Chart #1

What Chart #1 shows is that consumer comfort is higher now than at any time in the past 34 years. The Bloomberg Consumer Comfort index started to soar just days after the November '16 elections. It appears quite likely that Trump's policies were the proximate cause of much, if not all, of this dramatic improvement in sentiment.

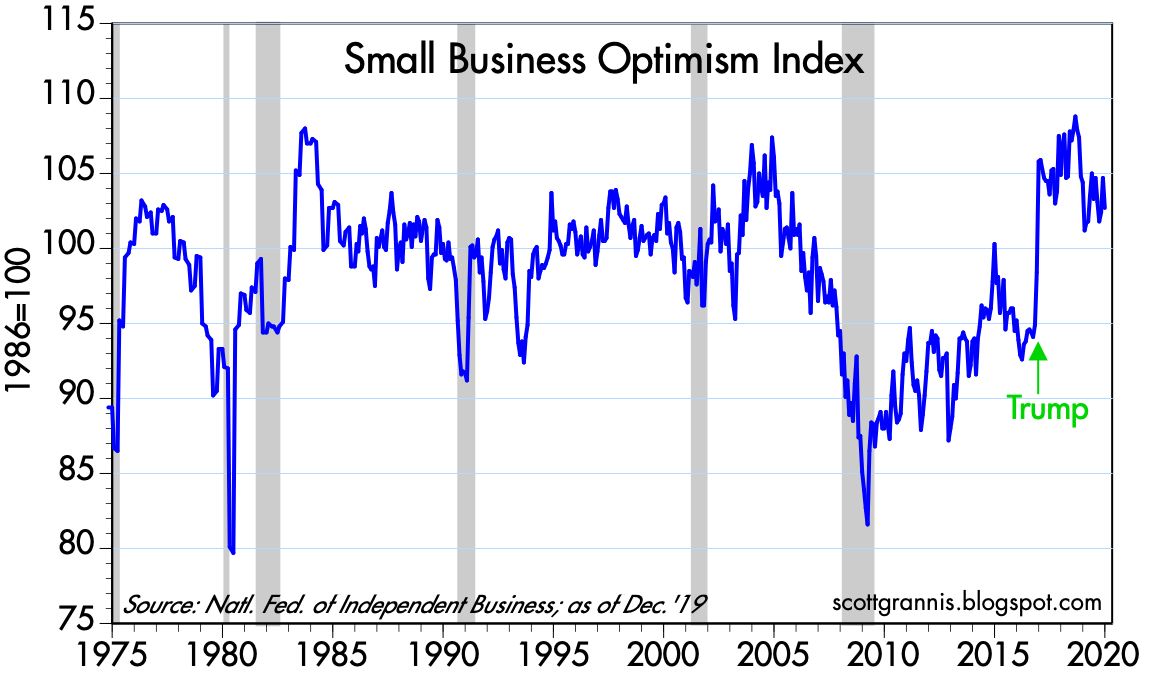

Chart #2

As Chart #2 shows, Small Business Optimism also began to soar just after the November '16 elections.

7 comments:

If height matters, he'll never catch up to Trump.

How do those charts jibe with the reduced business investment from trade related uncertainties? Is it the tax cut? Long time reader, first time commenting. Thank you Rick

I do not know why Bloomberg wants to be president. Trump had reasons to be president, those being lower taxes on business, control of illegal immigration (which harms America's employee class) and getting out of the Middle East.

I am disenchanted with Trump's inability to withdraw the United States from fantastically expensive yet counterproductive Middle East entanglements.

If Bloomberg would commit to a pro-business platform, and a radical reduction of US involvement in the Middle East, I might ponder voting for him.

I've been a Trump critic for the duration. I've argued that any actions / "decisions" that worked out for him are pure coincidence or luck, lacking any evidence of understanding or strategy. But my God, the man's survival and opportunistic instincts are stunning. He has without a doubt come out of impeachment stronger and has the opposition running in horror to an 80 year old socialist - like that will work out. It's starting to seem the smart people overthink politics and strategy. And underestimate the appeal to those being led, for a leader with big balls. Particularly these days when emasculation carries the left. Stunning.

Re "How do those charts jibe with the reduced business investment from trade related uncertainties?"

That's an excellent question, because one would think that with the huge increase in consumer sentiment and small business optimism there would be a similar increase in business investment. Moreover, since corporate profits have been exceptionally strong relative to GDP for most of the past decade, one would expect to see a big increase in business investment. But that's not been the case, at least to judge by things like capital goods orders and gross private investment, all of which suggest that business investment has been lackluster. In turn, lackluster business investment probably accounts for the fact that labor productivity has been modest.

I've suggested in previous posts that one reason this has been happening is the substantial increase in federal transfer payments that began in 2009. The more the government hands out to those who don't work, the less incentive they have to work, invest, or take risk. Another reason could be the federal budget deficit, which has effectively absorbed a sizeable fraction of corporate profits. Yet another reason could be the persistence of risk aversion, about which I've commented numerous times over the years. There are lots of signs of optimism, but this doesn't necessarily mean that risk aversion can't exist as well. The demand for money remains very strong and has been increasing for most of the past decade.

I might add that for many years most of the world's major economies have been devoting a substantial amount of investment to "green" projects (e.g., windmills, solar power). Those projects have been justified in the name of saving the planet from eventual climate destruction, but in the meantime they have been terribly unproductive. Fossil fuels remain by far the cheapest source of energy. Using anything else is equivalent to throwing money down the drain, unless you consider it to be an investment in saving the planet, and that, unfortunately, is very hard to prove.

In short, it appears that numerous factors have contributed to dampen the economy's "animal spirits."

But that's not been the case, at least to judge by things like capital goods orders and gross private investment, all of which suggest that business investment has been lackluster.---SG

If a US-based company invests in plant and equipment offshore, is that counted as gross private investment in the domestic count, or not?

As Scott Grannis has pointed out, these are the good old days for corporate profits, higher both absolutely and relatively than ever before. We are also seeing record volumes of corporate stock buybacks.

This suggests that everything is already invested in full, that is we have capital gluts. I often ask on blogs, "Is there an industry anywhere straining to meet demand?," and I have never found a positive answer.

The world could absorb a lot more aggregate demand. I think the answer is money-financed fiscal programs, as non-PC as that policy might be in some circles. I suggest tax cuts on wages to stimulate demand, But no increases in spending on social welfare or warfare....

NormanB: re the equity risk premium. Today’s premium is relatively high, just as it was in the late 70s and early 80s. Back then would have been a fantastic time to turn bullish on equities, because the high premium reflects a lot of bearish sentiment that late proved mistaken.

Post a Comment