses realized by unfortunate banks, insurance companies, hedge funds, etc. Maybe there is another $100 billion or so that's waiting in the wings, but how could such a piddling amount bring the $15 trillion US economy to its knees?

Those who argue that the sky is going to fall if Congress doesn't act are betting that the losses will be far more than is possible from defaulted subprime loans. They worry about all the leverage in the system and the many trillions of swaps and other derivative contracts. But those things are just ways in which the system redistributes risk; they magnify risk for some and reduce it for others. As for total risk, it's a zero sum situation.

I'm also remembering that the eventual losses from subprime loans are indeed finite, and the bulk of them have been declared, absorbed, and written off. In round numbers (don't quote me on this), subprime loans totaled about $1.5 trillion. Even if you assume the absolute worst, that every single loan defaults and banks recover only half of the original loan value when properties are foreclosed and sold, the total losses can not be more than $750 billion. More realistically, the total losses can't be more than $500-600 billion, because obviously not every borrower will go bust and not every house will lose half of its value. I believe we've already seen the bulk of those losses realized by unfortunate banks, insurance companies, hedge funds, etc. Maybe there is another $100 billion or so that's waiting in the wings, but how could such a piddling amount bring the $15 trillion US economy to its knees?

Those who argue that the sky is going to fall if Congress doesn't act are betting that the losses will be far more than is possible from defaulted subprime loans. They worry about all the leverage in the system and the many trillions of swaps and other derivative contracts. But those things are just ways in which the system redistributes risk; they magnify risk for some and reduce it for others. As for total risk, it's a zero sum situation.

Deregulation did not cause this crisis

It's very important to dispel the myth that the current financial crisis was the result of deregulation. As Peter Wallison notes in this article:

There has been a great deal of deregulation in our economy over the last 30 years, but none of it has been in the financial sector or has had anything to do with the current crisis.

The repeal of portions of the Glass-Steagall Act in 1999 has no relevance whatsoever to the financial crisis, with one major exception: it permitted banks to be affiliated with firms that underwrite securities, and thus allowed Bank of America Corp. to acquire Merrill Lynch & Co. and JPMorgan Chase & Co. to buy Bear Stearns Cos. Both transactions saved the government the costs of a rescue and spared the market substantial additional turmoil.

None of the investment banks that got into financial trouble, specifically Bear Stearns, Merrill Lynch, Lehman Brothers Holdings Inc., Morgan Stanley and Goldman Sachs Group Inc., were affiliated with commercial banks, and none were affected in any way by the repeal of Glass-Steagall.

It is correct to say that there has been significant deregulation in the U.S. over the last 30 years, most of it under Republican auspices. But this deregulation -- in long-distance telephone rates, air fares, securities-brokerage commissions, and trucking, to name just a few sectors of the economy where it occurred -- has produced substantial competition and innovation, driving down consumer costs and producing vast improvements and efficiencies in our economy.

Republicans have favored financial regulation where it was necessary, as in the case of Fannie Mae and Freddie Mac, while the Democrats have opposed it. In 2005, the Senate Banking Committee, then under Republican control, adopted a tough regulatory bill for Fannie and Freddie over the unanimous opposition of committee Democrats. The opposition of the Democrats when the bill reached the full Senate made its enactment impossible.

Calafia beach morning

Here on Calafia Beach the world seems utterly unaffected by the recent tumultous events in the financial markets. Irrelevant observation of the day: the distant point at the left of the photo is where Nixon had his Western White House.

Here on Calafia Beach the world seems utterly unaffected by the recent tumultous events in the financial markets. Irrelevant observation of the day: the distant point at the left of the photo is where Nixon had his Western White House.

Monday, September 29, 2008

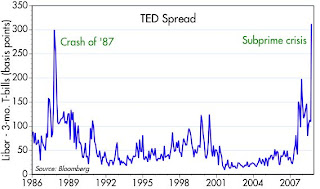

This eclipses the '87 crash in a way

The TED spread, a measure of how much fear there is that the bank you are trusting with your money may default on you, has reached a record high, eclipsing the panic in the wake of the '87 stock market crash. Someone needs to lift the cap on federal deposit insurance to fix this.

The TED spread, a measure of how much fear there is that the bank you are trusting with your money may default on you, has reached a record high, eclipsing the panic in the wake of the '87 stock market crash. Someone needs to lift the cap on federal deposit insurance to fix this.

What if the sky doesn't fall?

The House has rejected the bailout bill, and markets have plunged. The bill was sold as absolutely essential to avert a financial market meltdown. But what if the there is no meltdown? Markets are down now in a knee-jerk reaction. But what if it turns out that the bill wasn't really all that critical? That would be almost unimaginably bullish. The next few days will be intensely interesting. I think there's a good chance we avert disaster, somehow.

VIX hits post-'87 crash high

Lots of panic selling going on. We could be very near a final capitulation that would mark the bottom. I hope.

Lots of panic selling going on. We could be very near a final capitulation that would mark the bottom. I hope.

Inflation update; still drifting higher

The market is obsessed this morning with the possibility that the bailout won't pass and/or we'll have massive bank failures and an ensuing depression; stocks are down and the VIX is back up to 40. While the market sorts out who is going to get stuck with the remaining subprime losses, I thought I'd highlight the inflation figures released today. As the chart shows, the Fed's preferred measures of inflation have been above target since early 2004. Energy prices are clearly the drivers behind the rise in overall inflation, but core inflation (ex-food&energy) has been drifting higher as well. That tells me that the Fed has been effectively accommodating higher energy prices with easy money—allowing higher energy prices to be passed through to other areas of the economy. It's also significant that there is no sign of moderation despite the weakness in the economy and falling housing prices in recent years. Traditional Phillips Curve thinking has held that we should have seen some moderation by now. Instead, the traditional monetary approach to understanding inflation has been more accurate in its predictions.

The market is obsessed this morning with the possibility that the bailout won't pass and/or we'll have massive bank failures and an ensuing depression; stocks are down and the VIX is back up to 40. While the market sorts out who is going to get stuck with the remaining subprime losses, I thought I'd highlight the inflation figures released today. As the chart shows, the Fed's preferred measures of inflation have been above target since early 2004. Energy prices are clearly the drivers behind the rise in overall inflation, but core inflation (ex-food&energy) has been drifting higher as well. That tells me that the Fed has been effectively accommodating higher energy prices with easy money—allowing higher energy prices to be passed through to other areas of the economy. It's also significant that there is no sign of moderation despite the weakness in the economy and falling housing prices in recent years. Traditional Phillips Curve thinking has held that we should have seen some moderation by now. Instead, the traditional monetary approach to understanding inflation has been more accurate in its predictions.Barring a gigantic collapse in oil prices, the upward and above-trend drift in inflation is likely to persist until the Fed decides to tighten policy to fight it. With all the focus on saving the economy, that is not likely to happen soon. The gold market has been on top of this, which is why gold prices are in the range of $900 today, up hugely from $300 when inflation hit a low point in 2002-2003. The dollar is up today as the whole world worries about bank failures and the dollar is seen as some port in a storm, but the dollar remains very weak from an historical perspective, and that confirms the message of gold prices; the Fed is not paying sufficient attention to the value of the dollar.

I don't think any of this means the end of the world as we know it. But I do think that we see here the seeds of the next thing the market will worry about once the subprime mess simmers down. Rising inflation has been bad for the economy (inflation is always bad for growth), but an inflation-fighting Fed won't necessarily be bad for the economy. Tighter monetary policy will be bad for Treasury bonds (higher yields) but very good for confidence, and that's good for the economy.

Sunday, September 28, 2008

Thinking about the "bailout"

It seems that Congress is likely to approve a plan that could resolve the current financial mess. It won't be a "bailout" in the sense that the government will repair the losses suffered by people who made bad decisions or were the unwitting victims of predatory lending. The government will in effect step in to shoulder some of the risk and uncertainty that seem to have paralyzed the financial markets. And for doing that government will extract a heavy price.

Treasury will get the authority to spend several hundred billion to buy troubled assets, and this should relieve some of the pressure on the banking industry. It's not a terrible arrangement at all: Treasury will be buying interest-bearing assets at distressed prices, and under normal circumstances that is a value investor's dream come true. Congress will have an option to recoup some of the losses if it doesn't work, and that will please those critics of bailouts who don't understand that if the plan doesn't work and all heck breaks loose, the banks won't have the ability to pay a tax in the future. But if all goes well, as is likely, then everyone is going to be happy. So I would look for this to produce positive results in the near term.

The things to worry about are the long term consequences. Moral hazard is going to be very much alive and well. Markets will learn once again to expect the government to come to the rescue whenever misguided government policies lead to predictable, disastrous results. Politicians (and, I would note, the Federal Reserve) will once again escape the blame for having created this mess in the first place. Voters will once again fail to understand that the problem is too much government, not insufficient government. Government will have more influence over the economy, the private sector less. Though very unfortunate, it's not going to be the end of the world, just another setback on the (sure to be slower) road to progress.

Meanwhile, for a look at what might have been a better solution, check out Brian Wesbury's alternative proposal, which calls for a fairly simple change in the accounting rules. He notes something that others have missed, by the way, which bears repeating here: if Treasury ends up making a profit on this "bailout" plan, then that profit will accrue at the expense of the private sector, and that equates to a tax. So if the plan works, the government could end up collecting a big, indirect tax on the financial sector. If the plan doesn't work, the government gets the option of imposing a big direct tax on the financial sector; and as we all should know, businesses never pay taxes—it's always the consumer that pays the taxes. So it's a win-win for the government, and a win-lose for the consumer: we escape a financial crisis caused by the government only to be burdened in the future by a more oppressive government presence in our lives.

Treasury will get the authority to spend several hundred billion to buy troubled assets, and this should relieve some of the pressure on the banking industry. It's not a terrible arrangement at all: Treasury will be buying interest-bearing assets at distressed prices, and under normal circumstances that is a value investor's dream come true. Congress will have an option to recoup some of the losses if it doesn't work, and that will please those critics of bailouts who don't understand that if the plan doesn't work and all heck breaks loose, the banks won't have the ability to pay a tax in the future. But if all goes well, as is likely, then everyone is going to be happy. So I would look for this to produce positive results in the near term.

The things to worry about are the long term consequences. Moral hazard is going to be very much alive and well. Markets will learn once again to expect the government to come to the rescue whenever misguided government policies lead to predictable, disastrous results. Politicians (and, I would note, the Federal Reserve) will once again escape the blame for having created this mess in the first place. Voters will once again fail to understand that the problem is too much government, not insufficient government. Government will have more influence over the economy, the private sector less. Though very unfortunate, it's not going to be the end of the world, just another setback on the (sure to be slower) road to progress.

Meanwhile, for a look at what might have been a better solution, check out Brian Wesbury's alternative proposal, which calls for a fairly simple change in the accounting rules. He notes something that others have missed, by the way, which bears repeating here: if Treasury ends up making a profit on this "bailout" plan, then that profit will accrue at the expense of the private sector, and that equates to a tax. So if the plan works, the government could end up collecting a big, indirect tax on the financial sector. If the plan doesn't work, the government gets the option of imposing a big direct tax on the financial sector; and as we all should know, businesses never pay taxes—it's always the consumer that pays the taxes. So it's a win-win for the government, and a win-lose for the consumer: we escape a financial crisis caused by the government only to be burdened in the future by a more oppressive government presence in our lives.

Friday, September 26, 2008

Markets are braced for bad news

Spreads on BB and B corporate bonds are about as high as they have ever been, nearly matching the highs we saw in the wake of the disastrous corporate governance scandals in 2002. It was in early October '02 that spreads peaked and the stock market reached its bear market low. It was a time when the consensus view was that we were mired in a jobless recovery, the Fed was powerless to do anything about it ("pushing on a string"), and company bankruptcies were going to be widespread.

Spreads on BB and B corporate bonds are about as high as they have ever been, nearly matching the highs we saw in the wake of the disastrous corporate governance scandals in 2002. It was in early October '02 that spreads peaked and the stock market reached its bear market low. It was a time when the consensus view was that we were mired in a jobless recovery, the Fed was powerless to do anything about it ("pushing on a string"), and company bankruptcies were going to be widespread.That we are once again seeing similar signs of distress in the market (the VIX index closed today at almost 35) means the market is assigning a relatively high probability to a very ugly economic scenario in which many companies end up failing, the economy likely slides into a long and painful recession, and the Fed and Congress can do little to stop it. That doesn't mean the market is right, rather that if you want to be bearish these days you have to believe in a real doomsday scenario. Anything less and spreads will narrow, corporate bonds will be very attractive investments, stocks will rally, and subprime loans bought by Treasury could end up being quite profitable.

So if the bailout fails to materialize this weekend or looks so ugly that it will be ineffective, markets could be disappointed, but the disappointment can't be much worse than what is already priced into the market. That, and the many signs that the economy on balance is still in reasonably good shape, suggest that the odds favor remaining bullish.

Money is plentiful

Bank reserves are the foundation of our monetary system. The Fed controls monetary policy by targeting the rate at which banks lend reserves to each other. They do this by adding or subtracting reserves from the system. In the past week or so, the Fed has added a gigantic amount of reserves to the system, as shown in this chart (the last data point is my estimate based on the recent expansion of the Fed's balance sheet). The amount of reserves they have dumped into the system of late dwarfs the action they took in the Y2K and 9/11 crises. This is a big deal.

Bank reserves are the foundation of our monetary system. The Fed controls monetary policy by targeting the rate at which banks lend reserves to each other. They do this by adding or subtracting reserves from the system. In the past week or so, the Fed has added a gigantic amount of reserves to the system, as shown in this chart (the last data point is my estimate based on the recent expansion of the Fed's balance sheet). The amount of reserves they have dumped into the system of late dwarfs the action they took in the Y2K and 9/11 crises. This is a big deal.Is this inflationary? Potentially, yes. However, since most of the increased reserves can be attributed to a surge in the demand for reserves on the part of banks trying to shore up their liquidity position, the Fed is simply supplying extra money in order to meet extra demand for money, and this is not inflationary. On balance, however, it appears that the Fed has added excess reserves to the system, and that is how inflation can really get going. How do I know this? Since the injection of extra reserves, the Federal funds rate has consistently traded below its target, reflecting an excess of funds in the system. Also, the dollar has weakened, gold has strengthened, and short-term interest rates have collapsed.

It appears the Fed is already trying to reverse its injections of reserves, so there is no reason yet for great alarm. We need to watch this however. Meanwhile, the chart underscores the gravity of the current crisis and the extent to which the Fed is trying to alleviate the pressures in the banking system.

Thursday, September 25, 2008

Thoughts on subprime stuff

Many people question why it is that banks on the verge of failure can't sell their subprime mortgage paper themselves, and why Treasury has to be the buyer of last resort. Are mark-to-market prices really absurdly low? If they are, where are the private speculators, the vulture funds? Why aren't they greedily buying this cheap paper?

One reason that is not widely understood is the extreme complexity of subprime mortgages. Where I used to work we had a small army of people who did nothing but track (almost daily) the cash flows of different mortgage securities, under the direction of a guy who has spent his entire professional life studying mortgages. These were smart guys, but they were blindsided just like everyone else. Things happened that were unforseeable at the time, to securities thought to be virtually bullet-proof.

An outsider would find it extremely difficult to step in and buy distressed subprime paper from a desperate bank. Evaluating these securities is extraordinarily difficult, complex, and time consuming. Every tranche of every deal (numbering in the hundreds and thousands) is unique. These are not your typical junk bond. What are they really worth? Who knows?

The value of a subprime mortgage-backed bond is a function of multiple independent variables: the level of interest rates, the shape of the yield curve, prepayment speeds, housing prices, the structure of each individual security, geographical exposure, and volatility assumptions. A handful of experts can attempt to make sense out of all this, but for the vast majority of investment professionals, it is virtually impossible.

One reason that is not widely understood is the extreme complexity of subprime mortgages. Where I used to work we had a small army of people who did nothing but track (almost daily) the cash flows of different mortgage securities, under the direction of a guy who has spent his entire professional life studying mortgages. These were smart guys, but they were blindsided just like everyone else. Things happened that were unforseeable at the time, to securities thought to be virtually bullet-proof.

An outsider would find it extremely difficult to step in and buy distressed subprime paper from a desperate bank. Evaluating these securities is extraordinarily difficult, complex, and time consuming. Every tranche of every deal (numbering in the hundreds and thousands) is unique. These are not your typical junk bond. What are they really worth? Who knows?

The value of a subprime mortgage-backed bond is a function of multiple independent variables: the level of interest rates, the shape of the yield curve, prepayment speeds, housing prices, the structure of each individual security, geographical exposure, and volatility assumptions. A handful of experts can attempt to make sense out of all this, but for the vast majority of investment professionals, it is virtually impossible.

More thoughts on the bailout (2)

The public is currently terrified of owning anything with subprime exposure, and terrified of lending to banks that might be wiped out by such exposure. At the same time the public is desperate for the safety of T-bills and T-bonds, to the extent that T-bill yields fell almost to zero the other day and are still less than 1%.

If Treasury actually goes ahead with the $700 bailout plan, this is the essence of what will happen:

Treasury will give the public exactly what it is desperate for (by selling a slug of new T-bills and T-bonds), and in return take from the public exactly what it doesn't want (subprime mortgage securities). It shouldn't have any trouble accomplishing this if and when the authority is granted.

In the financial market the role that Treasury will be playing is traditionally the role of the speculator; the one who buys what no one wants in exchange for the cash that everyone wants. The problem many people have with this (myself included) is that the Constitution does not give the federal government the authority to be a speculator. That's what the private sector is for.

If Treasury actually goes ahead with the $700 bailout plan, this is the essence of what will happen:

Treasury will give the public exactly what it is desperate for (by selling a slug of new T-bills and T-bonds), and in return take from the public exactly what it doesn't want (subprime mortgage securities). It shouldn't have any trouble accomplishing this if and when the authority is granted.

In the financial market the role that Treasury will be playing is traditionally the role of the speculator; the one who buys what no one wants in exchange for the cash that everyone wants. The problem many people have with this (myself included) is that the Constitution does not give the federal government the authority to be a speculator. That's what the private sector is for.

More thoughts on the bailout

I don't like the idea of a bailout, and I wonder if it is necessary, but I do know that the financial markets are under extreme stress. This chart of the TED spread (a measure of stress in interbank lending) makes the point—this is worse than the Crash of '87. Bad policies and short-sighted politicians got us into this mess, and there is no easy way out at this point, unfortunately. The wheels of commerce are still turning, as I've been pointing out, and loans are still being made, but a potentially large number of banks are at risk of failure. The problem is that they have more exposure to subprime real estate than they ever imagined. That's because the market is currently assuming that the extent of the housing market collapse will be far greater than even the most extreme, pessimistic assumptions that people used a few years ago.

I don't like the idea of a bailout, and I wonder if it is necessary, but I do know that the financial markets are under extreme stress. This chart of the TED spread (a measure of stress in interbank lending) makes the point—this is worse than the Crash of '87. Bad policies and short-sighted politicians got us into this mess, and there is no easy way out at this point, unfortunately. The wheels of commerce are still turning, as I've been pointing out, and loans are still being made, but a potentially large number of banks are at risk of failure. The problem is that they have more exposure to subprime real estate than they ever imagined. That's because the market is currently assuming that the extent of the housing market collapse will be far greater than even the most extreme, pessimistic assumptions that people used a few years ago.I can't prove this, but people I trust tell me that subprime paper is currently priced to the assumption that nationwide housing prices will fall 40-50%, triggering massive defaults and losses to those holding subprime loan tranches that were once considered virtually bullet-proof. (Here's an analogy: you're a conservative investor that buys only AAA-rated corporate bonds from the country's premier corporations. One day you wake up to discover that virtually ever major corporation is expected to default on its obligations. You simply can't believe it, but you're wiped out.) So far prices have fallen by about 20% in major markets, according to the Case-Shiller indices, but the market is assuming we're less than halfway to the eventual bottom in housing prices. To be a willing seller of subprime-related paper today, you have to believe that prices will fall by more than 50% from their mid-2006 peak. I know some houses in the Inland Empire have already fallen by that much, but to think that this will be repeated everywhere around the country is pretty pessimistic to say the least, and would certainly prove catastrophic to just about everyone.

If the bailout can result in unburdening the banking system of some portion of these distressed securities, we will avert massive bank failures and restore badly-needed confidence. It is not unreasonable to think that the loans that Treasury ends up purchasing could prove to be quite profitable. They might not even have to spend $700 billion; just demonstrating that it is possible might be enough to attract bottom-feeders who would willing relieve the banks of these loans at higher prices.

Capital goods orders still healthy

Capital goods orders are not robust, but neither are they declining, despite all the bad news out there. Notably, there is nothing like the weakness we typically see in recessions. Businesses are still investing in new plant and equipment, and that is the seed corn for future growth in productivity, so this is a healthy sign.

Capital goods orders are not robust, but neither are they declining, despite all the bad news out there. Notably, there is nothing like the weakness we typically see in recessions. Businesses are still investing in new plant and equipment, and that is the seed corn for future growth in productivity, so this is a healthy sign.

Wednesday, September 24, 2008

Existing home sales have stabilized

Existing single-family home sales are way down from their peak, but they haven't dropped at all in the past 11 months. Total home sales (including townhomes and condos) are unchanged from their Dec. '07 level. Meanwhile, prices are falling. This is a healthy development. If sales were still declining that would mean a dearth of buyers even as prices fall. Instead we have plenty of buyers stepping up to buy homes as they become more affordable. And yes, a good percentage of the sales are foreclosed properties, but that doesn't change the fact that the homes are getting sold. It also provides evidence that there is financing available, albeit without the generous terms available a few years ago. Is the whole financial system really as "clogged up" as Bernanke and Paulson would have us believe?

Existing single-family home sales are way down from their peak, but they haven't dropped at all in the past 11 months. Total home sales (including townhomes and condos) are unchanged from their Dec. '07 level. Meanwhile, prices are falling. This is a healthy development. If sales were still declining that would mean a dearth of buyers even as prices fall. Instead we have plenty of buyers stepping up to buy homes as they become more affordable. And yes, a good percentage of the sales are foreclosed properties, but that doesn't change the fact that the homes are getting sold. It also provides evidence that there is financing available, albeit without the generous terms available a few years ago. Is the whole financial system really as "clogged up" as Bernanke and Paulson would have us believe?

Tuesday, September 23, 2008

Households' financial burdens are not excessive

You would think that in the aftermath of a huge rise in housing prices and all the refinancing and zero-down loans that took place in its wake, households today would be laboring under increased financial burdens. But you would be wrong. Data released today by the Fed shows that financial burdens dropped in the second quarter of this year, and as a result have not risen materially since 2001. The big increases in financial burdens happened in the 1995-2000 period, long before housing prices went up. This is just one more example of how the housing/subprime crisis is actually quite limited in scope. If anything, the wave of defaults and falling home prices sweeping the country is shifting the burden away from households onto the shoulders of the banks and other institutions that were holding the mortgages that are defaulting. In a sense it's a zero-sum game, and thus does not necessarily imply the imminent destruction of the U.S. economy.

You would think that in the aftermath of a huge rise in housing prices and all the refinancing and zero-down loans that took place in its wake, households today would be laboring under increased financial burdens. But you would be wrong. Data released today by the Fed shows that financial burdens dropped in the second quarter of this year, and as a result have not risen materially since 2001. The big increases in financial burdens happened in the 1995-2000 period, long before housing prices went up. This is just one more example of how the housing/subprime crisis is actually quite limited in scope. If anything, the wave of defaults and falling home prices sweeping the country is shifting the burden away from households onto the shoulders of the banks and other institutions that were holding the mortgages that are defaulting. In a sense it's a zero-sum game, and thus does not necessarily imply the imminent destruction of the U.S. economy.

Do we really need a $700 billion bailout?

I'm thinking that the Paulson/Bernanke Plan, which would give Treasury the authority to buy up to $700 billion worth of troubled securities, is not really necessary. Brian Wesbury made a similar point yesterday in this article. The more I research the problem, the more apparent it becomes that clumsy accounting rules have made a bad situation (the decline of housing prices and the subsequent default of lots of mortgages) worse. Institutions other than banks that hold distressed mortgage-backed securities are required to value them at their mark-to-market value. Banks can opt to hold them in a special category that doesn't require mark to market valuation, which is one big reason that Goldman and Morgan Stanley wanted to become banks. This value is currently being determined by distressed sales of these securities, and thus the prices are in many cases much less than the value that could be realized by holding the security to maturity. Why not allow firms to value the securities based on some other method? That is almost exactly what Paulson and Bernanke are pushing for, but they don't take the next logical step. They envision Treasury sponsoring some sort of auction system that would attach more reasonable values to these securities. If Treasury were willing to pay that price, then it would give everyone a firm basis for using that value in their mark to market accounting.

Why does Treasury have to buy the securities? Isn't there some mechanism that would accomplish the same thing without requiring Treasury to become a major holder of mortgage securities? Wesbury suggests that Treasury could sell insurance to companies that would backstop their security valuations, among other ideas. Surely some clever rocket scientist out there can come up with a good plan that doesn't socialize a large portion of mortgage industry.

Why does Treasury have to buy the securities? Isn't there some mechanism that would accomplish the same thing without requiring Treasury to become a major holder of mortgage securities? Wesbury suggests that Treasury could sell insurance to companies that would backstop their security valuations, among other ideas. Surely some clever rocket scientist out there can come up with a good plan that doesn't socialize a large portion of mortgage industry.

Origins of the current crisis

The Wall St. Journal has an excellent article today that explains the origins of the housing/subprime credit crisis. Here's my short summary: Freddie, Fannie, and Congress are the major culprits. It started in 2003 when Congress pressured F&F to make housing more affordable. F&F responded by becoming the largest buyers (total GSE exposure exceeded $1 trillion ) of subprime and Alt-A mortgages. Without F&F's voracious appetite for these loans, the mortgage industry likely would not have created more than a fraction of the loans that have now brought our financial markets to their knees. The Senate banking committee in 2005 tried to pass a major F&F reform bill supported by Republicans that would have prohibited F&F from holding portfolios and would have subjected them to regulation similar to that of banks. "McCain endorsed the legislation in a speech on the Senate floor. Obama, like all other Democrats, remained silent." Democrats refused to allow the bill to come to a vote. And the rest is history.

Monday, September 22, 2008

The inflation trade is back with a vengeance

The market is still worried about how the Paulson/Frank bailout plan will actually work and how it will affect the economy. I'm still wondering myself, and it's hard to find anything to cheer about, except that one way or another the government is going to be socializing the costs of the housing crisis. This will take pressure off of the financial sector and should lead to an unclogging of the financial system over time. The great unknown is just how bad this precedent will be for the future of our free market system, as the government plays an ever-greater role in financial markets.

Meanwhile, the concerns about inflation have really heated up in the past two trading days. A weaker dollar, soaring gold and oil prices, and rising breakeven spreads on TIPS are all signs that the market is getting more worried now about inflation. The Fed has been plenty easy, in my view (though other supply siders, most notably Art Laffer would disagree), and they still are, so it's no surprise to see this.

The actions in dollar, gold and oil all suggest that the problem we're facing is not one of a shortage of dollars. Dollars are plentiful and cheap, why else would the value of the dollar be declining against these three key benchmarks?

If there is plenty of money in the system, then it's likely that the economy won't be as bad as many people seem to fear. Inflation is not good for an economy, since it leads to malinvestments (like the housing boom) that then need to be worked off and result in lost productivity. But we're not in a hyperinflation were everything is paralyzed. So I'm still optimistic that we're going to avoid an economic collapse or a deflation as some are predicting. The surprise will likely be that the economy continues to grow, albeit modestly, and inflation continues to be a problem. Should this be the case, look for Treasury yields to rise significantly, and all other yields to rise by much less.

Meanwhile, the concerns about inflation have really heated up in the past two trading days. A weaker dollar, soaring gold and oil prices, and rising breakeven spreads on TIPS are all signs that the market is getting more worried now about inflation. The Fed has been plenty easy, in my view (though other supply siders, most notably Art Laffer would disagree), and they still are, so it's no surprise to see this.

The actions in dollar, gold and oil all suggest that the problem we're facing is not one of a shortage of dollars. Dollars are plentiful and cheap, why else would the value of the dollar be declining against these three key benchmarks?

If there is plenty of money in the system, then it's likely that the economy won't be as bad as many people seem to fear. Inflation is not good for an economy, since it leads to malinvestments (like the housing boom) that then need to be worked off and result in lost productivity. But we're not in a hyperinflation were everything is paralyzed. So I'm still optimistic that we're going to avoid an economic collapse or a deflation as some are predicting. The surprise will likely be that the economy continues to grow, albeit modestly, and inflation continues to be a problem. Should this be the case, look for Treasury yields to rise significantly, and all other yields to rise by much less.

Sunday, September 21, 2008

Real yields are rising and that's good

This chart says a lot. The bottom line is the market's expectation for consumer price inflation over the next 5 years (and it is also the difference between the top two lines). The middle line is the real yield on 5-year TIPS. The top line is the nominal yield on 5-year Treasuries. Let's suppose we're in a recession now, as most people seem to think. If so, what is different about now versus the recession of 2001? First what's the same: both times inflation expectations fell, since the market believes (because of the Phillips Curve theory of inflation) that a weak economy will reduce inflation. Both times nominal yields fell, because a) the Fed eased in response to the weakness, and b) a weak economy increases uncertainty and the demand for the safe haven of Treasuries. This time, however, real yields are rising whereas they fell in 2001. That tells me that the market is significantly reassessing its expectations of Fed policy. Short-term real yields are heavily influenced by the market's perception of future Fed policy. Higher real yields mean the market is expecting the Fed to be tighter than was previously expected. That in turn implies a stronger underlying economy. Think of the real yield on short maturity TIPS as similar in some sense to the economy's expected growth potential. This is another reason to be bullish on stocks.

This chart says a lot. The bottom line is the market's expectation for consumer price inflation over the next 5 years (and it is also the difference between the top two lines). The middle line is the real yield on 5-year TIPS. The top line is the nominal yield on 5-year Treasuries. Let's suppose we're in a recession now, as most people seem to think. If so, what is different about now versus the recession of 2001? First what's the same: both times inflation expectations fell, since the market believes (because of the Phillips Curve theory of inflation) that a weak economy will reduce inflation. Both times nominal yields fell, because a) the Fed eased in response to the weakness, and b) a weak economy increases uncertainty and the demand for the safe haven of Treasuries. This time, however, real yields are rising whereas they fell in 2001. That tells me that the market is significantly reassessing its expectations of Fed policy. Short-term real yields are heavily influenced by the market's perception of future Fed policy. Higher real yields mean the market is expecting the Fed to be tighter than was previously expected. That in turn implies a stronger underlying economy. Think of the real yield on short maturity TIPS as similar in some sense to the economy's expected growth potential. This is another reason to be bullish on stocks.Update: the expected rate of inflation embodied in the TIPS market has risen sharply in recent days. That it had fallen so much was the anomaly.

Palin continues to lift McCain

Well, this is getting serious. What can explain Palin power? Victor Davis Hanson has a thoughtful essay on the subject. A few quotes:

Well, this is getting serious. What can explain Palin power? Victor Davis Hanson has a thoughtful essay on the subject. A few quotes:Most of you ... seem to think that a fumbling nervous Obama in interviews, who grasps for a word and utters vacuous platitudes is “really” contemplative, like his Harvard Law professors; but when a Sarah Palin seems nervous under scrutiny from a pseudo-professorial, glasses-on-the-lower-nose Charlie Gibson, she is clearly an empty head with an Idaho BA.More impressively, "thousands of Floridians lined up to see Sarah Palin today in Florida. 60,000 people showed up to see Governor Palin in a community of about 75,000." See the rest here. She's clearly tapped into some force that Obama seems to have left behind.

I think it is much harder for a mother of three or four in an out-of-the-way Alaskan town to get elected to city council and the mayorship, then take on the entire Republican establishment and get elected governor than it is for a Barack Obama to emerge from Chicago politics into the Illinois state house and later Senate. The qualities that allowed a Palin to succeed without the power spouse, the identity politics, the Ivy-League cachet, the fawning New York editors and DC insider-press will ensure she does not implode on the campaign trail—and won’t in office either.

Update: take this chart with several grains of salt—today's figures (9/22) reversed the probabilities dramatically, with Obama at 57% and McCain at 41%. Not sure how or why to explain the sudden shift.

Saturday, September 20, 2008

Forgotten facts

Tom Feeney (R-Fl) reminds us that the housing crisis is finite because the vast majority of homeowners have been responsible and prudent. Unfortunately, the forgotten majority will now be bailing out the distressed minority:

"I come today to speak on behalf of the forgotten man, and that includes some 50% of Americans that either own their home, or are renting . . . the 95% of homeowners that are making their payments on time . . . the 99% of Americans that did not behave irresponsibly . . . that ultimately will pay the price for this bill."

Friday, September 19, 2008

Most exciting election in recent memory

Some computer science and political science students at the University of Illinois have put together a mathematical model to predict the probability of each candidate receiving a majority of the Electoral Votes, and thus winning the presidency. As inputs they use well-known polls of voters in each state and then aggregate the results using a dynamic programming algorithm. You can even play around with the assumptions, depending on your view of how swing voters are likely to lean. The data don't cover the period between the time Palin's candicacy was announced and just before she gave her acceptance speech, but it is nevertheless clear that Sarah Palin was the biggest thing to happen to this election so far. Obama was almost a sure thing to win in late August, but now McCain has a modest lead. The betting on Intrade has generally reflected this same shift, although today McCain trails Obama by 4 points.

Some computer science and political science students at the University of Illinois have put together a mathematical model to predict the probability of each candidate receiving a majority of the Electoral Votes, and thus winning the presidency. As inputs they use well-known polls of voters in each state and then aggregate the results using a dynamic programming algorithm. You can even play around with the assumptions, depending on your view of how swing voters are likely to lean. The data don't cover the period between the time Palin's candicacy was announced and just before she gave her acceptance speech, but it is nevertheless clear that Sarah Palin was the biggest thing to happen to this election so far. Obama was almost a sure thing to win in late August, but now McCain has a modest lead. The betting on Intrade has generally reflected this same shift, although today McCain trails Obama by 4 points.HT: Club for Growth

Back to worrying about inflation

Now that the market is much less worried about a financial market implosion that leads to an economic collapse, it's turning its attention back to what I've been worrying about all along: inflation. Standard thinking (inspired by the Phillips Curve) says that if the economy is very weak, inflation will fall. That's why the bond market hasn't been too worried about $900 gold and $100 oil, because the weak economy would presumably take care of the inflation problem that these are symptoms of. This chart shows that normally, bond yields average about 3 percentage points above inflation. Right now bond yields are actually below the level of inflation (which means the market expects inflation to fall). But the Phillips Curve is not the best way to understand inflation. Monetary policy, not economic strength, is the cause of inflation, and the Fed has been pretty easy for a long time. If the economy continues to grow, look for the market to worry more and more about inflation. This relief rally has resulted in higher gold and oil prices, higher interest rates, and a weaker dollar, all signs that inflation is alive and well.

Now that the market is much less worried about a financial market implosion that leads to an economic collapse, it's turning its attention back to what I've been worrying about all along: inflation. Standard thinking (inspired by the Phillips Curve) says that if the economy is very weak, inflation will fall. That's why the bond market hasn't been too worried about $900 gold and $100 oil, because the weak economy would presumably take care of the inflation problem that these are symptoms of. This chart shows that normally, bond yields average about 3 percentage points above inflation. Right now bond yields are actually below the level of inflation (which means the market expects inflation to fall). But the Phillips Curve is not the best way to understand inflation. Monetary policy, not economic strength, is the cause of inflation, and the Fed has been pretty easy for a long time. If the economy continues to grow, look for the market to worry more and more about inflation. This relief rally has resulted in higher gold and oil prices, higher interest rates, and a weaker dollar, all signs that inflation is alive and well.

Relief rally

Stocks are up 8% from yesterday's lows, 2-yr Treasury yields are up 75 bps, and credit spreads are down sharply. So far the government hasn't done anything except to curb short-selling and announce a plan to socialize the remaining costs of the housing crisis sometime in the future. That tells me that this crisis wasn't fundamental or systemic. There was a relatively easy fix out there, and what it did was to remove the fear of an imminent financial market implosion. We've still got to wait awhile to see the details of the plan, and we've got to wait to see if the economy is getting better or worse. So there will be plenty of time for reversals and surprises. The VIX index is still above 30, so the storm hasn't completely passed. But I think that with time we'll see the economy doing slowly better, and by the time the RTC solution gets put together, it might not even be necessary.

Thursday, September 18, 2008

California home prices plunge, another good sign

Home sales in California surged 13.6% as median home prices plunged 35% in the year ending August, according to DataQuick. Almost half the sales were foreclosure sales. Buyers are coming out of the woodwork. Prices are getting back to reasonable levels. My nephew is a mortgage broker in the Inland Empire and says he's never had it so good. The market is clearing and homes are becoming more affordable. That's great news (for everyone except those that paid too much for their homes and/or refinanced near the peak). It will be a long time before we see another real estate bubble in California.

Households are still in decent shape

Just to keep things in perspective, here are the results of the Fed's calculations of household net worth as of the end of June (just released today). This is a very big-picture look at what's going on in the economy. Yes, there has been some deterioration in the past year, but there's nothing here that sticks out as way out of kilter. Even after a decline of about 5% from its peak last September, net worth was up over 40% from the lows of the 2001 recession. Debt increased only 3.5% in the past year. Even if we make aggressive assumptions about the ongoing decline in nationwide housing prices and recent stock market losses, household net worth by the end of this year should be at least $51 trillion, fully 30% above the low 2002 lows. It's been very painful, but it's still progress.

Just to keep things in perspective, here are the results of the Fed's calculations of household net worth as of the end of June (just released today). This is a very big-picture look at what's going on in the economy. Yes, there has been some deterioration in the past year, but there's nothing here that sticks out as way out of kilter. Even after a decline of about 5% from its peak last September, net worth was up over 40% from the lows of the 2001 recession. Debt increased only 3.5% in the past year. Even if we make aggressive assumptions about the ongoing decline in nationwide housing prices and recent stock market losses, household net worth by the end of this year should be at least $51 trillion, fully 30% above the low 2002 lows. It's been very painful, but it's still progress.Interesting update: The total wealth of the Forbes 400, the poorest of which is worth $1.3 billion, adds up to $1.57 trillion, or about 2.8% of the total net worth of U.S. households.

Positive developments

Well, I said this couldn't go on much longer, and it didn't even last a day. News that the government is considering some sort of RTC type solution for the subprime crisis sent bank stocks sharply higher. Gold gave up all its gains as people began to reassess their fear that bank failures were going to be massive. The VIX has dropped back to 34, and 10-year Treasury yields have jumped 11 bps. That leaves the VIX/10-yr ratio at 9.8, substantially below its high this morning. There will be plenty to worry about in coming days, though, since creating another RTC won't be the work of one day, and the details will likely be in flux for awhile. But it does look like the worst of the panic is behind us.

Another measure of fear

Here's another look at just how bad things are. This chart is a ratio of the VIX index to the 10-year Treasury bond yield. When things are really bad, the VIX is high and the bond yield is low. People are scared to own stocks, and instead prefer the safety of Treasuries. When you add to this the fact that consumer price inflation is 5% and Treasury bond yields are only 3.4% (giving you a negative real yield), you see that people are so frightened that they are willing to lose money (in real terms) in order to seek safety. The other thing you see in this chart is that these periods of fear are fleeting. Let's hope that's the case this time also.

Here's another look at just how bad things are. This chart is a ratio of the VIX index to the 10-year Treasury bond yield. When things are really bad, the VIX is high and the bond yield is low. People are scared to own stocks, and instead prefer the safety of Treasuries. When you add to this the fact that consumer price inflation is 5% and Treasury bond yields are only 3.4% (giving you a negative real yield), you see that people are so frightened that they are willing to lose money (in real terms) in order to seek safety. The other thing you see in this chart is that these periods of fear are fleeting. Let's hope that's the case this time also.

Fear and trembling update

Things are pretty scary out there. The VIX index is up close to recent highs. The news is uniformly bad. Gold is up from $750 to just over $900 in the space of a week. Yields on 3-mo. T-bills are just about zero. Very difficult to know how this will work out, but this sort of action can't go on much longer.

Things are pretty scary out there. The VIX index is up close to recent highs. The news is uniformly bad. Gold is up from $750 to just over $900 in the space of a week. Yields on 3-mo. T-bills are just about zero. Very difficult to know how this will work out, but this sort of action can't go on much longer.Update: The VIX briefly rose above 100 in the Oct. '87 stock market crash. That marked the bottom.

Wednesday, September 17, 2008

Putting the bear market in context

It's been ugly this year, but this chart puts it into a long-term perspective (last data point as of today's close). We've seen a lot worse. And, barring a global catastrophe, stocks are likely to resume their uptrend before too long. The real ugly time to own stocks was in the 1970s. Those were the days of Nixon's dollar devaluation, double-digit inflation, and soaring interest rates. This banking crisis may be unique and painful, but the U.S. and world economies are in better shape today than they were then.

It's been ugly this year, but this chart puts it into a long-term perspective (last data point as of today's close). We've seen a lot worse. And, barring a global catastrophe, stocks are likely to resume their uptrend before too long. The real ugly time to own stocks was in the 1970s. Those were the days of Nixon's dollar devaluation, double-digit inflation, and soaring interest rates. This banking crisis may be unique and painful, but the U.S. and world economies are in better shape today than they were then.

Housing construction can't shrink much further

Residential construction has been cut way back. New housing starts are now about as low as they've ever been. This probably isn't the exact bottom, but we must be getting close. Further declines can't do much to damage the economy anyway, since residential construction is now a very small part of total activity. At this low level of new home construction, the excess inventory of homes will definitely decline, thus eventually strengthening the housing market. The excesses of the past are clearly being worked off. The system is fixing itself.

Residential construction has been cut way back. New housing starts are now about as low as they've ever been. This probably isn't the exact bottom, but we must be getting close. Further declines can't do much to damage the economy anyway, since residential construction is now a very small part of total activity. At this low level of new home construction, the excess inventory of homes will definitely decline, thus eventually strengthening the housing market. The excesses of the past are clearly being worked off. The system is fixing itself.

Now it's a banking crisis

The public is terrified that banks are going to fail, which is why the demand for safe havens is exploding: gold is up over $100/oz. in the past few days, and the interest rate on 3-mo. T-bills has dropped to zero (actually, 0.1% according to Bloomberg as I write this). And of course stocks are down to new lows, and credit spreads are sharply wider. This now approaches a classic crisis of confidence in the banking system.

A problem like this can't be solved by lowering the Federal funds rate (but you can't rule out the possibility that the Fed would be compelled to do just that if things get worse). For now, the government is going to have to take some action which shores up confidence directly. And they are probably going to have to socialize a good portion of the real estate-related losses that have not already been written off. Raising the FDIC deposit insurance limit would help, as would establishing another RTC, as suggested by Brady, Ludwig and Volcker in today's WSJ. And the Fed will have to "lend freely" as recommended long ago by Walter Bagehot.

More disturbing is the increasing (though still relatively small) likelihood that some of these losses will be absorbed via the printing press. Higher inflation is a back-door way of dealing with too much debt. That's the Argentine recipe for getting out of a debt mess: run the printing presses and use the money to pay off debt holders. Higher inflation not only reduces the burden of the debt but in this case it might also slow or stop the decline in housing prices, and that would short-circuit this crisis directly. The risk of higher inflation would help explain the sudden rush to gold (though I think it's mainly a bank panic for now). No one has proposed an Argentine-style solution yet, and even if they did it would most likely be disguised amidst a blizzard of other measures, loans, and/or bailouts.

So, the solution to this problem will probably involve 1) the socialization of remaining real estate losses, and 2) more inflation than most people expect. On this latter point, I would note that the TIPS market is assuming that inflation is set to plunge from its current 5% level, averaging a mere 1.5% over the next five years. If you think inflation could be higher than that (which seems likely to me), then TIPS should be your investment of choice if you're looking for a safe haven.

A problem like this can't be solved by lowering the Federal funds rate (but you can't rule out the possibility that the Fed would be compelled to do just that if things get worse). For now, the government is going to have to take some action which shores up confidence directly. And they are probably going to have to socialize a good portion of the real estate-related losses that have not already been written off. Raising the FDIC deposit insurance limit would help, as would establishing another RTC, as suggested by Brady, Ludwig and Volcker in today's WSJ. And the Fed will have to "lend freely" as recommended long ago by Walter Bagehot.

More disturbing is the increasing (though still relatively small) likelihood that some of these losses will be absorbed via the printing press. Higher inflation is a back-door way of dealing with too much debt. That's the Argentine recipe for getting out of a debt mess: run the printing presses and use the money to pay off debt holders. Higher inflation not only reduces the burden of the debt but in this case it might also slow or stop the decline in housing prices, and that would short-circuit this crisis directly. The risk of higher inflation would help explain the sudden rush to gold (though I think it's mainly a bank panic for now). No one has proposed an Argentine-style solution yet, and even if they did it would most likely be disguised amidst a blizzard of other measures, loans, and/or bailouts.

So, the solution to this problem will probably involve 1) the socialization of remaining real estate losses, and 2) more inflation than most people expect. On this latter point, I would note that the TIPS market is assuming that inflation is set to plunge from its current 5% level, averaging a mere 1.5% over the next five years. If you think inflation could be higher than that (which seems likely to me), then TIPS should be your investment of choice if you're looking for a safe haven.

Tuesday, September 16, 2008

What if Obama loses?

This was unthinkable just a few weeks ago, now it's not. Richard Miniter does a great job exploring the consequences:

Obama is ... straight out of a Democratic dream factory; his being touches and excites every element of the vast and varied Democratic party coalition. He and his wife are activist lawyers; he is connected to both the 1960s radicals (Ayers et al) and the Daley Democrats who beat them up in 1968 (Michelle’s father was a Daley ward heeler). Obama is not only an environmentalist-surfer from Hawaii, but he is a better public speaker than Keanau Reeves. He is an author-intellectual yet he can emote. He is telegenic and fit, yet has one perfect flaw: he is struggling in his fight against cigarettes. He has no problem with his wife earning more than he does while he decries the fact that, on average, women earn less than men in the some positions. He is Christian, but not born-again. And so on. He is an absolutely perfect incarnation of the liberal dream.

If Obama is rejected by voters, liberal activists will face a difficult moment. Mondale, Dukakis, Gore, Kerry, sure. There was something wrong with them. A failure to connect. A remoteness. A coldness felt in some feathers of the left wing. Bill Clinton was an electoral success, but something about him didn’t sit right. The drama. The southerness. The welfare reform. The zaftig valley girl. Activists can understand why voters might have punished Hillary for the sins of Bill.

But Obama? He is perfect.

A rejection of Obama can only mean one of two things: a rejection of the 1960s formulation of liberalism (the current formulation, alas) or that America is deeply racist. Too many of them will go for the second hypotheses.

Too many think that elections turn on identities, not ideas.

If Obama loses–and it is still a big ‘if’–too many liberals will fail to heed the message that voters have been sending them since 1981. Seventy percent of the country is tired of 1960s liberalism. Indeed many find the hippie vision frightening: A country too ashamed of itself to fight its enemies, too unsure of itself to praise its own history, govern its children or corral its criminals, and too resentful of the rich to allow the economy to make more of them.

The Fed does the right thing by not easing

Congratulations, Ben, you've shown some courage under fire. Yes, the financial situation is distressing and the economy is weak, but inflation is clearly a problem and the dollar needs help. You've got your eye on all these problems. Relative to what the markets were expecting, you gave more weight to inflation and the dollar than to the economy. This is a real break from your past behavior and one that I think is very encouraging.

The Fed can (and did this morning) inject funds into the banking system at any time to relieve liquidity shortages. They don't need to make money cheaper in order to do this.

The market may be disappointed by this lack of Fed action, but this could be one of those many times when the market's knee jerk reaction is the wrong one from a long-term perspective. I bet the market will come back to its senses and eventually applaud this (lack of) move.

The Fed can (and did this morning) inject funds into the banking system at any time to relieve liquidity shortages. They don't need to make money cheaper in order to do this.

The market may be disappointed by this lack of Fed action, but this could be one of those many times when the market's knee jerk reaction is the wrong one from a long-term perspective. I bet the market will come back to its senses and eventually applaud this (lack of) move.

Ok, this is a serious crisis, and that's good

The VIX index, the measure of Wall Street's panic, rose this morning by enough to qualify this as a very serious problem. That's of course bad, but it's a good thing because it means that a great number of people have tried very hard to avoid risk (e.g., by buying put and call options, by selling, by hoarding cash) and so now they can sit back and wait for things to settle down.

The VIX index, the measure of Wall Street's panic, rose this morning by enough to qualify this as a very serious problem. That's of course bad, but it's a good thing because it means that a great number of people have tried very hard to avoid risk (e.g., by buying put and call options, by selling, by hoarding cash) and so now they can sit back and wait for things to settle down.In other words, the signs of panic and desperation are abundant, and sufficient for this to be the peak of the crisis. It needn't go much further, because this crisis is still limited to housing and banking. The basic problem is simple: people bought a lot of housing at inflated prices with borrowed money, and it's now going bust. There's no quick and easy solution to this problem, since the Fed would have to ease so massively as to reflate everything and thus stop the decline in prices. So we are unlikely to get rid of the problem soon, no matter what the Fed does today (I would not ease if I were Bernanke). Meanwhile, the market is dealing with the consequences of the problem. Housing prices are getting marked down and the market is clearing. Surely the financial markets have priced in and digested the great majority of the real estate losses. This can't go on forever and we've probably seen the worst.

Throughout all this housing price implosion, people have made the mistake of thinking that wiping out a big chunk of real estate wealth would have a huge negative impact on the economy, but it hasn't. They continue to worry about this, only now in spades. The economy is weak, but not dangerously so. Life goes on quite normally for most people. There are no systemic problems such as tight money or higher taxes or tariff wars to deal with this time. These are the classic economy killers Art Laffer always talks about.

The Fed holds a lot of the blame for all this. Easy money in the 2002-2005 period gave a boost to leverage strategies, housing prices, and all things physical. They've been trying to recapture the love, so to speak, by cutting interest rates, but it hasn't helped much, and that doesn't surprise me. You can't dial up inflation at will, it takes time and effort. Still, the CPI ex-energy rose 3.1% in the past year, and rose at a 3.4% rate in the past six months. This is an ongoing, but relatively moderate reflation that is making its way through the economy. Every day that helps narrow the gap between housing prices and reality; that lessens the pressure on housing prices to decline, by making them more affordable.

I don't agree with Gross that this will be a deleveraging implosion that leads to a massive or ongoing deflation. Once the losses are taken and the dust settles, life will go on as normal. We've got quite a few years of easy money in the pipeline that is waiting to show up in prices in coming years. Thank goodness oil has come down below 100! That takes a lot of pressure off, but $92 oil is still a sign that inflationary pressures are in the pipeline. Oil today is still 15% above where it was a year ago.

Monday, September 15, 2008

It doesn't matter whether the Fed cuts rates tomorrow

Futures markets are suggesting a strong probability that the Fed will announce another cut in its target for the Federal funds rate tomorrow, which would bring it down from 2.0% to 1.75%. Presumably they would do this in order to provide support to the economy at a time when financial markets are in distress. I don't think it really matters whether they cut or not. For one, rates are already very low relative to inflation (see chart). Monetary policy is already about as easy as it gets. Second, I don't believe that reducing interest rates makes the economy stronger. If anything, it might exacerbate the inflationary problems which have contributed to get us in this mess in the first place. The seeds of the housing bubble were sown back in the early 2000s, when the Fed held short-term rates very low for an extended period. This encouraged financial players to use too much leverage, and it encouraged builders to build too many homes, and it encouraged buyers to bid prices up too high. Eventually this bubble had to burst.

Futures markets are suggesting a strong probability that the Fed will announce another cut in its target for the Federal funds rate tomorrow, which would bring it down from 2.0% to 1.75%. Presumably they would do this in order to provide support to the economy at a time when financial markets are in distress. I don't think it really matters whether they cut or not. For one, rates are already very low relative to inflation (see chart). Monetary policy is already about as easy as it gets. Second, I don't believe that reducing interest rates makes the economy stronger. If anything, it might exacerbate the inflationary problems which have contributed to get us in this mess in the first place. The seeds of the housing bubble were sown back in the early 2000s, when the Fed held short-term rates very low for an extended period. This encouraged financial players to use too much leverage, and it encouraged builders to build too many homes, and it encouraged buyers to bid prices up too high. Eventually this bubble had to burst.The only way that the Fed could take direct action to solve the housing problem (which is now essentially a problem of falling prices), is to pump so much money into the economy that it lifts all prices. Like a rising tide that lifts all boats, a massive infusion of money would lift all prices. Housing prices might stop falling as other prices, including incomes, rose. Housing could quickly become more affordable, and inflationary policies would once again heat up the demand for physical things, since those are what hold their value during times of inflation.

A cut of 0.25% in the funds rate is not going to be the key to unlocking a flood of new money. But it could weaken demand for dollars (since easy money undermines the long-term value of a currency), and that would be a lot worse than any amount of stimulus that lower rates might imply. Don't forget also that the Fed can only control short-term interest rates; the rest of the yield curve is determined by the market.

If I were Bernanke, I would not want to cut rates tomorrow. I would want to signal to the market that my next move would be to raise rates, because I'm more concerned about inflation and the value of the dollar than I am about the solvency of some investment banks.

A financial crisis, not an economic crisis

Brian Wesbury today reminds us in this article that the crisis playing out on Wall Street is mostly financial in nature, and does not necessarily pose a serious risk to the economy. I've been pointing out in most of my posts here that although the economy is a bit on the weak side, we have not yet slid into a recession, and Brian agrees. Similarly, while subprime lending has virtually ceased to exist, more traditional forms of lending are proceeding apace. As Brian notes, and I agree, it is critically important that today's problems are not the result of any drastic change in government policies. Credit is contracting to a subset of borrowers, but overall credit conditions remain healthy. Some banks are going out of business, but there is no shortage of dollars in the world, and interest rates remain relatively low compared to inflation (see chart). Taxes have not gone up, and despite Gov. Schwarzenegger's worst efforts, California has apparently resolved its budget crisis without raising taxes. World trade continues to expand, and exports are the brightest star in the U.S. economy.

Brian Wesbury today reminds us in this article that the crisis playing out on Wall Street is mostly financial in nature, and does not necessarily pose a serious risk to the economy. I've been pointing out in most of my posts here that although the economy is a bit on the weak side, we have not yet slid into a recession, and Brian agrees. Similarly, while subprime lending has virtually ceased to exist, more traditional forms of lending are proceeding apace. As Brian notes, and I agree, it is critically important that today's problems are not the result of any drastic change in government policies. Credit is contracting to a subset of borrowers, but overall credit conditions remain healthy. Some banks are going out of business, but there is no shortage of dollars in the world, and interest rates remain relatively low compared to inflation (see chart). Taxes have not gone up, and despite Gov. Schwarzenegger's worst efforts, California has apparently resolved its budget crisis without raising taxes. World trade continues to expand, and exports are the brightest star in the U.S. economy.Update: This financial crisis can be likened to the impact of a neutron bomb which creates an electro-magnetic pulse that fries electronics but leaves buildings and people intact. Paper wealth has been destroyed, because lenders were careless and many used too much leverage. But the homes that were built remain, and most people are still working; job losses to date haven't yet approached the level of a recession or even a mild one. The paper wealth that has been vaporized represents claims on future cash flows. Those claims don't represent any new growth or new investment, they simply mean that cash will not flow from some homeowners to some lenders in the future. But the underlying source of all cash flows—work, investment, risk-taking, job creation—remains intact.

The market is very nervous, but it's not panic (yet)

The implied volatility of equity options (as measured by the VIX index) is pretty high today, as the chart shows, but it hasn't reached extreme panic levels. Nevertheless, significant rises in this index usually occur at times when the market is very nervous or very worried, and that is a time when equity prices tend to be their lowest. Peaks in the VIX index, in other words, signal periods of crisis, and more often than not these are times to be buying rather than selling. If you have the nerve. Things could still get worse, but the news of Lehman's failure ranks as awfully bad coming as it does in the wake of some other very large failures.

The implied volatility of equity options (as measured by the VIX index) is pretty high today, as the chart shows, but it hasn't reached extreme panic levels. Nevertheless, significant rises in this index usually occur at times when the market is very nervous or very worried, and that is a time when equity prices tend to be their lowest. Peaks in the VIX index, in other words, signal periods of crisis, and more often than not these are times to be buying rather than selling. If you have the nerve. Things could still get worse, but the news of Lehman's failure ranks as awfully bad coming as it does in the wake of some other very large failures.In one encouraging sign, just 45 minutes into the trading session the VIX has fallen from an opening high of 31 to 28.5.

Friday, September 12, 2008

Federal finances are not in terrible shape

The federal deficit is rising, but relative to the size of the economy it is far from being a significant problem. Most people are blaming runaway spending for the deficit, but that's not actually the case. The rebates this summer did help to widen the deficit, and spending growth in recent years has somewhat outpaced growth in the economy, but it's not earth-shattering. As these charts make clear, the biggest reason the deficit has gone up this year is a decline in revenues. That in turn owes much to the slowdown in the economy and the losses related to subprime securities. It's not unusual at all for revenues to slump when the economy slumps. What is unusual, and very much counter-consensus, is that spending relative to the economy has not surged. Note the surge in spending as a % of GDP that occurred prior to other recessions. George W. Bush is getting a bit of a bad rap on this.