The demand for money—as measured by the ratio of M2 to nominal GDP—currently stands very near to an all-time, eye-popping high (see Chart #1). The turmoil and fears which characterized the Covid-19 era caused the public to seek out and hold trillions of dollars of extra cash, and the Fed correctly obliged this demand for money and money equivalents by greatly expanding its balance sheet— transmogrifying notes and bonds into T-bill equivalents (aka bank reserves). (I've explained this all in detail over the course of many previous posts.) Conveniently, increased savings on the part of a terrified and sheltering public provided most—if not all—of the money that Treasury borrowed to fund Covid relief spending.

Chart #1

Chart #2

But as Chart #1 suggests, the surge in money demand has passed. Confidence is returning and the economy is regaining lost ground. It stands to reason that the demand for money should begin to decline, and it has already declined, as we see in Chart #2, driven mainly by a sharp rise in nominal GDP. This is quite likely to continue; the main question going forward is how much of the increase in nominal GDP will be real and how much will be inflation.

Chart #3

Chart #3 shows the daily volume of airline passengers (white) screened by TSA, with the magenta line being the 7-day moving average. Notice the sharp increase in air traffic in the past two months. Compared to the levels which prevailed 2 years ago at this time of year, air traffic is now down only 40%, whereas at the lows of last April, air traffic had plunged by an astounding 96%. With the rapid pace of vaccinations and increasing signs of optimism, there is every reason to expect air traffic to grow rapidly in coming months and the economy to grow as well.

The resurgent demand for air travel almost certainly is driven in large part by increased confidence. And with increased confidence, the rationale for the public continuing to hold a huge portion of their annual incomes in cash (i.e., the public's demand for money) surely is fading. But since the Fed has taken no steps to reverse its note and bond purchases, the M2 measure of money supply can't simply evaporate. And with the recently passed Covid relief bill, deficit-funding spending is going to ratchet up once again, which could add yet more money to the financial markets, especially since the Fed plans to continue to its purchases of notes and bonds.

Unwanted money can't disappear, but it can fuel an expanding economy and it can bid up the prices of other assets.

Chart #4

Chart #4 provides some clues as to how this works. The bars represent the current yield on a variety of investments. The green line is the market's expected average annual increase in the CPI over the foreseeable future (about 2.3%); think of that as the average increase in the prices of all goods and services over the next 5-10 years. Owning cash, short-term Treasuries or mortgage backed securities is very likely to give you a loss in terms of purchasing power. On the other hand, yields on real estate trusts, high-yield debt, emerging market debt and the S&P 500 promise to deliver a purchasing power gain. Unwanted money (much of which is held in very short-term investments such as T-bills, bank deposits and 2-yr Treasury notes) will naturally want to seek out the much more attractive returns on just about all other assets. And as prices for other assets rise, their yields will decline.

This is another way of saying that a tsunami of unwanted cash likely is going to lift the prices of just about everything, and that is another way of saying we are going to see more inflation in the years to come, UNLESS the Fed reverses course. Which they have promised not to do for at least another year and a half.

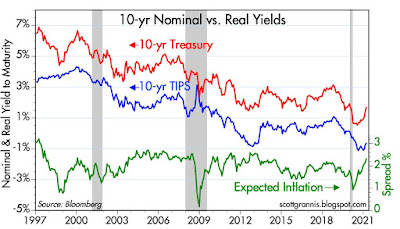

Chart #5

Chart #5 shows us the bond market's way of expressing the view that inflation is likely to average about 2.3% per year for the foreseeable future. The difference between real and nominal Treasury yields gives you the market's expected rate of inflation. Note that most of the increase in inflation expectations of late has come from a rise in nominal Treasury yields. Real yields are still very low.

Chart #6

Chart #6 shows how 2-yr real yields on TIPS have a strong tendency to track the growth rate of real GDP over time. That real yields are currently so low means that the market either does not have a lot of confidence in future growth prospects, and/or the market is still very risk averse (meaning that people are willing to pay extremely high prices for the relative safety of TIPS). Going forward, we are likely to see real yields rise as long as the economy demonstrates that it has the ability to grow by at least 1-2% per year for the next several years.

Chart #7

Chart #7 gives us a long-term view of the evolution of the Treasury yield curve (using 2- and 10-yr yields as the classic reference points for short and long-term interest rates). Bear in mind that short-term rates are heavily influenced by both the Fed's monetary policy target and the market's demand for safe assets. The yield curve has steepened noticeably since last summer, mainly due to rising long-term yields, which in turn have been driven by expectations that the economy will improve enough to allow the Fed to raise short-term rates in the future. This is a healthy development, since very low yields are a sign of a very weak and risk averse economy. There's no reason yet to worry that higher yields will derail the ongoing equity market rally.