For the past two months we have been experiencing the fastest and steepest decline in economic activity in the history of this country. Estimates of 2nd quarter GDP range from -31% (New York Fed) to -48% (St. Louis Fed). (Note: these are annualized rates of decline.) I'm going to be optimistic and guess that Q2/20 growth will post a 30% annualized decline, which is equivalent to a 6.8% nominal decline. Meanwhile, the M2 measure of the money supply is on track for something like a 50% annualized rate of increase in the current quarter. The following charts show you what these numbers look like:

Chart #1

Chart #1 shows the actual history of these variables and my estimated values of M2 and nominal GDP for Q2/20. The current disparity between the two is historical.

Chart #2

Chart #2 shows the ratio of M2 to GDP, which is a proxy for money demand. Think of it as you would your personal finances: How much cash and cash equivalents do you want to hold as a percent of your annual income? Since the onset of the Great Recession in late 2007, that value for the average person has increased fully 80% (from 50% to 90%). That's a lot of money being stockpiled, mainly because this has been a rather crazy period in history.

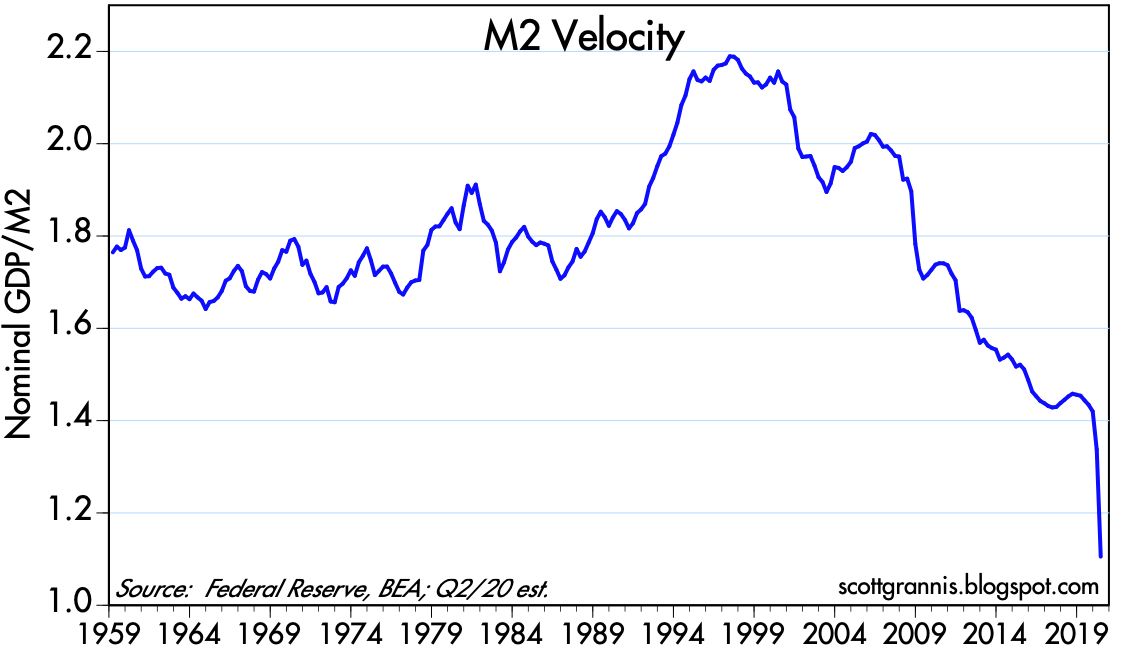

Chart #3

Chart #3 shows the inverse of Chart #2, which can be thought of as the number of times a dollar is spent every year—a proxy for the velocity of money. People today are holding on to their cash like never before.

So M2 has gone way up and GDP has gone way down because the forced shutdown of the economy has caused the demand for money to soar. That's completely natural and predictable. The Fed has done the right thing by expanding the supply of money in order to accommodate the increased demand for money. The fact that inflation expectations, the dollar, and industrial commodity prices have been relatively stable for the past six weeks confirms that the Fed has accommodated soaring money demand, and has NOT been madly printing money. I've made similar arguments quite a few times in the past on this blog. Quantitative easing is NOT stimulus, it's a badly-needed remedy for a huge increase in the demand for money.

But what comes next? With increased signs that the economy is reopening and activity is increasing, it's quite likely that the demand for money will begin to decline as confidence slowly returns. Money that has been socked away in bank accounts is increasingly going to be spent on goods and services. Will the Fed be able to reverse its QE4 efforts in a timely fashion? Will the public's desire to reduce their money balances lead to rising inflation?

I won't be surprised to see restaurants reopening with higher prices on the menu. The government will mandate that the supply of restaurant tables be limited (e.g., maximum occupancy rates of 25% and maybe 50%) at a time when many consumers with pent-up demand will be seeking tables. When demand exceeds supply, higher prices are almost inevitable. Especially since few if any restaurants can be profitable at much lower occupancy rates than they have enjoyed in the past—occupancy mandates will force restaurants to raise prices.

But not everything will be supply-constrained. Airlines are going to have a huge surplus of seats for a long time. Hotels will have a vacant rooms galore. Malls and stores won't be full until the fear of contagion and crowds disappears. But we are already seeing positive signs of improvement which are quite likely to continue.

We've seen the worst of the covid-19 crisis. Looking ahead, the 800-lb gorilla that will dominate the economic and financial landscape for the balance of the year will be the need for the Fed to begin to reverse its massive monetary expansion of recent months. Curiously, I see many analysts worrying that a Fed reversal will jeopardize the recovery. On the contrary, I think it would be very worrisome if the Fed did not realize that they need to "tighten" as the demand for money begins to decline.

28 comments:

I would just point out that velocity has been straight down ever since the GFC. Something is very wrong when animal spirits are this low (and plunging). Perhaps this explains the paltry GDP growth, the lame capex growth, and the pathetic productivity, and all despite massive increases in the money stock. (I'm referring to the last 12 years, not just since Covid reared its ugly head.) The Fed deserves credit for offsetting the decline in velocity with massive increases in money (resulting in weak but positive GDP growth and low but positive inflation). But something is very wrong in our economy when for roughly 12 years this is what we have.

So I'm not misinterpreted, I'm not negative on the market because one should not fight the Fed. But something is very wrong in our economy and has been for a dozen years.

I wish I knew how this ends...

@Grechster I agree, something is wrong. I notice myself beginning to come to terms with the fact that we are not going back to normal.

Scott's been showing us the gap between potential and actual GDP for years. I think it amounted to about 3 trillion USD going into this Corona-mess. Low investments were blamed, and it was said corporate tax cuts would fix it, but it hasn't happened. Not in the US, nor in Europe.

The same goes for the monetary interventions. I understand the argument about QE being about the demand for money, but at the same time it has resulted in central banks holding massive amounts of government debt (about a quarter if all debt here in the eurozone). We now know this was not a one-off because of a once in a lifetime financial crisis, this is the new normal.

Strange times indeed.

When the fear factor ends, people will face lower rates. So, in theory they should pour part of their cash in equties.

Great post by Scott Grannis.

Perhaps inflation is a worry, but I sure would like to see Full Tilt Boogie Boom Times in Fat City for a few years after this horrible government-mandated shutdown nightmare.

There have been highly intelligent luminaries of the economics profession predicting higher rates of inflation for the last 40 years. Instead we have seen the US economy brought to the edge of deflation.

Let's get the unemployment rate down to 2%, then worry about inflation.

I'm 100% with Benj on his comments.

Something has been going on in this economy going all the way back to the 1990s.

Seems to me there was a major shift in the economy back then, and I wonder if our transition to a service economy had something to do with it. But that should not change monetary variables. I thought I had a supply-side understanding of the economy but now I'm not so sure.

My dream is to see robust economic growth with increasing productivity, growing wealth, very low unemployment, low inflation and increasing efficient manufacturing in the US, a strong Dollar, and abundant energy resources.

If Scott will allow, WHAT READER CAN RECOMMEND A TOP-LINE KITCHEN APPLIANCE MFG. AND WASHER/DRYER to replace LG?

Seems all our household appliances are lemons.

Scott - thanks very much for this post. I've been watching the M2 growth which, compared to 2008-09 is much different. My view was that in the financial crisis, the bulk of the FED money went to support banks. This time it has gone into the economy. I'd been worried about inflation but you've given me some other ways to view it. Thanks again - your comments are always enlightening.

Benjamin: For the umpteenth time I agree with you.

Inflation just isn't the worry, or shouldn't be.

Imagine if the Fed came out and said they were targeting 10-year breakevens at 2%. They will print until they get there. They have that power.

But, and this is a big but... I think it would be madness bordering on the immoral to keep pumping up various bonds in order to get money into the system. We've tried every version of that and we still have sub-2% inflation on every scale. Why don't we try sending money to every single social security number? $1000 every six months until breakevens are at 2%. No means testing, no exceptions for minors, no restrictions, no funny business. Tell the peeps this isn't due to economic weakness or anything else but a monetary fix for the unrelenting disinflationary pressures brought to us, mostly, by the incredible nature of technology.

Oh, and this would help at the margin to ameliorate the vast chasm between the haves and the have-nots.

Grechster and WealthMon:

I am dubious about the "QE only" approach, and I agree with Grechster that there must be a "helicopter drop on Main Street" role.

But I am a pro-business and work type of guy. So I favor tax cuts, my favorite being a holiday on Social Security payroll taxes, offset by the Fed buying bonds and placing them into the SS trust fund. This tax-holiday puts money into the hands of workers and employers---that is, increases the rewards for working and employing.

Aside from elderly and bona fide disabled, I am not a fan of sending people money for doing nothing.

I am somewhat offended we tax people who work for a living anyway, especially those on modest wages. I prefer taxes on property, pollution, imports, fuel, and a national sales tax.

But I have said this for years. The tax code is made in DC, with the usual results for the usual beneficiaries.

It would be entertaining to see FED taper of TQE while Treasury issues loads of new debt, but it wont happen. Rates would soar. So simply not possible. If this scenario plays out inflation will be let loose

Benjamin: We're all for payroll tax cuts. But for reasons that aren't quite clear to me there is no appetite for them in DC. And I too am not comfortable with sending people money for doing nothing. We shouldn't be.

But the conversation started with the observation that inflation refuses to go up to the Fed-preferred level of 2% after all the incredible interventions over the last 12 years. Animal spirits as expressed in velocity figures over 12 years have done nothing but decline.

For good or for bad we've all had to accept QE. The question then is how do we deliver it? We're right to be uncomfortable giving people money for doing nothing. But I'm even MORE uncomfortable bailing out the well-heeled after they made poor investments. Think of it. The Fed told the market that it will buy HY debt! Now really... They didn't just stabilize the Treasury market (off of which every other debt instrument is priced). They backstopped everything to include many investments THAT SHOULD HAVE BEEN WIPED OUT OR AT LEAST HAIRCUTTED. The interventions have been so dramatic and so long-lived that, imo, it is undermining the cornerstone of capitalism - price discovery on essential indicators.

When we speak of zombie companies we're really talking about the massive misallocation of capital; denying capitalism the heavy enforcement hand of failure. This concept is what brought down the Soviet Union.

Again, sending cash to every social security number is far from my first choice. But it is better than what we're doing. And it would force inflation higher. It would also, at least on the margin, give more power to the public to determine "winners and losers" in the corporate realm rather than leaving it increasingly to our dysfunctional government.

Thought experiment: Instead of all that the government has done over the last couple months, consider an alternative hypothetical. The Fed makes it known that it will backstop the Treasury market and maybe some critical dollar shortages overseas. But then instead of everything else, it just sent $10,000 to every SS number. That would cost $3.3 trillion, a figure that's very much in the ballpark of what was actually spent. At least this scenario would be more egalitarian and I dare say more effective for long term economic health. Businesses would have to compete more than they have to now for the consumers' dollars. And the ugliness of DC's preference for wealthy financial types would take a, uh, haircut. Instead, we bailed out HY bond investors, among many other investor types, while Main Street begs Washington for rent money.

There is probably a more current article, but this cold classic is worth the time:

https://scottgrannis.blogspot.com/2014/08/what-happened-to-all-profits.html?m=1

Grechster---

Yes, your idea is better than current policy, which as you say moves dangerously close to government support for weakling industries.

The situation today is very conflicted, as it was the government that mandated shutdowns, thus harming industries and their investors. Thus, any investor can justifiably say that, sure, they purchased a leveraged asset but it was reasonably leveraged until the government came along.

Well, let us hope for the best....

State of Georgia was first to open back up, and began with the "riskiest" close contact businesses first: haircuts, tattoos, and bowling alleys.

Everything is open there for the past few weeks.

Georgia just reported the lowest number of hospitalizations for COVID since they began keeping records.

Over half their deaths occurred in nursing homes. Almost all deaths had co-morbidities.

Nothing about this virus was as bad as the bureaucrats told us.

If I was able to publish an op-ed, the title would be "The global bureaucracy hits back". Thanks to covid scapegoat strateg they can control more resources. So one of the president Trump reforms were pulled back partially.

Great lecture by Adam Andrzejewski "The Depth of the Swamp".

Post covid, the Swamp only gets deeper.

“...there’s little correlation between the severity of a nation’s restrictions and whether it managed to curb excess fatalities — a measure that looks at the overall number of deaths compared with normal trends.”

“ In Europe, roughly three groups of countries emerge in terms of fatalities. One group, including the U.K., the Netherlands and Spain, experienced extremely high excess mortality. Another, encompassing Sweden and Switzerland, suffered many more deaths than usual, but significantly less than the first group. Finally, there were countries where deaths remained within a normal range such as Greece and Germany.

Yet the data show that the relative strictness of a country’s containment measures had little bearing on its membership in any of the three groups above. While Germany had milder restrictions than Italy, it has been much more successful in containing the virus.

The overall impression is that while restrictions on movement were seen as a necessary tool to halt the spread of the virus, when and how they were wielded was more important than their severity. Early preparation, and plentiful health-care resources, were enough for several countries to avoid draconian lockdowns. Germany, with better testing and contact tracing and more intensive care units than its neighbors, could afford to keep the economy a bit more open. Greece, by acting quickly and surely, appears to have avoided the worst, so far.

As one would expect, the countries with the most intense lockdowns look likely to suffer the most economically. What’s not clear yet is how much economic benefit countries with relatively lax curbs really stand to gain, given the integrated and trade-driven nature of the European economy.”

https://www.bloomberg.com/graphics/2020-opinion-coronavirus-europe-lockdown-excess-deaths-recession/?srnd=premium-europe

In the United States the early evidence out of Washington State was that the ~10% of general population older than 65 had a higher prior likelihood of adverse outcome from COVID 19 than the ~90% of the population under the age of 65. However, little or nothing was done to isolate older people confined in rest homes (eg NY, MA). The federal health bureaucracy and elected officials were merely part of a political response that, like state governors, focused primarily on the November elections.

“In the end, it does not come down to country- or even city-level statistics. It comes down to people. Each individual catches the bug or not, lives or dies. Not because of their country, but because of themselves, their health, their circumstances. Any given individual might have benefited from self-quarantine and loss of job. Just as any given individual might have come to a bad end from a lockdown. The only possible way to know is to measure each case. Which can never happen.

What should we conclude? Strike that. What can we conclude. Only one thing: we cannot conclude that lockdowns worked.”

https://wmbriggs.com/post/30833/

“It is reported that Boris Johnson recently joked with his colleagues, saying: ‘I’ve learnt that it is much easier to take people’s freedoms away than give them back.’ “

https://www.spiked-online.com/2020/05/20/the-lockdown-has-done-untold-damage-to-this-country/

“Results Twelve studies were identified with usable data to enter into calculations. Seroprevalence estimates ranged from 0.113% to 25.9% and adjusted seroprevalence estimates ranged from 0.309% to 33%. Infection fatality rates ranged from 0.03% to 0.50% and corrected values ranged from 0.02% to 0.40%.

Conclusions The infection fatality rate of COVID-19 can vary substantially across different locations and this may reflect differences in population age structure and case-mix of infected and deceased patients as well as multiple other factors. Estimates of infection fatality rates inferred from seroprevalence studies tend to be much lower than original speculations made in the early days of the pandemic.“

https://www.medrxiv.org/content/10.1101/2020.05.13.20101253v1.full.pdf

The federal and state governments’ response to COVID 19 is among the most damaging policy in American history.

It began with the intention of “flattening the curve” of patients in need of ventilators arriving at ICUs. The economy was locked down and ventilator production was sharply accelerated. By the time the first ventilators had arrived, it was discovered that COVID patients are poorly served by being intubated and that ventilation is better avoided than used. Meanwhile, the COVID financial plan had run 3T in deficit, unemployment had risen into the teens, securities markets shed 30% of their year end values and the hospital system had been crippled by underutilization.

What should have been obvious from the beginning was that the segment of the population in rest homes was far more at risk than the general population. For the last several weeks state governors and the federal bureaucracy have done little more than engage in a blame avoiding, “cover-your-ass” exercise and focused on nothing as much as the November election.

The sooner the lockdown and it’s fabricated restrictions are tossed onto the scrap heap the better.

The link below describe a policy failure that might better be called “Thomas Bayes’ Revenge.”

https://www.aier.org/article/focus-on-the-covid-19-death-rate/

cbt696 -

Thanks for the link. My comment is that the intended article was informative, but even more, I could not help being drawn into the following article deconstructing Franklin Foer's "vegetarians save the world" opinion piece. A good example of how ideologues repeatedly screw up by reducing complex systems with simplistic and misleading but smart sounding "science".

Oops, got my Foer's mixed up. Jonathan Safran Foer is the vegetarian activist. Franklin Foer is the former New Yorker editor.

Will we see inflation?

The Cleveland Fed inflation expectations model says inflation under 1% for next six years.....

https://www.clevelandfed.org/en/our-research/indicators-and-data/inflation-expectations.aspx

Of course, in present circumstance, any model or outlook is probably a bit suspect Who knows? Inflation might even be lower. But as of now, a serious attempt at modeling, by the inflation-phobic Federal Reserve, says no inflation for the next six years.....

Wake up, America!

Outside of the Boston-Philadelphia corridor, Detroit, Chicago and NOLA, the COVID 19 never merited any consideration for any extreme public health intervention (graphic at link)

The lockdown was the result of a media feeding frenzy that empowered the entrenched bureaucracy to expand its writ by panicking an inept political class that focuses on nothing as intensely as getting itself elected.

The true death toll from the lock down will trickle in over the next several years from suicide, undiagnosed cancers, postponed surgeries, mis-spent charitable resources, etc and et al.

“The urge to save humanity is almost always only a false-face for the urge to rule it. Power is what all messiahs really seek: not the chance to serve.”

H. L. Mencken

“No democratic delusion is more fatuous than that all men are capable of reason, and hence susceptible to conversion by evidence.“

H. L. Mencken

"The whole aim of practical politics is to keep the populace alarmed (and hence clamorous to be led to safety) by menacing it with an endless series of hobgoblins, all of them imaginary."

H. L. Mencken

Link to graphic referenced above:

The map above of COVID deaths by US county shows a much higher level of granularity than my recent map of deaths by state and illustrates graphically the disproportionate concentration of COVID deaths in selected counties in New York, New Jersey, Massachusetts, Connecticut, Pennsylvania, Illinois (Chicago area) and Michigan (Detroit area). Interestingly, two-thirds of COVID deaths in the US have occurred in counties that represent only 15% of the US population.

https://www.aei.org/carpe-diem/map-of-the-day-us-population-divided-by-one-thirds-of-covid-deaths/

The big Keynesian theory in practice. Fill in the gaps and then cut back. I wonder if the cut back will actually occur.

Europe Admits Shutdowns Were a Mistake

· Norway Health Authority Admits Lockdown was a Mistake: "Our assessment now....is that we could possibly have achieved the same effects and avoided some of the unfortunate impacts by not locking down, but by instead keeping open but with infection control measures," Camille Stoltenberg, head of the Norwegian Institute of Public Health, said. "The scientific backing was not good enough," Stoltenberg said of the decision to close down schools.

https://www.thelocal.no/20200522/norway-could-have-controlled-infection-without-lockdown-health-chief

· Spain Cuts its COVID Death Count by 7,000: "The Spanish Health Ministry on Monday revised downward the official coronavirus death toll in Spain. The total number of victims since the beginning of the pandemic stood on Sunday at 28,752. But on Monday, the figure reported was 26,834. This represents a drop of 1,918, or 7% of the total."

https://english.elpais.com/society/2020-05-26/spanish-health-ministry-lowers-coronavirus-death-toll-by-nearly-2000.html

.......

Non-Stay At Home States Lost Fewer Jobs

Our friend Dave Trabert at the Kansas Policy Institute examined the state by state April jobs report. His findings confirm common sense, but we have lost that during the pandemic crisis.

• The 8 not shut down had a 9.8% decline over March levels, while the other 42 states fell 15.4%.

• Six states had losses less than 10%, and they were all states not shut down by their governors.

Graphic:

https://sentinelksmo.org/april-jobs-private-sector-down-10-5-state-govt-steady/

Would be interesting to see some graphs specific to deficits and future tax implications of this inane shutdown. The 5000 $ Social Security loan for delayed benefits I see floating around wreaks of future budget issues.

Hello Scott, I can't believe you just wrote about this because I have been mulling for years your position that the Fed is not printing money. Well, if the Federal Reserve is buying Government bonds with money "created out of thin air" (through the vehicle of Bank Reserves), what really is the difference? The government is then "air dropping" that money through various programs, very similarly to the anecdote about printed money being airdropped.

Yes, the government bonds are an iou, but everyone knows they cannot be paid back without the Fed there to buy more bonds. The Fed will have to keep buying bonds to keep interest rates from going too high, but this will cause more inflation. Is this not in effect the same as printing money? As to why it did not happen (inflation) during the last go around, well, it did: because of the huge technological productivity of the last years, we would have had falling prices (the offshoot of higher productivity that people have all but forgotten about). This was offset by the Fed's releveraging of money supply. Does this make sense, or am I off base? Richard

Post a Comment