However, while monetary policy isn't currently threatening, trade wars are indeed a cause for concern. Trump is engaged in brinkmanship with China, in an attempt to force China to respect intellectual property rights and reduce punitive tariffs on some US exports to China. Today, some Chinese officials threatened retaliatory tariffs on US exports, particularly grains, and that raised the stakes, which in turn explains why the market fell meaningfully. Nobody benefits from tariff wars, particularly a tariff-imposing country's own consumers. If a tariff war were to escalate—heaven forbid—the results could be devastating, as happened with the Smoot-Hawley tariffs and the Great Depression. But everyone could benefit from freer and fairer trade, and I think that's what Trump is aiming for. If we've learned anything about Trump in the past year or so, it's that he is a clever negotiator who scares people from time to time. He undoubtedly believes that you've got to take great risks to achieve great results.

While we nervously await the outcome of the Trump vs. China war of nerves, it's helpful to remember that the growth fundamentals of the US economy are "beautiful," to borrow a phrase. Corporate tax cuts have set the stage for a significant pickup in investment, jobs growth, and real incomes, but it will take awhile before we see the results. The outlook is promising, but we're sweating through a lot of uncertainties at the moment. I think it pays to remain optimistic, but it's clear that uncertainty and risk are a bigger factor today than they have been in more than a year.

Here are some charts which are relevant to my comments above:

Chart #1

Chart #1 is number one on my Recession Watch list. It shows that recessions have always been preceded by a severe tightening of monetary policy. That tightening in turn consists of 1) real short-term interest rates of 3% or more, plus 2) a flat or inverted Treasury yield curve. Currently, real rates are still unusually low, and while the yield curve has become a lot less steep in recent years, its current slope is consistent with continued growth. The curve is positively sloped because the market believes the Fed will indeed raise rates in coming years, though not excessively.

Chart #2

Chart #2 compares the real yield on 5-yr TIPS (red line) with the real Fed funds rate (blue line). The former is effectively equal to what the market believes the latter will average over the next five years. Thus, the market currently expects only a modest amount of monetary policy tightening for the foreseeable future. That is normal, and it is consistent with the slope of the nominal Treasury yield curve.

Chart #3

Chart #3 shows how real yields (blue line) have risen gradually and in line with a modest strengthening of real GDP growth. It also suggests that if economic growth were to accelerate meaningfully (e.g., 3-4%), then we should expect to see real yields move up to at least 1.5-2.0%.

Chart #4

Chart #5

Industrial production is booming, both here and in the Eurozone, as Chart #4 shows. And it's not just utilities, as Chart #5 shows: after subtracting utility output from the IP data, we see that manufacturing output has in increased meaningfully in the past year, after several years of only modest gains.

Chart #6

Billings at major architectural firms have also picked up in the past year, as Chart #6 shows. There is a lag of at least 9 months between a pickup in billings and the resultant pickup in construction, so this is a good leading indicator of better news to come in the commercial construction sector.

Chart #7

Chart #7 compares an index of truck tonnage (orange line) with the S&P 500 index (white line). I like the truck tonnage index because it is a fairly contemporaneous measure of the physical size of the economy]Both have improved significantly in the past year or so, and both have dipped of late.

Chart #8

Skeptics call Chart #8 the "mis-" leading indicators, since this series doesn't do a good job of anticipating important changes in the economy. It's best thought of as a good contemporaneous indicator. In any event, the Leading Indicators index is up 6.5% in the year ending February, and that is a pretty good indication that we are still in the growth phase of the current business cycle.

Chart #9

When talking about debt and deficits, it is imperative to express them as a percent of economic activity. Chart #9 does just that, showing the federal deficit as a percent of nominal GDP. Although the $706 billion that the government has borrowed in the past year sounds like a lot, it is a smaller percentage of GDP than the Reagan deficits were in the 1980s. Another thing to note about this chart is that the burden of deficits (their size relative to GDP) always declines during periods of growth, while it always increases during periods of economic weakness. Growth is the key variable when talking about debt and deficits. I've explained before that the deficit has been increasing of late not because the economy has been weak, but rather because people have been anticipating tax reform and consequently accelerating expenses and postponing income. Now that tax reform is not only a reality but significantly pro-growth, we should see faster economic growth, more jobs, and a bigger tax base that should ultimately result in an improving fiscal situation (i.e., a declining deficit/GDP ratio).

This is not to ignore the long-term risks to the fiscal outlook, which center around the growth of entitlement spending. We're not yet on a collision course with fiscal disaster, but that remains a major source of concern for the long haul. In the meantime, more growth would mitigate those concerns.

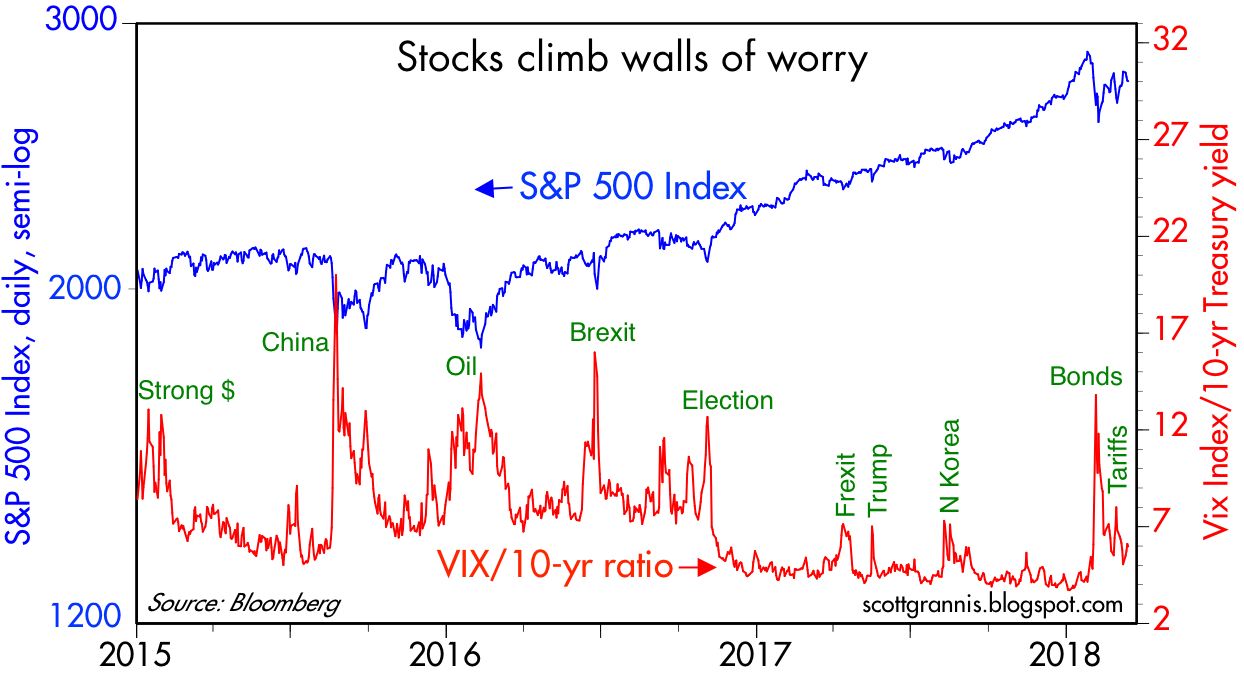

Chart #10

Chart #10 shows how market worries (as proxied by the red line, which is the ratio of the Vix "fear" index to the 10-yr Treasury yield) have affected stock prices. The current "wall of worry" is not too high; we've seen much worse in recent years.