Recently we had 32 family members for our traditional Christmas Eve dinner. About two-thirds of us (my wife and I included) ended up testing positive for Covid, and I'm pretty sure we all got the Omicron variant.

Everyone thought they were healthy to begin with, and the index case was the only one of the group that was triple-vaxxed—surprises all around. Only 3 people were unvaxxed, and all 3 got it; 22 fully vaxxed individuals got Omicron, and virtually all of them had received two doses of the Moderna vaccine. Three people had had Covid previously, but none of them caught Omicron. No one has even considered going to the hospital.

Nobody thought they were sick that evening, so we were all surprised by the ease with which the virus spread; it is indeed extremely contagious. The virus mainly attacks the muscles, the throat, and the sinuses. Very few of us developed a fever; I never did. I've had worse flues, but mainly because most of my flues were accompanied by fever and ended up with many days of coughing. I'm now six days into the infection, and my only compliant is a sore throat. I did feel very tired the first 2-3 days; muscle soreness was notable, even almost debilitating—but it quickly passed. Only a sore throat has lingered.

It was not easy to find a test kit, at least in our neighborhood. Yesterday the city offered free testing at a nearby school, and there was a line of people three blocks long waiting to be tested.

My takeaway: the MRNA vaccines don't protect you at all against Omicron. Omicron is similar to a flu. Above all, it is extremely contagious, so I won't be surprised if nearly everyone ends up getting it. A few weeks ago, I remember telling people that I wouldn't mind catching Omicron, if only because that would solidify my immunity to this crazy virus (I was fully vaxxed last February). Now that it's happened, I have no regrets. Sayonara, Covid!

We already know from the numbers that new Covid cases are skyrocketing, and I fully expect that to continue. I imagine that a significant fraction of the population will end up catching Omicron. With many millions at home sick for a week or so in coming weeks, that is bound to negatively impact the economy, but not permanently. It looks like the market agrees, since it reached a new high today. But I wouldn't be surprised if the news of millions of new daily cases doesn't shake people's confidence a some point in the near future.

And now for a quick look at some charts:

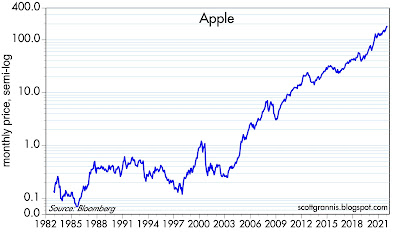

Chart #1

Chart #2

Apple is not a complete outlier, as Chart #2 shows: its market cap is not greatly different from Microsoft's. Both have enjoyed spectacular gains over the years, and they've been jockeying for first place for more than a decade. Both are riding a technological wave of tremendous progress, and both are selling products and services to a market that now includes many billions of customers. Never before has any company enjoyed such a huge market. The other thing I like about this chart is the way it shows how Apple, once a David to Microsoft's Goliath, triumphed in the end.

P.S. I've been working on an update to my money supply/inflation thesis for the past few weeks, and hope to publish it soon.

20 comments:

Very sorry to hear of your illness and am glad you feel that it is going so well.

I am trying to backtrack the date of infection to the date of posting. Am I correct that you were exposed to the index case on the 24th, and first developed symptoms about five days after exposure on Wednesday December 29th please?

Best wishes to you and yours for a Happy and Healthy New Year.

Pretty sure I was exposed on the 24th, but it could possibly have been on the evening of the 23rd. I now think my first symptoms appeared on the 28th. I felt pretty lousy the 29th, 30th, and 31st, but since then I have been gradually improving. Today I have only a moderately sore throat. My wife has fared better than I have all along. All in all, not so bad considering we are both 72. Though I'm sure it helps that we have a fairly active, outdoor lifestyle along with regular weight training sessions.

Good luck to Scott Grannis, and of course everybody, with Omicron. IMHO, we will all get it, wherever you are on the planet and whatever precautions you take.

Fighting C19 is like fighting the tide with bucket and sand.

Well, from Reuters---

"S&P 500, Dow hit record highs on 1st trading day of 2022"

---30---

They say Wall Street is forward-looking. Let us hope Wall Street is right.

Full and quick recovery to you. Best wishes in 2022.

Glad to hear you're well and thanks for the story. I like to hear personal and non biased experiences with that virus/s. I'm looking forward to your inflation thesis.

Generally the money supply has been controlled via Open Market Operations, fractional reserve system, FFR, Discount Rate, more recently IOR. Now SOFR too?

FED/Treasury seemed to have bypassed this system and injected significant currency in circulation directly to citizens bank accounts, business, and small businesses. Federal unemployment subsidy, child tax credits, stimulus checks, Payment Protection Program, etc.

I was dismissed here before for mentioning this but I still can't see how it didn't have some significant effect on the money supply and inflation. (Or maybe it was a technicality where I believe we increased the money supply outside of the fractional reserve banking system and both you and Carl said I was wrong).

It's like the Fed/Treasury is performing Monetary and Fiscal Policy at the same time...

Income/aggregate demand shot up/right, even as unemployment surged.

Aggregate Supply shocked left.

Prices/inflation scissored up.

Do we still talk about cost push demand pull inflation anymore? These things happened. And the money supply shot up seemingly independent of monetary policy and fractional reserve.

Ataraxia--

I think you ask interesting questions.

With the advent of sustained QE (Bank of Japan, the Fed) we are seeing, some say, modern monetary theory (MMT) in action.

The US government spends money, the Fed prints money and buys US Treasuries...it really is a money-financed fiscal program.

If the Fed is regarded as part of the US government (I think it is), then the US government indebtedness has not risen in the last couple of years.

Some will talk about reserves at banks, and that is something of a clunky leftover from the Federal Reserve and commercial banking origins. Will the reserves eventually lead to too much lending? Supposedly, that is the theory behind the need for interest on excess reserves.

Frankly, I think the Fed should print money and buy the US government bonds directly, and bypass the claptrap of buying bonds from broker-dealers who then place the bonds into their accounts in the commercial banking system. Rube Goldberg, where are you?

Well, new records ahead on the S&P 500, and inflation is cooling off in some places. Maybe things are not so bad.

Happy new year Scott!

Been reading you for many years (2007 or 2008 I believe), your knowledge and judgement are unmatched as far as I'm concerned, thank you!

Jean-Pierre

Thanks Benjamin-

I've watched a few great recent interviews of old timer FED Reserve insiders, Plosser, Hunt. The FED culture was historically staunchly independent and pretty much laser focus on inflation/price stability. The unemployment mandate which is well known to be usually in tradeoff to inflation/price stability was added even though not everyone agreed that should be the case.

The FED now actively influences relative financial market price signals which was historically correctly frowned upon and denied. Mortgage backed securities, corporate bond purchases, etc. I think the FED has innovated into confusion. Some time ago, even BV (Before Virus), Powel state Fiscal Policy was needed due to zero lower bound.

They, Fed/Treasury/Government are amalgamating all these things which obfuscates price signals needed for sound decision making.

-On the coronavirus

Catching covid a few days ago is different from carching covid a while back, for somebody who is 72. Covid (omicron) is now a less virulent form and vaccines still do an amazing job at decreasing covid risk of severe disease, hospitalization and mortality. That’s what ‘they’ meant (at least in a way) when the concept of curve flattening was described.

The omicron spread is a blessing in disguise as it will help to transition to post pre-covid status but there will be short term pain to be ‘felt’ in the next few weeks. Even if more benign, the omicron spread is truly phenomenal and will cause a significant rise in hospitalisations during a time when healthcare human resources will be squeezed also maximally as a result of covid+ workers’ absenteeism. Clearly not an extinction-level event but US hospitals will tend to ‘feel’ like Canadian-socialized-medicine hospitals for a while. I wonder if Americans will get used to that?

-On the inflation

The Covid episode showed that the coordination of money and fiscal policy could result in inflation (not in Japan though even at this point). And of course, the path to runaway inflation is a potential avenue. The key question though is to wonder if inflation will persist and for how long. I just looked at a graph correlating interest rates and inflation over the last 30 years and we’re clearly in a unique and uncharted territory with this Fed-Treasury experiment. The two will have to reconcile somehow. My bet is that the fixed income market (at least the part that’s not manipulated) is more right than wrong and it may be reasonable to expect disappointing growth and disappointing inflation going forward.

Timing is always tricky but all loans and leases (held in all US commercial banks) will be back to its longer term trend within the next 2 to 4 months and the new normal post pre-covid will be stuck with much more debt in the aggregate. Still, the huge elephant in the room appears to be the amazing growth of government debt securities held by commercial banks since the GFC and, especially, since March 2020, a unseen issue responsible for a very significant growth in money supply through synthetic direct commercial banks’ loans to the government.

Japan just announced an incredible stimulus package (as % of previously announced public debt issue, per unit of GDP etc) based on (IMHO) Ponzi finance only possible because of still existing unique conditions, including a transfer of ¥100,000 to all resident minors (18 years old or younger).

Unless the US becomes a Banana Republic, i think persistent inflation will never come, just like Godot. Of course, one should never say never.

Scott, glad you're recovering rapidly....been missing your commentary. ten year yields reached a critical area today, if you're a technical guy [i am]. a break above this level gives me a target of 2.15%, which is not enough to derail the equity train.

keep posting your thoughts, and again, get well quickly.

Scott Grannis" "22 fully vaxxed individuals got Omicron...No one has even considered going to the hospital."

Also Scott Grannis: "My takeaway: the MRNA vaccines don't protect you at all against Omicron"

:Facepalm:

You might want to figure out how these vaccines are meant to work.

Your unvaxxed friends/family members should consider themselves very lucky. I'm currently dealing with an anti-vaxx friend in the ICU (45 yrs old, fit, no underlying conditions, 3 young children). Positive on the 24th, covid pneumonia, weeks of hospital time and months of recovery ahead of him (if he survives). All completely avoidable of course. Granted I don't know if it is Omicron or Delta (Delta is still raging).

Anyways the vaccines don't stop you from contracting, but are pretty darn effective at keeping you out of the hospital and alive.

Our Orange County Deputy DA (and anti-vaxxer) found this out the hard way today as well.

Welcome to club Scott!

All the best for a great year ahead.

Appreciate your work -- thank you.

Scott tends to read the book upside down...vaccines are not meant to prevent you from catching the virus, for crying out loud, some vaccines even inject a tame form of the virus into a person so the body trains to fight it. Vaccines help you survived the virus, so that you kick back at home watching tv while your body fights the disease, instead of being in the ICU, breathing thru a tube. Hark back to the middle ages when the Black Death stroke Europe. I bet they wish they had vaccines. By the way, the same bs ya'll see now with people about the pandemic, pretty much the same bs that played back then.

There are already 2 readers who essentially posted what I would regarding the vaccines. I’m a financial advisor, so I have no official qualifications, but I happen to have a Dr. as a client who has over thirty years of epidemiological experience on two continents.

He hasn’t entered the inflation debate, due to his humility.

The bubonic plague traveled on the Silk Road from China.

Sorry to hear you got sick, Scott. Glad to hear you're getting better.

Scott, I just learned you have been sick. I hope you fully recover very soon. You are terrific in my book.

10 yr still trying to make something stick.

The below is from your blog:

Inflation: headline inflation has gone down, but core inflation hasn't; once oil prices bottom (which I think is happening), all measures of inflation will head higher; I don't see a hyperinflation yet, but I do see inflation that is significantly higher than what is priced into the bond market. The main driver of higher inflation will be the Fed's inability to withdraw its massive liquidity injections in a timely fashion; they will prefer to err on the side of inflation rather than risk a weaker economy.

It was your predictions December 31 2009...your first post.

Any thoughts please?

I just read Mish Talk's comments on bonds. The govt has 25% of the TIPS market, not sure of average maturity.

"TIPS are no longer a market signal about inflation expectations, the Fed ruined this with its big footprint. TIPS are flow driven and flows are dominated by expectations of the speed of the Fed printer."

The FED really ramped the purchases since the pandemic started. So does the bond market really see 2.8% inflation over the next 5 years? Seems like this number could be more volatile and less reliable than in the past. Would the conclusion of a market expectation of low growth be any different if this number was 5%? Or would that just bolster the conclusion from chart 5?

BTW, thank you for putting out this blog. As an engineer I get great value out of the charts and they have really increased my understanding of the markets these last 5-10 yrs.

Jeff F: Thanks for your comments, nice to know the charts are appreciated, as I do take pains in that regard. As for the Fed distorting the TIPS market through its purchases, I've addressed this issue in prior posts over the years, and I have addressed the subject professionally with clients for decades. The short answer is that the evidence to support the thesis that QE has distorted the Treasury market is weak. The Fed today owns about 25% of all marketable Treasury securities. The Fed about 20% of the market about 20 years ago, and it's holdings have since that time ranged from a low of 7% in early 2009 to a high of 25% (today). Over that same period, 10-yr yields have ranged from a high of 5% (2006) to a low of 0.6% (2020). There is no obvious correlation that I can see; in fact there are periods during which the Fed was selling bonds by the truckload yet yields were falling. In the past year, Fed ownership of Treasuries has risen from from 20% to 25%, while yields have fallen from 0.5% to now 1.8%. Over the decades I have failed to uncover any convincing evidence that Fed bond purchases distort interest rates.

The Fed indeed owns a lot of Treasuries ($5.6 trillion), but that represents only a fraction (<10%) of liquid, marketable global debt. And since the Treasury yield curve is the risk-free standard against which all other debt is measured, it strains credulity that the Fed has distorted the entire global bond market. Indeed, I have never found evidence of inter-market distortions. Credit spreads, for that matter, are near historical lows; if Treasury yields were artificially depressed, we would expect to see the spread between Treasuries and other, more riskier debt at relative highs.

In short, Mish is treading on thin ice. But it is true that yields of all sorts are driven in part by expectations of what the Fed is going to do in the future. As many have observed, the Fed often times follows the lead of the bond market and vice versa.

Post a Comment