Today the FOMC announced that it did not see any reason to further increase the supply of bank reserves (i.e., there would be no QE3). But as a concession to those who still worry deeply about the economy, the FOMC did decide to extend its "Operation Twist" by buying another $267 billion of longer-term Treasuries while simultaneously selling an equal amount of shorter-term Treasuries.

Stocks initially sold off, Treasuries rallied, and gold fell, all signs that the market was disappointed there would be no more quantitative easing. But as often happens, the market's initial reaction was subsequently reversed. What that tells me is that, upon reflection, the market has decided that the Fed did the right thing. We don't need more QE to get the economy going.

The one thing the Fed could do to help would be to more forcefully explain to the world that monetary policy cannot stimulate growth. The Fed has done just about all it needs to do in order to accommodate the world's massive appetite for dollar liquidity; doing more would only risk inflation and a weaker dollar. To get the economy moving again we need stimulative fiscal policy, and by that I mean government spending cuts, a broadening of the tax base via the elimination of deductions, loopholes, and tax credits, and a lowering and flattening of tax rates.

Just in case you missed it, do read David Henderson's essay today which explains how

gigantic cuts in government spending at the end of WW II not only failed to tank the economy but actually led to a huge boom. The Keynesian view that cuts to government spending would hurt the economy are unfounded. With government spending now close to record post-war levels, reducing the burden of government would unleash powerful private sector forces that would almost surely boost economic growth.

To recap the state of monetary policy, the chart above shows bank reserves, which are currently about $1.6 trillion following the Fed's two rounds of quantitative easing.

Of that total, $100 billion of reserves are currently "required" in order to back bank deposits per our fractional reserve banking system. That leaves $1.5 trillion which are "excess" reserves sitting idle on the Fed's balance sheet. Banks have been slow to use the massive amount of reserves the Fed has dumped into the system via its purchases of MBS and Treasuries. That's mainly because reserves are now functionally equivalent to 3-mo. T-bills, since the Fed now pays banks interest on the reserves they hold. In fact, reserves are even better in a sense than T-bills, because reserves earn an interest rate of 0.25% while 3-mo. T-bills only yield 0.09%. Banks are holding reserves because they want to bolster their balance sheets and because they are still very risk averse. The extremely low level of yields on T-bills is proof of the intense demand for safety. Indeed, if the Fed had not engaged in quantitative easing there would have been an acute shortage of risk-free dollar liquidity, and that could have precipitated a global depression and/or deflation.

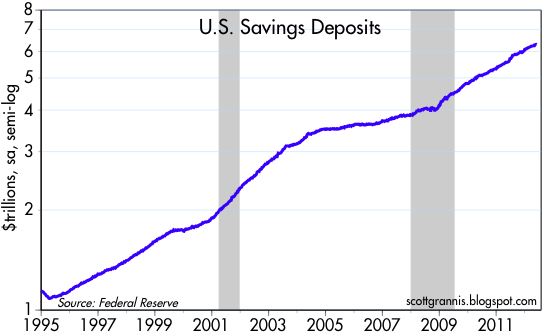

The entire world in fact is still very risk averse, and you can see that in the huge growth of savings deposits in U.S. banks, which now total some $6.3 trillion. Savings deposits have surged from a low of 10.6% of GDP in 1982 to over 40%, and much of that increase has occurred over the past 4 years, as can be seen in the chart below, which shows the ratio of savings deposits to nominal GDP.

Other signs that the Fed has done enough quantitative easing can be found in the following charts.

2-yr swap spreads are back to normal, a sign that the banking system is functioning normally and systemic risk is low. Banks have access to all the liquidity they need; the world is not starved for liquidity.

Not only is there no shortage of dollars, there is actually a relative

abundance of dollars in the world to judge by the dollar's weakness relative to other currencies.

As the first of the two charts above shows, credit default swap spreads have fallen significantly from their recession highs, a good sign that credit conditions have improved dramatically. Spreads are still somewhat elevated, however, but I would argue that has little to do with Fed policy and everything to do with the ongoing Eurozone financial crisis and the extremely low level of short-term Treasury yields, which in turn is being fueled by the world's extreme risk aversion. As the second of the two charts above shows, corporate bond yields are about as low as they have ever been: credit spreads are still elevated because low corporate yields are being compared to exceedingly low Treasury yields. The fact that the world is happy to buy investment grade corporate debt with yields as low as 3.8% suggests the outlook for corporate profits is excellent. And indeed, corporate profits are very close to record-high levels, both nominally and relative to GDP.

On the margin, gold and commodity prices are off their recent highs. Many analysts argue that this is a sign that the Fed has inadvertently tightened policy and that more quantitative easing is therefore necessary. My interpretation is somewhat different: I think the recent "weakness" in gold and commodity prices is a sign that monetary policy has become "less easy." Gold and commodity prices are still trading at very lofty levels compared to where they were 10 years ago when the Fed first embarked on an ambitious program to easy monetary policy. Monetary policy was indeed tight in the late 1990s and early 2000s, but that's certainly not the case today.

Finally, as this chart shows, forward-looking inflation expectations are not displaying any evidence at all that the Fed is too tight. This chart shows the market's implied 5-yr inflation rate 5 years in the future (i.e., the expected average annual inflation rate five years from now for the subsequent 5 years, as derived from TIPS and Treasury prices; i.e., the expected average inflation rate from 2017 through 2022), and it is right around where it has been for a long time—neither high nor low. This is the Fed's preferred measure of inflation expectations. In the absence of any decline in inflation expectations, such as occurred in late 2008, and in the fall of 2010 and 2011, it would have been very hard for the Fed to justify another round of easing today. If anything, I would note that inflation expectations have

increased slightly this year.