The reflation theme is alive, well, and prospering. Today, Fed Chairman Powell himself told the world that.

He sees a long road to recovery, he's not concerned about rising prices, and he plans to keep short-term rates low for a long time.

And it's not just stocks that are benefiting. Here is a modest collection of charts that I'm currently tracking with interest:

Chart #1

As Chart #1 shows, copper prices are exploding to the upside even as gold prices hold relatively steady. The world is rebuilding and speculators are jumping on the commodity price bandwagon. The dollar is somewhat weak, but I think the chart tells us that a weaker dollar is not telling the whole story. Today the dollar is only slightly weaker than its average over the period of this chart, but copper prices (adjusted for inflation) are much higher than their average. Gold, by the way, is not looking good even though the world is reflating. That can only suggest that gold hit an all-time high several years ago in anticipation of what we are seeing today.

Chart #2

Chart #2 compares 10-yr Treasury yields (red line) to the ratio of copper to gold prices (a good proxy for global growth expectations). This reaffirms the view that we're in a reflation. Not only are inflation expectations rising, but industrial commodity prices are too, as is construction activity in general. 10-yr Treasury yields are up because the world is feeling a little less concerned about the economy remaining weak forever. More inflation and more growth mean higher yields, it's that simple. And yields have plenty of room on the upside (i.e., bonds are a terrible investment these days).

Chart #3

Chart #3 updates a chart I haven't featured for a long time. Given all the weakness in the economy in the past year, I was surprised to see that commercial real estate prices last December reached a new all-time high. Malls may be empty and downtown businesses and restaurants may be abandoned, but no one is giving up on the idea that we'll get back to normal before too long. Easy money, low borrowing costs, and the fact that life is not going to go dormant anytime soon all add up to the expectation that the physical side of the economy is going to be picking up for the foreseeable future. SPG (Simon Property Group) has more than doubled since early November.

Chart #4

Chart #4 is a perennial classic that shows how equities are performing relative to gold prices. Typically, equities underperform in times of hardship and outperform in times of plenty. This ratio has a ways to go before it returns to the 5-handle highs last seen in 2000.

Chart #5

Chart #5 is also a long-time favorite that I haven't featured in awhile. As I see it, the equity market tends to lead truck tonnage (a proxy for the health of the physical economy). Equities are effectively pricing in a full recovery and the eventual attainment of new all-time highs for GDP. This may worry the bears, however, but I would argue that the economy won't be at serious risk of a downturn until the Fed tightens by a ton, the yield curve flattens, and real yields rise significantly. And we're a long ways from those things happening.

This is not to say, however, that I see real GDP growth averaging more than 2% per year in the years to come. Things are definitely improving right now, but I think one's enthusiasm should not go unchecked. The policies favored by the Biden administration are not going to optimize economic health or maximize economic growth. And a multi-trillion dollar "stimulus" plan is going to do just the opposite of stimulating the economy. I'm hoping that clearer head prevail in Congress. Beware economic "stimulus" plans: they never work and they usually just make things worse. The government simply cannot spend money more efficiently than letting people spend their own money.

Chart #6

Chart #6 shows the makeup of inflation expectations that are priced into the bond market. Inflation is expected to average almost 2.5% per year for the next 5 years. We've seen something like this before, but nothing much worse than that. (I think we'll end up seeing worse.) Note especially the extremely low level of real yields (blue line). This can mean two things: 1) the market expects economic growth to be sluggish for the foreseeable future and that means low real yields in general, and/or 2) since TIPS are the safest and surest way to protect against inflation (TIPS pay a coupon equal to their real yield plus the rate of CPI inflation), and since the Fed is pledging to keep short-term rates very low for a long time, the Fed is effectively putting an artificially low cap on the level of all real yields, which forces investors to pay artificially high prices—and receive artificially low real yields in exchange—for inflation hedges. I'm inclined to think that both forces are working at present.

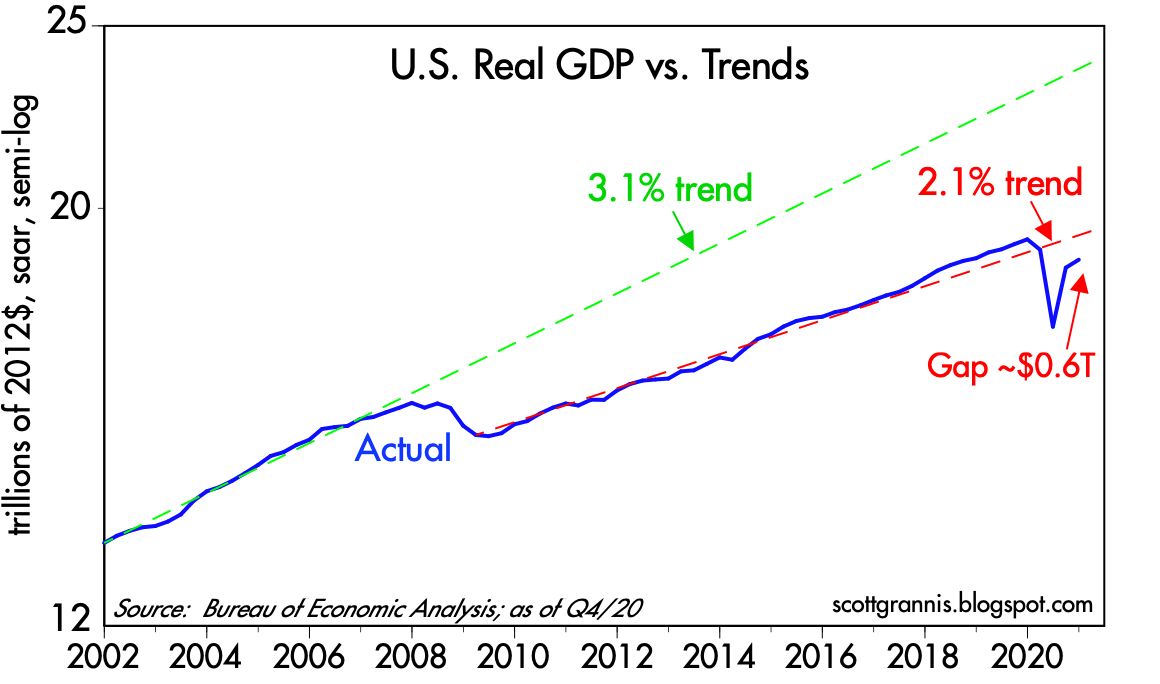

Chart #7

Of course that also suggests that one should keep their hopes for the future from running wild. Stocks can't go up like this forever.

UPDATE: (Feb 25th) As Chart #8 shows, capital goods orders (the precursor of future productivity gains and thus an excellent leading indicator of economic growth) have surged in recent months, far exceeding expectations and breaking out of a prolonged slump. This is perhaps the most optimistic chart in my basket.

Chart #8