The chart above shows the PE ratio of the S&P 500, with the latest datapoint as of Friday: at 21.1, it is definitely above its long-term average of just under 17, so it's easy to look at this and conclude that the market is pricing in good news.

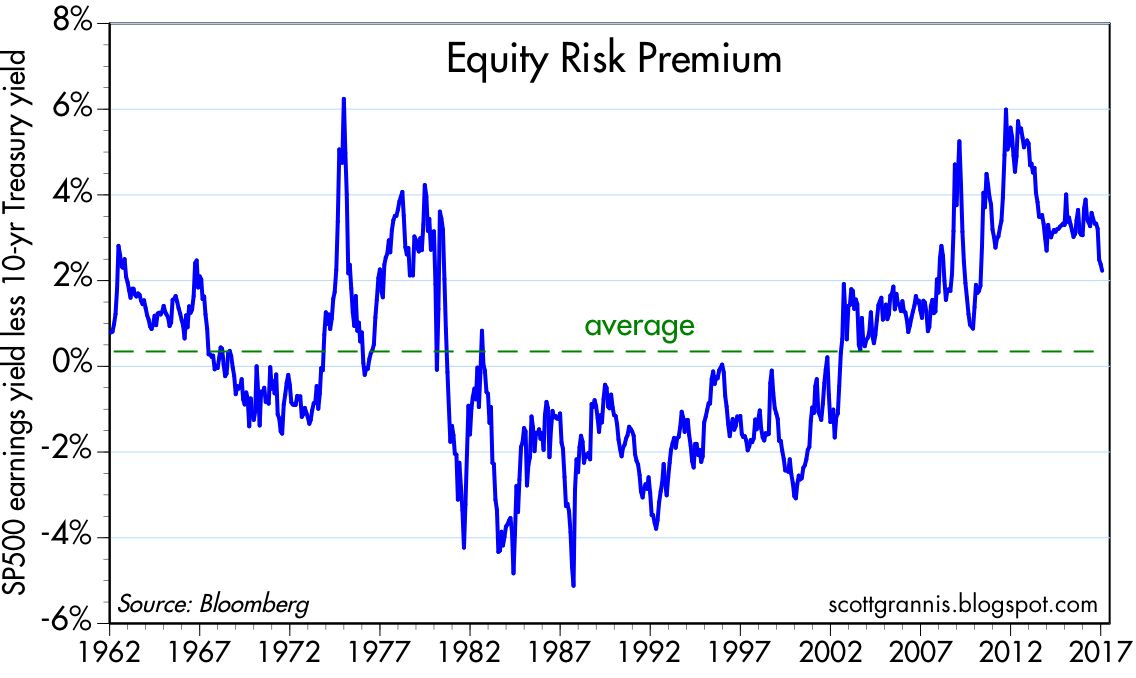

But PE ratios can't be viewed in a vacuum. The chart above compares the earnings yield on stocks (EPS divided by price, or the inverse of PE ratios) with the yield on 10-yr Treasuries, which are a proxy for long-term risk-free rates. The greater the difference between these two, the less optimistic the market is. When the difference is negative, as it was in the 1980s and 1990s, the market is quite optimistic, since investors are willing to accept a very low yield on stocks relative to their risk-free alternative, because they are confident that stocks will appreciate by more than the difference. Today, it's almost the opposite; investors are unwilling to take on the risk of stock even though their yield is about 200 bps higher than the yield on 10-yr Treasuries.

Fourth quarter GDP growth was weak, at 1.9%, and growth over the most recent four quarters was also weak, only 1.9%. Looking back to the beginning of the current economic expansion, the annualized growth of real GDP has been a modest 2.1%, which is significantly below its long-term trend of about 3.1%. The chart above shows how significant this 1% annual shortfall in growth has been: the gap between where the economy is today and where it could have been if growth had been 1% per year stronger, is about $3 trillion. If this had been a normal recovery, real incomes on average would be about 15-17% higher today than they actually are. No wonder this has been a disappointing economy, even though it has been growing rather steadily for over seven years.

The chart above compares the real yield on 5-yr TIPS to the 2-yr annualized growth rate of real GDP. It's likely not a coincidence that real yields on TIPS have been zero to negative for a number of years, while the economy has managed real growth of only 2%. Think of the real yield on 5-yr TIPS as the risk-free real growth rate that investors can lock in; it should rarely be equal to or higher than the real growth of the economy (which is best proxied, I would argue by the 2-yr annualized growth of GDP), because if it were, then TIPS would be the best risk-adjusted investment in town.

Typically, as the above chart also shows, the real yield on TIPS tends to be somewhat less than the prevailing real growth rate of the US economy. That is as it should be: risk-free real yields should normally be lower than the real returns available from a growing economy, because the latter are uncertain. When the economy was growing 4-5% per year in the late 1990s, real TIPS yields were 3-4%. Now that the economy is growing 2%, real TIPS yields have rarely been higher than 0.5%. Real yields on 5-yr TIPS are going to have to rise meaningfully before it can be said that the market has turned optimistic about the future of the US economy.

What has the economy been so sluggish for so long? The chart above is one answer: business investment has been unusually weak. Without investment it's very difficult to grow. Without investment in new plant and equipment, new software, etc., worker productivity is likely to be low. And indeed, productivity has been a meager 0.5% or so per year, on average, for the past 5-7 years.

The chart above tells the same story: capital goods orders, a proxy for business investment, have been very weak. In real terms, they haven't growth at all since the mid-1990s.

The chart above compares the real and nominal yield on 5-yr Treasuries, and the difference between the two (green line), which is the market's expected rate of CPI inflation over the next 5 years. Note how nominal yields have jumped in the past few months while real yields have been relatively flat. All that's happened, as far as the bond market is concerned, is that inflation expectations have risen from 1.3% last summer to now just over 2.1%, and most of that rise can be explained by higher oil prices.

Higher inflation expectations could arguably be a healthy development, if only because the market seems to have lost its fear of deflation. But if inflation expectations were to continue to rise, that would soon become problematic, since it would mean that the Fed was falling behind the inflation curve, and sharply higher interest rates would soon become inevitable.

UPDATE: The chart below compares the real Fed funds rate to the real yield on 5-yr TIPS. The real funds rate is today's real risk-free rate, while the 5-yr real yield on TIPS can be thought of as what the market expects the real funds rate will be in 5 years. The blue line is usually above the red line, which is the normal state of affairs because it means the market expects the Fed to "tighten" in the future. But when the red line exceeds the blue line, it means the market senses the economy is weak and will require Fed easing in the future. Note that the red line exceeded the blue line in advance of the past two recessions; this is just another way of saying that tight Fed policy plus an inverted real or nominal yield curve is a good warning sign that a recession may be on the horizon.

The market won't be "optimistic" about the future of the economy unless and until the 5-yr real yield on 5-yr TIPS moves significantly higher. Because that will be the best indication that the market senses the economy is going to improve significantly and that the Fed will therefore be accelerating its rate hikes.