There is no shortage of things to worry about.

That's a phrase I have used several times over the past decade. I used it as a foil to argue that since the market was quite cautious (and nervous), then a surprise downturn or selloff wasn't a serious risk. Recessions usually happen when nearly everyone is feeling optimistic. Today there again is no shortage of things to worry about, and the market is within inches of its all-time high. Most disturbing, however, is that neither the Fed nor the administration nor Congress nor the bond market are very worried about inflation. Inflation and all its nasty consequences are, arguably, big things to worry about today.

Fed policy, as laid out in today's FOMC minutes, is amazingly blasé about the risks of higher inflation. The Fed currently plans to begin "tapering" its purchases of Treasuries and mortgages sometime next month, and to finish tapering by mid-2022. That's not a tightening of monetary policy; it's only making policy less accommodative over a prolonged period. Actual tightening—which would consist of draining reserves (i.e., selling bonds) and/or raising the interest rate it pays on reserves (i.e., higher short-term interest rates)—won't begin until sometime late next year.

The market has apparently agreed that this is a sensible course of action. Inflation expectations embedded in bond prices are somewhat high, but still a relatively tame 2.75% per year (average) over the next 5 years. The bond market is currently pricing in one or two 25 bps "tightenings" by the end of next year (i.e., short-term interest rates of roughly 0.4% to 0.5%), and a 1.5% fed funds rate 3 years from now. By any standard, that would be a supremely gradual pace of monetary tightening. But at a time when inflation is at levels not seen in over 30 years?

This is almost certainly an unsustainable situation. The Fed and the bond market are almost certainly underestimating the risks of higher-than-expected inflation.

How do I know this? It's all about incentives. Today, the incentives to borrow are huge. Short-term interest rates are below the current level of inflation and will likely remain so for at least the next year. (Even 30-yr fixed rate mortgages are lower than the rate of inflation.) Smart investors and consumers won't find it hard to arbitrage these variables. In fact, the process is already underway. You simply borrow money and buy anything that is a productive asset and which also has roots in the nominal economy (e.g., commodities, equities, farms, factories, cars). Leverage is your friend and ally in a high-inflation, low-interest-rate world.

How does one place a bet on an asset (in this case the dollar) that is expected to decline in value (because of inflation eroding its purchasing power)? You sell it if you own it, or you sell it short (you borrow it and then sell it). You buy it back when inflation settles back down and/or interest rates rise to a level that is greater than inflation. One way to "short" the dollar is to simply borrow dollars. And a common way to do that is to get a loan from a bank. And when the bank lends you money, the bank can actually create the money it lends you, which in turn expands the money supply. Banks are uniquely able to create money, provided they have sufficient reserves on hand to collateralize their deposits. Since the banking system currently has upwards of $3 trillion in "excess" reserves, thanks to the Fed's gargantuan purchases of notes and bonds, banks have an almost unlimited ability to increase their lending.

So it's not surprising that the M2 money supply has expanded at an unprecedented rate over the past 18 months, a time in which the Fed has bought almost $3 trillion of notes and bonds and bank deposits have swelled by some $5 trillion. And it's also not surprising that in the past six months consumer price inflation has posted a 6-7% annualized rate of growth—a rate last seen in late 1990.

As for Biden, his approval rating is now down to an abysmal 38%. His administration has committed a series of blunders, most notably with the Afghanistan withdrawal. His top priority now is to pass two bills chock full of new social spending and new taxes which he preposterously claims will cost the economy "zero." Meanwhile, inflation has risen to multi-decade highs, yet both the administration and the Fed keep insisting it's just transitory. Things will almost certainly get worse if trillions of new taxes and spending, additional layers of bureaucracy, and hundreds of billions of dollars of new handouts and subsidies get lavished on the middle class. My good friend and talented artist Nuni Cademartori sums it up in this cartoon:

As the battle in Congress over Biden's "Build Back Better" agenda rages, I would urge everyone who thinks this agenda will actually help the economy grow and prosper to read the

recently released study by the Texas Public Policy Foundation in collaboration with my good friend, Steve Moore of the Committee to Unleash Prosperity.

The key findings:

• The cost of the Biden Build Back Better plan spread across two bills will reach $6.2 trillion over the next decade.

• The higher tax rates on corporate income, small business income, capital gains, and so on will raise the cost of capital and reduce national investment and the capital stock.

• Compared to baseline growth, the negative impact of these taxes over the next decade will result in 5.3 million fewer jobs, $3.7 trillion less in GDP, $1.2 trillion less in income, and $4.5 trillion in new debt.

While I'm on the subject of Steve Moore, whom I've known since the mid-1980s, I will once again recommend you read and subscribe to the Committee to Unleash Prosperity's free

daily newsletter. I read it every day, as do more than 100,000 citizens and Washington policymakers. (One of his recent issues featured Nuni's cartoon, and another featured some of my recent charts.)

In the study mentioned above you will find details on a plethora of Biden's tax proposals (e.g., a 12.5% payroll tax on all income over $400K, a reduction in the estate tax exemption of $8 million, and an increase in the top marginal tax rate to 65%) and their likely negative impact on the economy and employment. It's frightening to think that the people who came up with these proposals apparently believe that the overall impact of BBB will be stimulative. Have they no common sense? Here's a fundamental supply-side truth: when you tax productive activity and success more, you will get less of it. And when the government borrows trillions only to redistribute the money to favored groups and industries, you get a weaker, less efficient economy. And you also risk boosting already-high inflation.

I'll wrap things up with some updated charts and commentary:

Nothing illustrates better the supply-chain bottlenecks that currently plague the global economy than Chart #1. Used car prices have literally skyrocketed; in inflation-adjusted terms, used car prices are higher than they have ever been. In nominal terms they are up over 50% since March '20.

Chart #2 shows how almost half of small businesses in the US report paying higher prices. The last time this occurred was in the 1970s. It's hard to escape a higher inflation deja vu conclusion.

Chart #3

As Chart #3 shows, bank reserves are very near their all-time high. The vast majority of these reserves are "excess" reserves, meaning they are not required to collateralize bank deposits. Banks thus have enough reserves on hand to collateralize an ungodly increase in deposits via new lending (i.e, money creation). If the Fed doesn't increase the interest rate it pays on these reserves by enough to make them more attractive, on a risk-adjusted basis, than the interest rate banks can expect to earn on new lending, bank lending will surely continue to expand, and that will fuel a prolonged expansion of the money supply and ever-higher inflation.

Chart #4 shows the 6-mo. annualized rate of growth of the CPI (including the ex-energy version). I think this is a fair way to measure what's happening now, since we are well past all the distortions of last year and the turmoil earlier this year. Inflation by this measure hasn't been this high since late 1990.

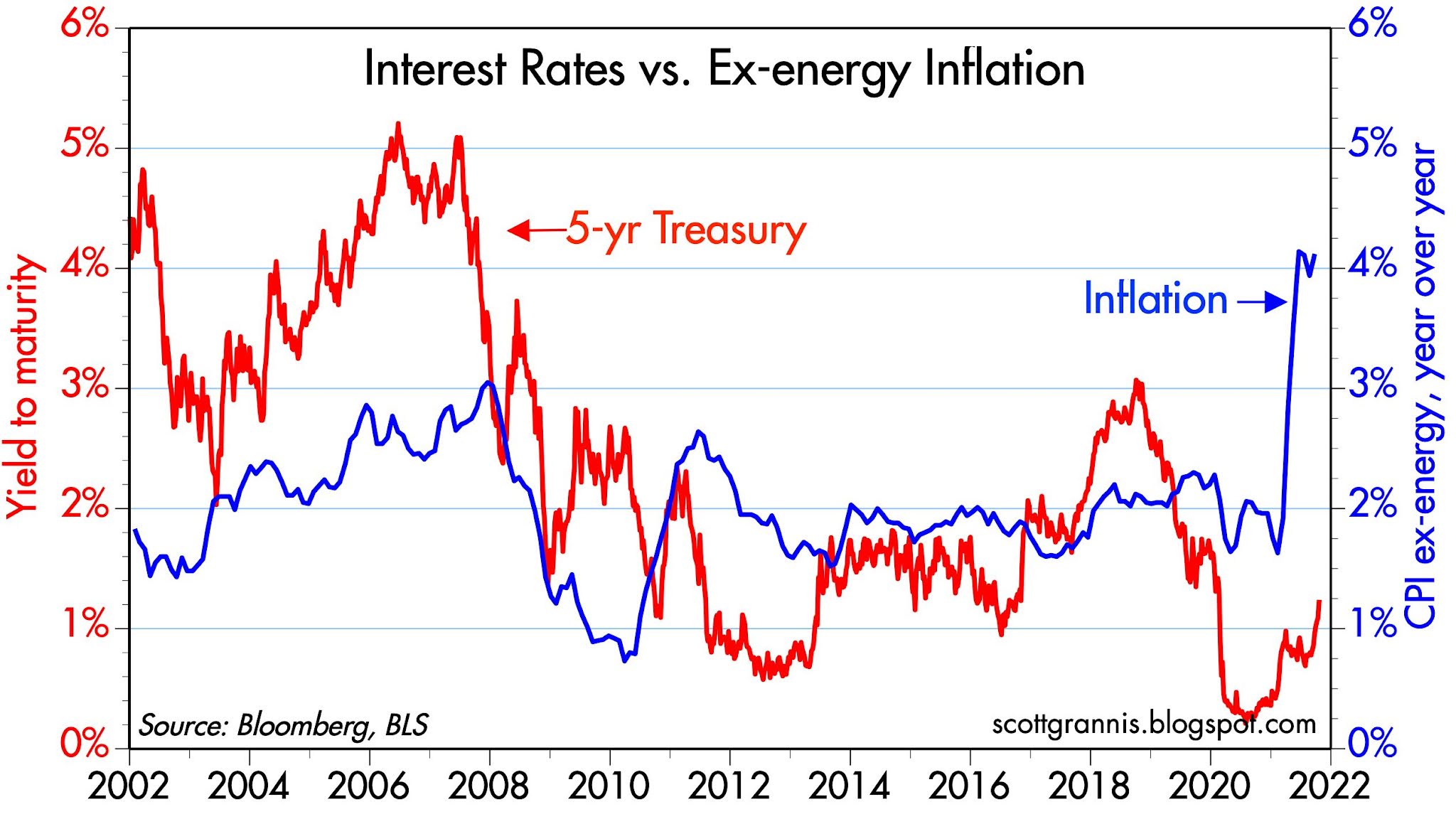

Chart #5

Chart #5 compares the year over year growth in the CPI (I'm being conservative with this) to the level of 5-yr Treasury yields. Yields haven't been this low relative to inflation since the 1970s. Recall what happened back then: millions of households made a fortune borrowing money at fixed rates and buying houses. Negative real interest rates cannot be sustained for long, mainly because of the incentives they create to borrow and buy.

Chart #6 is an updated version of the one featured in Steve Moore's newsletter. It's important to note that the multi-decade trend rate of M2 growth is 6-7% per year. This has been blown away in the past 18 months. If the public tires of holding $3.8 trillion more in bank deposits than they normally would at this time, that's a tsunami of money that could float higher prices for nearly everything in the next year or so. It's also worth noting that M2 has been growing at a 10-11% annualized rate so far this year.

What worries me the most right now is how this all sorts out. The Fed seems determined to avoid even the semblance of tightening for the next 12 months. Yet if inflation turns out to not be transitory as they currently expect, how long will it be before policy becomes tight enough to threaten the economy's health?

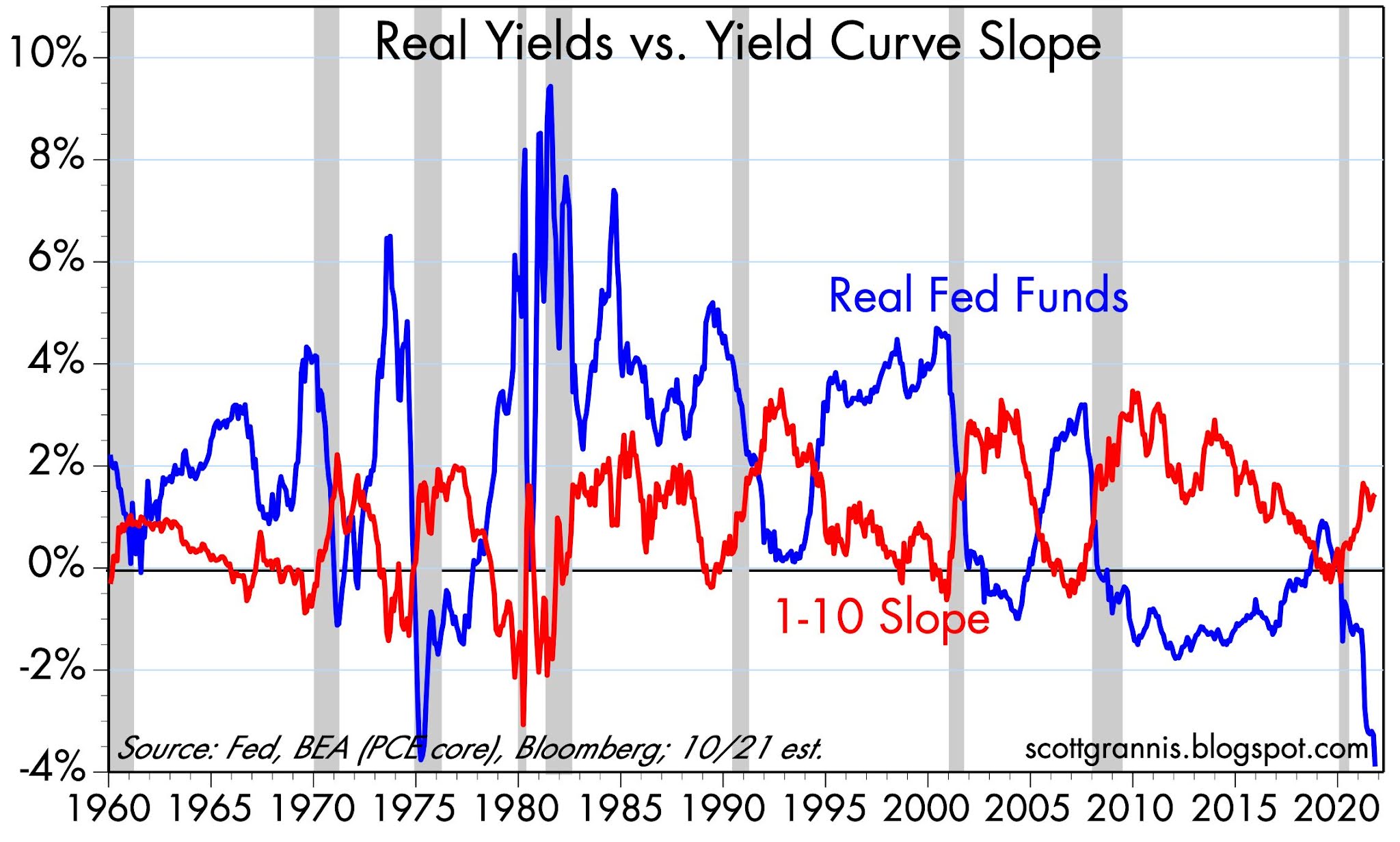

Chart #7

Chart #7 provides some historical context which may help answer that question. Note that every recession on this chart (shaded bars), with the exception of the last, was preceded by 1) a flat or negatively-sloped Treasury yield curve, and 2) a very high real Fed funds rate. Both of those conditions confirm the existence of very tight monetary policy that was intended to keep inflation pressures at bay. Neither condition is in place today, however, which strongly suggests that monetary policy poses no threat to the economy at this time.

Past Fed tightenings, however, were different from what a tightening would look like today. To really tighten policy, the Fed would have to 1) start raising the interest rate it pays on reserves, and 2) start draining reserves by selling bonds. It might take years to get rid of all the excess reserves, however, and no one knows for sure how the economy will respond to higher short-term rates in the presence of abundant reserves—that's never happened before. In the past, the Fed simply drained reserves until they were in such short supply that the banks were willing to pay ever-higher interest rates in order to acquire enough of them to collateralize their deposits. A scarcity of reserves led to a liquidity shortage, and high real borrowing costs led to bankruptcies and weak investment. Eventually, economic growth ceased, and the inflation cycle was broken.

The dilemma for investors: we might be years away from a return to these conditions, so selling risky assets right now might be premature. And, by the way, holding cash is a guaranteed way to lose money. But how long can you wait, knowing that another economic collapse looms on the horizon?

In the meantime, the prospects for Biden's Build Back Better lollapaloosa are declining by the day, thankfully, and the spreading disarray in Washington only makes that more likely. I'm willing to bet that if any of his bills survive, it will be in greatly reduced form, and thus much less damaging to the economy. Just letting the economy sort things out on its own would be a great relief to everyone, in my view.

Nobody said investing was easy. There are a lot of things to worry about these days. But I wouldn't panic just yet. The next year or so might be likened to watching a train wreck in slow motion.