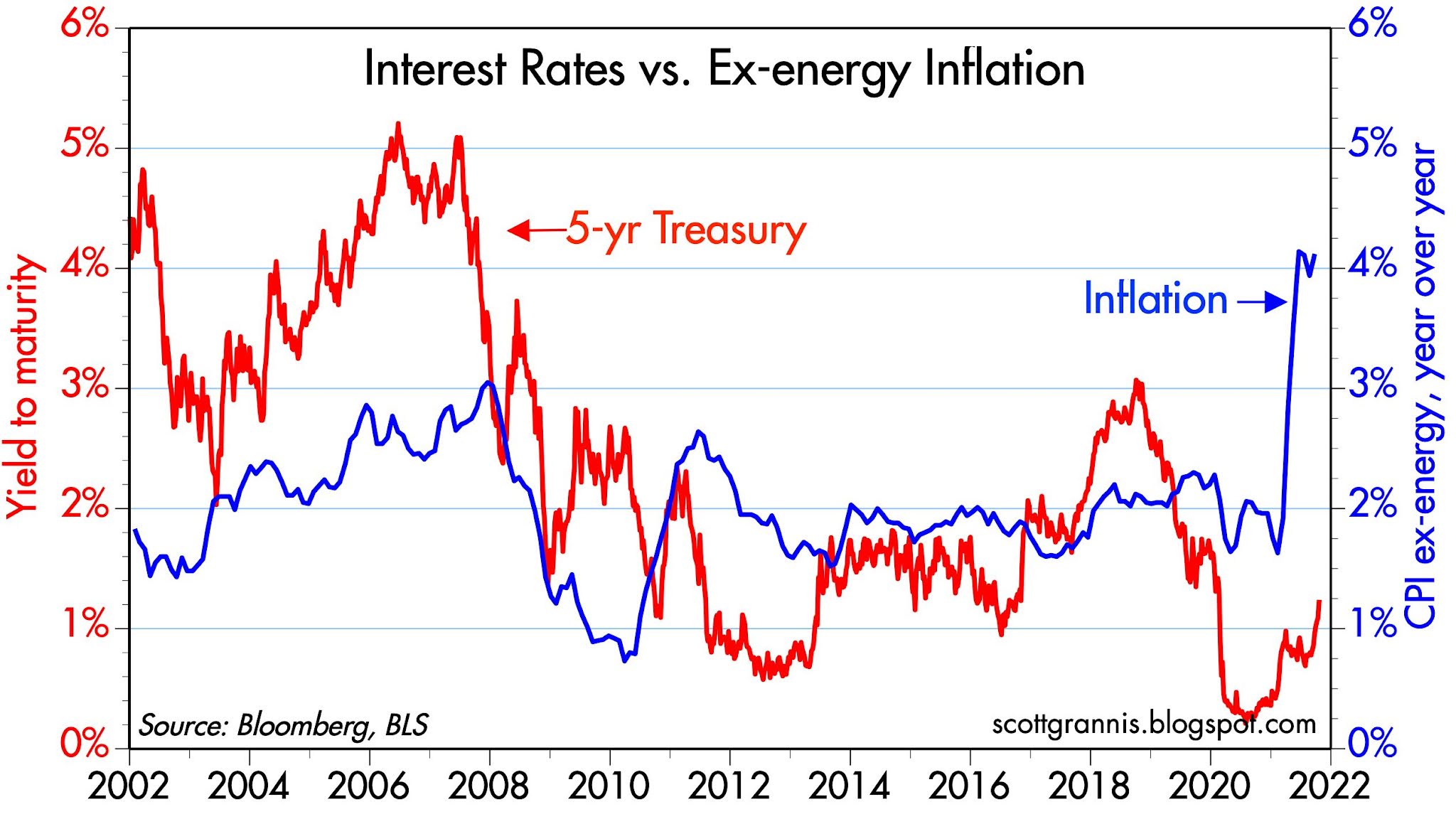

Chart #1

Chart #1 compares the nominal yield on 5-yr Treasuries (which is roughly equivalent to what the market expects that the Federal funds rate will average over the next 5 years) to the ex-energy rate of consumer price inflation (I remove energy because it is by far the most volatile component of the CPI). Despite recent jumps in yields, the chart strongly suggests that the level of yields is still way below what it "should be" given the current level of inflation. But yields are moving in the right direction.

I've been making the point of late that negative yields (i.e., nominal yields below the rate of inflation are unsustainable long-term because the existence of negative yields gives consumers and investors a strong incentive to "borrow and buy." When real yields are negative it pays to short the dollar (i.e., borrow dollars) and go long anything that has roots in the nominal economy (e.g., houses, commodities, cars, equities). This incentive weakens the demand for money, which then leaves the economy with a lot of unwanted money—which provides the fuel for higher inflation. Eventually, rising yields and rising inflation expectations will prod the Fed to ignore the supposed weakness of the economy and begin the long process of normalizing interest rates.

Chart #2

The economy won't be at real risk of higher interest rates until real short-term interest rates are much higher than they are today (probably 3% or more) and the yield curve is much flatter than it is today (currently it is still steepening).

Fasten your seat belts, because we've just begun what could be a long and wild ride to higher interest rates.

25 comments:

Great outlook.

Well, wait and see.

Everywhere you look, capital looking for a home. This seems to be the era of permanent capital gluts. Uncle Sam is a safe home (at least we hope).

I won't be surprised if in two years oil prices are lower, even with the Biden Administration.

BTW, used Volkswagens went up 30% in price in the last year. You should've invested in used cars.

Your whacky uncle with all those old cars in back pasture is a millionaire.

I think a bunch of the long-term fundamentals in the real economy remain under deflationary pressure in developed economies- low birth rates, government intervention/malinvestment causing lower GDP, socio-political/maleducation causing low economic/business IQ in the general population.

The shorter/intermediate-term items caused by the pandemic, and on-going financial nonsense by government actors such as deficits and money-printing (=money for nothing) are causing inflation. These should have reduced impact in the next 12-18 months.

If I had to guess, 2023, looks like the start of some pretty rocky times.

Where are the funds the Fed spent to purchase treasuries? In reserves? Can the Fed sell treasuries back to banks?

What control does Fed have over the M2 funds?

Re "Where are the funds the Fed spent to purchase treasuries?"

Tracing the money through all its stages is beyond my capabilities. But I can say that when the dust settled, this is what happened since the end of Feb. '20: (caveat: this is VERY approximate)

1) The Fed bought about $2.5 trillion of Treasuries and mortgage-backed securities. These were "paid for" by issuing bank reserves to the banking system. In effect, the Fed took in notes and bonds and issued short-term securities in exchange—a swap of short-term securities for longer-term securities, all of which had essentially zero credit risk. Importantly, bank reserves are not "money" because they can't be spent anywhere. Banks hold them as assets (which which in turn are liabilities of the Fed), and they are used to collateralize deposits. Holding more reserves allows banks to create more deposits by lending money that banks alone can create. The Fed does NOT create or print money in this process.

2) Banks created about $5.5 trillion of new money via lending operations, $350 billion of which became currency. Substantially all of that money is still held in the form of currency, bank accounts, savings deposits, etc., all at the retail level.

3) Treasury sold about $5 trillion of debt, the proceeds of which were sent out as checks to various and sundry parties in compensation for the government having shut down the economy.

4) Substantially all of the money distributed by Treasury ended up being saved by the public.

wkevinw - "socio-political/maleducation causing low economic/business IQ in the general population." I've seen this in action, in my conversations with many people, particularly the younger generations, but I've never thought of it this way. Brilliant summation. Thanks!

Scott - I still can't wrap my head around rising interest rates. As I understand it, government debt is mostly short-term, so any increase in rates will increase our debt payments. Since the numbers are cosmic, the increases in debt payments will be huge. In my ignorant pigheadedness, I maintain that the Fed will not raise rates, at least not substantially, because they're manacled to the Federal debt. They're independence has been given away, bit by bit, until they're no longer free to operate as they should.

Please tell me I'm wrong.

K T Cat: For the past several years, Treasury has been selling debt with maturities skewed to longer maturities. That's one reason the Fed has had to step in and reverse that by being longer maturities and issuing short-term bank reserves (which pay interest, so they are in effect T-bill equivalents) in exchange. This was done to satisfy the market's craving for cash and cash equivalents. In short, there was a shortage of short-term securities. The result is that federal debt consists of maturities that are probably relatively evenly distributed across the yield curve.

Know also that current debt service payments relative to GDP are about as low as they have ever been, despite the huge amount of debt (about 100% of GDP) outstanding. This debt service burden will be increasing as interest rates rise, but not quickly. Bear in mind that interest costs will rise because inflation is rising. Rising inflation will result in higher incomes and higher tax collections. So federal tax receipts will rise in tandem with a rising interest rate burden. Net result? A very gradual and prolonged rise in the federal debt service burden. The situation is not catastrophic nor even close to being so. But it is definitely something to worry about long term.

Lots of inflation would be a nice, quick solution from the government's perspective, but it would at the same time be a very painful solution from the public's perspective. That's because inflation imposes a tax on all holders of longer term debt. By allowing higher inflation the government is effectively stealing money from the public. That's why I hate inflation and that's why I hate the Fed when they say that we need higher inflation (i.e., at least 2% for several years). They are pre-announcing the theft of hundreds of billions of dollars from the public.

“Where are the funds the Fed spent to purchase treasuries? In reserves? Can the Fed sell treasuries back to banks?

What control does Fed have over the M2 funds? »

There is some confusion here and it’s helpful to think along a balance sheet model since even supply-siders don’t seem to realize that the US has entered the vicinity of MMT since the GFC, in an accelerating mode since 2016 and the Covid episode.

Let’s look at balance sheets of the Fed, the private parties and the banks (of course the consolidated balance sheets need to balance, at least until the Reserve Act is modified and Fed excess reserves become legal tender).

-The Fed

When doing open market operations, the Fed “buys” government debt (and GSE debt) from institutions (private parties). Then it expands its balance sheet with a new asset, the government debt and with a new matching liability which are reserves deposited at the Fed by commercial banks (then the Fed is like any bank and deposits represent a liability).

-The private parties

With open market operations, private parties’ balance sheets are not expanded. It’s simply an asset swap between a government debt held as an asset to newly created money held as an asset (now counting in M2 and counting as a commercial bank deposit). From end Feb 2020 to now, there were net 2.39T of new deposits and new money (M2) ‘created’ this way although it is not really new ‘funds’ for private parties.

-The commercial banks

With open market operations, the banks’ balance sheet is expanded with new money held as assets (cash assets growth at commercial banks has had a 100% correlation with growth of excess reserves deposited at the Fed) and new deposits as a result of the private parties’ asset swap from the Fed operations.

From this “accounting” perspective, “Banks created [correction: did not create] about $5.5 trillion of new money via lending operations”. Bank lending to private parties for the period account for less than 10% of the new deposits ‘created’.

-----

An interesting part (not discussed in traditional media, even financial media etc) is that the Treasury issued a lot of debt since end Feb of 2020. Some of the resulting increased matching deposits/cash (liability/asset) held at commercial banks (from the Treasury ‘deposits’) has been associated with banks using a lot of this ‘created’ money (asset) to buy (on a net basis) an incremental amount of 1.52T of securities (asset swap), most of which being government debt securities. This effectively means that a lot of the money matched with new treasury deposits at commercial banks by the Treasury was used by banks to buy government debt then held by banks. If this feels like a circular argument or Ponzi scheme, it is because it is. This will work until it doesn’t and is based on the premise of commercial banks’ balance sheet expansion unrelated to underlying real economic activity.

The following shows that Treasury deposits explain the recurrent waves of excess savings but does not discuss how the top 20% (especially the top 1%) benefited mostly for the across-the-board money sprinkling by increasing their cash holdings (and buying government debt…) and by seeing the asset valuations skyrocket as a result of close to zero interest rates while the bottom 80% (especially the bottom 40-60%) used the Treasury subsidies to pay the bills and reduce credit card debt and saw housing becoming even less ‘affordable’.

Personal savings during the pandemic | FRED Blog (stlouisfed.org)

-----

The bottom line is that the present bipartisan trend implies that the government has been growing in importance based on the assumption that it can create productive capacity through capital investments (one of the main premise of MMT). The Fed-Treasury complex has been trying an MMT-like experiment using quantitative easing and may be tempted to go full MMT-mode if given the opportunity (downturn). Then for sure inflation would become a major and sustained issue. i think it is still time to study the numbers and to act accordingly.

Scott - thanks so much for your thorough reply. I think I understand things a bit better now and see how the Fed actually has more room to maneuver than I thought.

A good friend of mine blogged this bit a while back discussing how the US got out of a similar debt trap after WW II. https://www.wcvarones.com/2012/01/silicon-t-bill.html

He also agrees with Scott and suggests that the Fed will deliberately keep inflation in the mid-single-digits to erode the debt.

^The average US government debt maturity is at around 72 months, 31% of Treasury maturities are within 1 year and 54%, within 3 years, so there would be a lag but not that long. Longer term, inflation tends to correlate strongly to interest rates and the key figure to watch (whatever interest/inflation rates prevailing) is the ratio of public debt to GDP. Note: the trend has been poor. Since 2012, the ratio has gone up by 30%, a percentage increase similar to what happened during WW2(!). The financial repression hypothesis seems to be based on the overall complacency ‘rate’ prevailing now.

The comparison to the post WW2 recovery period is fascinating. During WW2, the US economy became publicly commanded and controlled. Concurrently, the private participants in the economy saved and reduced private debt. The US was on the winning side and its geographic and infrastructure integrity had been maintained, with the potential to become the uncontested leader of the global economy. The US was able to transition to an economy driven by private initiatives to meet growing private demand. Yes, there was transitory inflation right after the war and some financial repression but the Federal Reserve, as confirmed by the 1951 Accord, was able to regain some independence and financial repression was only a small component to the gradually decreasing public debt to GDP while private debt was low and on its way to rise significantly to a more ‘normal’ level given the economic possibilities:

https://3yaxqw1hoybz1qcak31ysc9f-wpengine.netdna-ssl.com/wp-content/uploads/2016/09/vague-charts5.png

There were two major contributors to the decreasing public debt to GDP ratio over the three decades that followed: fiscal restraint and high GDP growth (with high productivity) two contributors which are likely to be disappointing for at least some time in the US. After WW2, the US government focused on balanced budgets and, even with the Korean War and other “shocks”, rising expenditures were met with raised federal revenues. President Eisenhower was a true believer in responsible government. But the major aspect was GDP growth, an inclusive kind of growth, around 7% nominal GDP growth over thirty years(!). Of course, then, some of the consensus thinking was that the US was about to fall back into a Depression mode.

Back to the present and using the year 2000 as a baseline, if the previously established long term 2.2 real GDP growth had happened instead of the 1.1% that actually occurred, real GDP per capita would now be 73.5k instead of 58.5k.

As shown below (this has been a long term trend since the 1970s), real GDP growth potential keeps being revised down and even if there are reasons to be optimistic for the longer term, the secular forces driving this trend are still (and for the foreseeable future) firmly entrenched.

https://www.brookings.edu/wp-content/uploads/2021/02/potential-GDP-fig-4.png

If people bet only on financial repression to get out of this excess debt mess, perhaps people should expect more repression than just the financial kind.

PS#1 As of now, the US private debt to GDP is at 130%..

PS#2 According to the CBO, from 2010 to 2020, the U.S. national public debt more than doubled (from $9 trillion to $21 trillion). Yet over the same period the gross interest cost on that debt grew only 26%, from $414 billion to $523 billion and the net interest costs to GDP is back to what it was in the 1970s. What’s wrong with that? i think it’s the result of collective mental regression but who am i to say?

PS#3 It’s not only the longer growth potential that’s eroding. Q3 (and Q4) of this year’s growth expectations are also dwindling like snow melting away on a sunny day.

https://www.atlantafed.org/-/media/images/cqer/research/gdpnow/gdpnow-forecast-evolution.gif?h=356&w=650&la=en

" around 7% nominal GDP growth over thirty years(!)"; "If people bet only on financial repression to get out of this excess debt mess, perhaps people should expect more repression than just the financial kind."; "PS#3 It’s not only the longer growth potential that’s eroding. Q3 (and Q4) of this year’s growth expectations are also dwindling like snow melting away on a sunny day."

Right!

The GDP growth potential in the future is just not enough to "solve" the debt problem. Financial repression worked because it went on at the same time as an historic opportunity to grow an economy after WWII.

I think we go back to trend growth of 1-2% real GDP with a giant debt overhang that future generations will be stuck with.

This is what I have been saying about the economic maleducation of the average citizen. Voters think we'll give free money to anything we think should be "improved" and it will all work out fine. Magical thinking at its "best".

I think what's playing out is the effects of a new economic theory that is well-described by The Grumpy Economist. Here's a key snippet:

Growth

Old view: Scarcity is the default condition of economies: the demand for goods, services, labor and capital is limitless, their supply is limited. ...faster growth requires raising potential by increasing incentives to work and invest. Macroeconomic tools—monetary and fiscal policy—are only occasionally needed to deal with recessions and inflation.

New view: Slack is the default condition of economies. Growth is held back not by supply but chronic lack of demand, calling for continuously stimulative fiscal and monetary policy. J.W. Mason.. said, that “‘depression economics’ applies basically all of the time.”

If slack is the default condition, then supply will always be able to scale up to match demand. We don't need to worry about people producing and shipping things. Yay!

Whoops!

K T Cat: that quote from John Cochrane is excellent. I regard him as one of the best economists living today and I try to read everything he writes.

https://johnhcochrane.blogspot.com/

Sadly, the Democratic Party seems completely ignorant of supply-side fundamentals. That is one of the greatest threats our country faces today: economic ignorance.

Grumpy Economist -- that's funny

Scott is the Happy Economist -- much more pleasant.

er

Nations with a high level of debt in the past have had slow rates of real economic growth than lower debt nations. I see no reason that relationship would have changed.

High levels of debt are often a symptom of reckless government spending. Kind of like the US in 2020 and 2021.

Whatever the problem, the Biden Administration

will somehow find a way to make them worse.

Their motto seems to be:

"What is good for America? -- We will do the opposite."

If you didn't have enough to worry about:

The US daily average COVID death rate in 2021

is +16.9% higher than it was in 2020

(with no vaccines and fewer natural antibodies)

An unbiased person would look at these data

and conclude the vaccines are failing.

More details to support the +16.9% number

(I know +16.9% is hard to believe)

https://electioncircus.blogspot.com/2021/10/the-2021-daily-covid-death-rate-is-169.html

TEOTWAWKI...except the S&P 500 just struck a new all-time zenith. They say Wall Street is forward-looking.

These are the good old days for corporate profits, much higher than even the Reagan days.(Biden gets a no credit for that and Trump a little).

Washington? More guns and butter for the fat and safe.

Cliff Claven: I have no axe to grind.

I look at the numbers on Covid-19 and I can't make heads or tails of anything.

My guess is there should be free vaccinations for anyone who wants one and we drop the matter.

I thought the same thing a year ago.

"Math is a beautiful thing."

Yes there is some math involved but the post is framed to suggest conclusions that are not a balanced and transparent representation of underlying data, if put in proper perspective.

Look at the following:

https://www.kff.org/policy-watch/covid-19-deaths-among-older-adults-during-the-delta-surge-were-higher-in-states-with-lower-vaccination-rates/

Lower vaccination rates in the younger cohorts will result, eventually, in higher rates of breakthrough cases in older cohorts. It's basic and biologic reasoning, uncontaminated by politics.

@Benjamin Cole

Wayne Gretzky, the hockey player, apparently would have said: "Don't go where the puck is, go where the puck will be."

Lower vaccination rates in the younger cohorts will result, eventually, in higher rates of breakthrough cases in older cohorts. It's basic and biologic reasoning, uncontaminated by politics.--Carl

OK...are the number of breakthrough cases high enough to warrant lockdowns and other measures?

I get the sense of goalposts being moved...again.

We are wearing masks, and lockdowning, enacting travel bans, firing some employees, and forcing not-at-risk children to wear masks and get vaccinated...due to breakthrough cases?

Is there any point where we can just go back to normal?

"South Korea is set to gradually phase out coronavirus restrictions starting next month as the vaccination rate rises, joining a list of countries embracing a new scheme of returning to normal life with the coronavirus.

The scheme, dubbed "Living with COVID-19," is set to take effect in early November. It means that COVID-19 will be treated as an infectious respiratory disease, like seasonal influenza, with eased social distancing being implemented."--The Korea Herald

This strikes me as overdue, and the right way to go. Flu can be a killer, cancer can be a killer. Smoking, drinking, we know are killers.

But too much government...and does the federal government ever win a war? Against terrorism, Viet Cong, poverty, drugs, hillbillies in Afghanistan, C-19, etc? These wars are eternal, unless voters rebel....

"OK...are the number of breakthrough cases high enough to warrant lockdowns and other measures?"

OK and i agree with smaller government to GDP.

But the idea is that decisions based on wrong assumptions or weak fundamentals are likely to be of lesser quality (at the individual and collective levels).

Smaller government doesn't mean more stupid government, something that has been forgotten in a bipartisan way and a reason inflation may realllly pick up eventually if the debt/saving imbalance reaches a tipping point.

For some time now, governments and the Fed score their 'successes' in terms of stock market levels. Isn't this weird?

Benjamin: Is there any point where we can just go back to normal?

Not in the foreseeable future. The left has invested too much into the political position of appearing like the "serious experts", and demonizing anything else. It's also been too valuable to mask (pun intended) the failures in virtually every other policy domain. It seems it would take a new administration to put a new narrative on it.

Aside - been paying attention to the inflation discussion here very closely. I took advantage of higher prices to sell some commercial real estate. Also considering taxes will likely go up - in particular for real estate partnerships. But - my selling probably confirms inflation is here to stay. Now what to do with the proceeds....

Randy, it depends where you are. Many states are back to normal. My own California, at least here in San Diego, to a great extent, is back to normal. If you turn off the TV and social media, I think things look a lot more normal.

KT yeah, for me it does seem semi-normal. I was thinking about schools - perpetual masking, closures, coming pressure to vaccinate - I'm semi depressed. Glad I didn't have to raise my kids in this environment.

I think what we're seeing is like an egg going through a snake. A very, very BIG egg. We shut things down for quite a while and now we're trying to go back to full speed. I think that the people who made the decisions to shut us down were familiar with laptops, but not big rigs.

I think that the people who made the decisions to shut us down were familiar with laptops, but not big rigs.--KT Cat

Amen. Elon Musk said that manufacturing is the hardest thing to do, much harder than anticipated. I was in simple manufacturing for 20 years (furniture), and even that was an endless challenge.

Building, farming, manufacturing, transportation--this stuff is hard. But lawyers don't make wealth.

On the keyboard, you make fixes with the mouse. In real life...

DC is a bubble, run by globalists. It shows.

Post a Comment