In early 1994, China opted for a monetary policy that targets the value of its currency vis a vis the dollar. This is a legitimate policy option, but very different from the monetary policy that all other major central banks have adopted, which is to target short-term interest rates. In order to manage its exchange rate, China's central bank must buy and sell foreign currency depending on the balance of capital inflows and outflows to their country. If there is a net inflow of capital, the BoC must buy whatever excess of foreign currency there happens to be, thus adding to its foreign exchange reserves while at the same time expanding the supply of yuan in the economy; otherwise, the excess of foreign currency would depress the value of the yuan and violate the peg. Conversely, an outflow of capital would require the BoC to sell foreign exchange and shrink the supply of yuan, thus supporting the yuan. In this manner, capital inflows feed directly into an expanding economy and an expanding money supply.

For the past 18 years, China has experienced an almost relentless and massive inflow of capital. The inflow was so massive that the BoC was ultimately forced to revalue the yuan by 37% in several stages, following its initial 8.72 peg, as reflected in the blue line in the chart above. As China deregulated and privatized its economy, allowing the entrepreneurial energies of the world's most populated country to flourish, the world was quick to see the investment opportunities in China. Investment flows followed, and they were huge. This meant that the BoC had no alternative but to make massive forex purchases (red line in the chart above), and that was a good thing because the abundant supply of yuan this created provided the wherewithal for the Chinese economy to grow roughly 10% per year (in nominal terms, the economy increased a mind-boggling tenfold) as foreign investment inflows financed a booming Chinese economy.

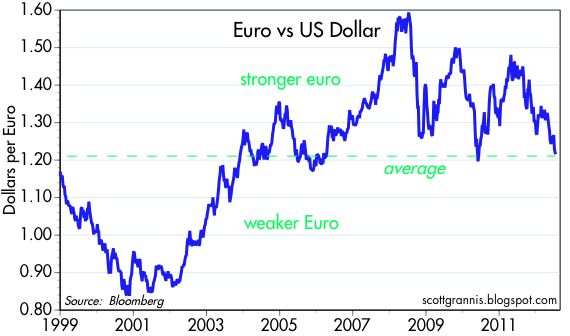

By pegging the yuan to the dollar, China effectively "outsourced" its monetary policy to the U.S., and so it is not surprising that inflation in the two countries is virtually identical, especially now that the economy has had many years to adjust to its currency peg.

The chart above makes it clear that the yuan has been a relatively strong currency since the adoption of its dollar peg. Against a basket of currencies, and adjusted for inflation differentials, the BIS calculates that the yuan has appreciated by over 50% since 1994. Interesting factoid: since 1994, the yuan has depreciated by only 10% vis a vis the mighty Swiss franc, and it is unchanged against the franc for the past 8 years.

Moreover, the fact that reserves and the currency have been flat for the past year tells us that China's capital flows have reached a sort of equilibrium. No longer is there relentless upward pressure to revalue the yuan. Indeed, China could now argue that balanced capital flows are proof that the yuan is no longer undervalued against the dollar. The yuan has perhaps appreciated enough.

Presumably, the BoC could have stopped trying to peg the yuan to the dollar once China's forex reserves had reached some invincible number like $1 trillion. But it seems they wanted to go even further in order to convince the world that the yuan, like their economy, was serious, strong, and here to stay. So now, forex reserves total a little over $3 trillion, most of which is held in the form of dollar, euro, and yen-denominated bills, notes and bonds. Think of those reserves as the collateral backing up China's M2 money supply, which today is equivalent to about $12.5 trillion dollars. By comparison, U.S. M2 is only $10 trillion, and that is "collateralized" by the Fed's holdings of $1.6 trillion of notes, bonds, and MBS.

In the future, China should have no problem accommodating more economic growth with its current level of reserves—the lack of growth in reserves over the past year poses no threat at all to China's ability to continue growth. By simply by lowering banks' required deposit reserve requirement ratio, which is currently 20%, China's banking system can create all the cash and currency needed to support an expanding economy for years to come.

As the above chart suggests, China's galloping growth phase seems to have come to an end. To judge from the evidence of the past year—i.e., no increase in forex reserves and no change in the yuan/dollar exchange rate—no longer does the world in aggregate see obvious bargains in China, or excessive growth, or low-hanging investment fruit. This is likely due to a combination of factors: the yuan's strong performance relative to almost all other currencies; weaker growth in other countries, which translates into weaker demand for Chinese exports; and weaker growth in China, which dampens potential investment returns. Capital inflows have come to a halt because China is no longer the most attractive investment destination in the world.

At the same time as capital flows reach a kind of equilibrium and growth cools, the world senses that the yuan is increasingly unlikely to continue appreciating, and this in turn means that speculative excesses are diminishing. If the yuan is going to be more stable in the future, then it makes less sense to speculate by buying the yuan or by buying Chinese assets. Investors increasingly must focus on things that make economic sense, and less on speculation. This takes some of the froth off of growth, and means that future growth is likely to be more balanced. The prospect of a slower-growing China may dampen one's enthusiasm for global growth in general, but that concern is offset by the likelihood that future growth will be more balanced, less speculative, and thus more durable.

Memo to Mitt: stop bashing the Chinese, please!