A Fed rate cut along the lines the market is calling for will not strengthen the economy. Easier money can never generate growth all by itself, but easier monetary conditions can make it easier for the market to cope with adverse conditions. Smooth-running financial markets are an essential ingredient to the health of the economy. Right now, financial market conditions are an impediment to growth, and the Fed can and should remove that impediment by acting soon.

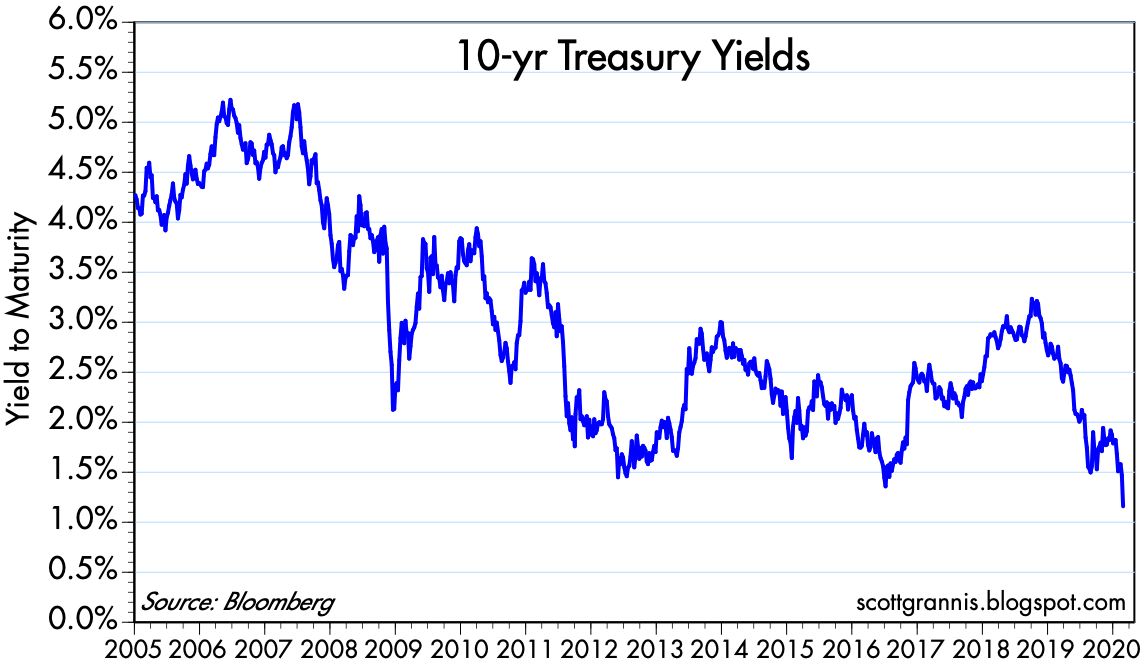

Chart #1

As Chart #1 shows, 10-yr Treasury yields have fallen to new, all-time lows—currently 1.17%. 5-yr Treasury yields are now just under 1%, a level last seen/exceeded only during the panic surrounding the PIIGS and Brexit crises (2011-2013).

Chart #2

Chart #2 is the best way to judge whether the Fed is keeping short-term rates too high. The red line (5-yr TIPS yields, which are the market's expectation for what the real Fed funds rate (the blue line) will average over the next 5 years, has recently fallen below the current real Fed funds rate by about 50 bps (the 5-yr TIPS yield is -0.44%, and that is about 50 bps below the difference between the current Fed funds target, 1.75%, and the current Core PCE inflation rate, which is about 1.7%). In short, the market now thinks the Fed is "too tight." The pricing of Fed funds futures shows that market fully expects the Fed to cut rates by 50 bps within the next few months. Given the panic, the sooner this happens the better.

Chart #3

Chart #3 shows the prices of gold and 5-yr TIPS (using the inverse of their real yield as a proxy for their price). Both have surged of late, reflecting the market's strong desire for safe and safe-haven assets.

The Fed can't provide a cure for the Covid-19 virus, but it can mitigate its adverse effects by easing monetary conditions in response to the market's increased desire for money and money equivalents. Doing so is simply doing the Fed's principal job, which is to maintain a balance between the supply of money and the demand for it. Right now the Fed is not doing enough, and we can see that in the fact that inflation expectations have fallen by roughly 25 bps in the past 10 days, to a relatively low 1.4%, as shown in Chart #4.

Chart #4

P.S. Be sure to check the updates to my last post for insights into the degree to which the market has panicked.

UPDATE: as of March 4. Yesterday the Fed did indeed cut rates by 50 bps, but there is still some pressure from the market for at least one more cut and likely two. In light of the majority of comments I see in the press to the effect that the Fed pulled a "shock and awe" move, and that it might be running out of ammunition, I feel the need to reiterate that the Fed's move has nothing to do with "stimulating" the economy or an otherwise positive "shock" to sentiment. It's simply a recognition of market realities.

The current real (inflation-adjusted) Fed funds rate is about -0.45%. But the current real yield on 5-yr TIPS (which is essentially the market's forecast for what it thinks that rate will average over the next 5 years) is -0.60%. Thus the market expects the Fed to cut at least once more and/or inflation to rise a bit from current levels.

It may also be the case that the very low level of interest rates on short-term securities like TIPS and T-bills is the market's way of telling the Fed that there is a shortage of such securities. Perhaps the Fed should consider increasing the level of excess reserves. The press would shout "another round of quantitative easing!" but in reality it would just mean accommodating the market's desire for more T-bill equivalents (bank reserves are in effect T-bill equivalents). The Fed can expand reserves by buying notes and bonds and paying for them with reserves, just as it did in three QE episodes. When the demand for reserves is intense, as it is now, transmogrifying notes into T-bill substitutes is not inflationary, nor is it necessarily stimulative. It's just supplying more short-term securities to the market to satisfy the demand for such. That would presumably allow the financial markets to function more smoothly, and that, in turn, could make it easier for the economy to deal with the uncertainties of the Corona virus

UPDATE: as of market close March 5th: The Fed is almost certain to cut rates by at least another 50 bps. Chart #5 provides the rationale:

Chart #5

I've long argued that the Fed usually follows the market. Chart #5 shows partial proof. The orange line is the 3-mo. T-bill rate, and the white line is the upper bound of the Fed's funds rate target. Note that in the early stages of Fed tightening (2015-2017), the Fed tended to lead the market: T-bill rates moved up several months after the Fed raised its target. But since 2019 the Fed has been following market rates on the way down. T-bill rates were always ahead of the Fed, and each ease was merely an attempt to bring the funds rate in line with T-bills. Since Tuesday's cut of 50 bps, T-bill rates have plunged. This suggests the Fed will need to cut rates by at least 75 bps just to keep up with the market!

When the Fed cuts rates in order to follow the market down, this is NOT monetary ease. It's NOT stimulus. It's NOT money printing. It's passive monetary policy. The big story is NOT Fed easing. The big story is the market's insatiable demand for safe and liquid securities. The virus-induced panic has caused a tremendous increase in the demand for money and money-equivalents, which are now demonstrably in short supply. The Fed MUST accommodate this demand by lowering its target rate and by increasing the supply of bank reserves (i.e., QE4).

43 comments:

No surprise that 10-year TIPS spreads have imploded, as well. According to this key metric we're waaaaay below the Fed's 2%.

It’s funny how spooked markets get. This is a healthy correction. We haven’t had a major pull back since last year and before that it was a while.

Just a blip over the long haul.

Sure seems like the Fed should cut interest rates and maybe Step Up on quantitative easing as well. However, both of these stimulative measures are somewhat clunky and slow.

There should be a mechanism whereby the Federal Reserve can engage in money financed fiscal policy, that is, an immediate tax cut financed by the Federal Reserve's printing of money.

The media and various governments appear intent on fomenting a panic in response to what is a serious cold virus, but nothing more than that.

Like everything else today, the coronavirus will become a platform for various hysterical ideological and political wars.

Thus, we could see real GDP decline at a 10% annual rate, as it did in the fourth quarter of 2008.

Helicopter drops would be the right antidote for such a contraction, but unfortunately they are not yet within the Federal Reserve's arsenal.

The sharp drop in markets tells me nothing very solid was propping it up. I think investors knew it was hyped and needed an excuse to get out. Interesting to read these comments calling for the Fed paramedics to rush to the scene and start another IV - in supposedly the greatest economy of all time.

Such good stuff as always. Just one typo: it’s “principal” not “principle” in this case.

Perhaps Joe Biden's win tonight in SC will calm the markets a bit. Any good news that puts a dent in crazy Bernie's march to the nomination should help.

Great post, Scott.

I have zero faith in Powell. He will screw up the timing of this inevitable rate cut, or botch the Q&A (on purpose??) to mitigate the effects as much as possible. Just like he’s done since he took office. Prove me wrong.

I agree with Fred about the Biden victory calming markets, somewhat.

Imagine if Trump announces a temporary ending of all tariffs thru year-end.

As a “goodwill gesture for the children of corona.”

CEOs would scramble to get orders done. Economic activity would surge, and this flu virus hype would return to back-burner status.

Donald...are you listening?

Scholar87: Thanks for the edit, now corrected!

I don't see where the Fed should do anything.

The economy is humming along nicely, as you have pointed out in post after recent post.

The markets were overvalued, and now they are freaking out and correcting. Good.

In short, it is not the Fed's job to save the markets from their own excesses. If the Fed cuts rates because the markets cannot keep their heads about them in the face of a minor health scare -- really, how many people out of 7.6 billion have died? -- then it might as well throw its charter away and acknowledge that it works for Wall Street.

Rick: the curve is inverted again. The Fed Funds rate is once again the highest interest rate of all.

The bond market is saying the Fed is too tight for conditions.

Rick: I know it seems bizarre (because the Fed Funds rate is historically low) but the Fed is starving the system of money. The most obvious evidence is the bond market as JBD points out. Not only is the curve inverted but breakevens have plummeted (and are far below 2%). We can see more evidence in the industrial metals markets, oil, nat gas, and the ag markets. PCE core is well below 2% as well.

I suspect we'll be engaging in another round of QE before too long. If it comes to that I hope the Fed will invoke a new wrinkle and give money straight to the people rather than buying Treasuries and/or MBS. $1000 to every social security number would be a good start. I'd also like to see a promise to issue another $1000 every six months as long as the PCE core is below 2% or, alternatively, breakevens are below 2%. If they did this it would clarify the policy. It would also have the effect of narrowing the gap between the haves and the have nots, if only by a little bit.

Remember Friedman: Deflation or disinflation is the easiest thing to fix. Just print money.

Just not true...

It's the speed of the down move. This was violent. Three of days biggest down ever in the last week.

Sunday nite, 8:45pm New York time....Futures just jumped 500 points from earlier.

From Wesbury (edited)

Active coronavirus cases (total minus deaths + recoveries) have dropped sharply, from a peak of 58,747 on February 17th to 44,314 Friday. They keep falling, worldwide. Today 43,293.

Active cases are the only ones that can spread the virus.

The press keeps reporting total cases, and deaths, but not the recoveries.

Odd. Almost as if they want it to be bad. 94% of total cases are from China. 96% of deaths are from China.

Scott, I love your earlier graphs showing 2 year and 10 year Treasury yields. Can you please update to current? Inversions seem to be a collapse of the term premium. Previously, when the term premium disappeared, it appears that a return to positive term spread came via a drop in short term yields. Is that a correction in fundamentals or due to Fed short term reductions due the recession? This time, there does not appear to be much room for the short term yields to drop to restore a term premium. Might this time be different? What happens if the term premium does not recover?

Record gain in points today. Dow up 5%. Panic unwinds, as predicted.

Unfortunately, volume on NYSE was down 32%.

Not at all what we want to see on a huge move up in all indexes. I’ll take it. Friday was an excellent purchase.

DEMs all rallied around Feeble Joe today to box out Bernie. Candidates were paid to drop out and endorse. Same as it ever was.

That was the real story of the afternoon.

Super Tuesday is huge for these nuts. Posturing and payoffs. And The People applaud, anyway. Not so “woke” after all.

If Bernie refuses to leave, there will be a split Party and Trump rolls. Or Bernie gets another beach house, and they “all come together”.

Isn’t it odd that the more senile Joe becomes, and the more he babbles incoherently, the higher he advances in the “polls”?? Odd, indeed.

Can you imagine this person getting a single delegate in the America of Yesteryear??

It’s time to congratulate Sleepy Joe for winning his very first delegate EVER in three Presidential campaigns.

Get ready for Ms Vice President Stacey Abrams, maybe with either candidate. Biden is just too in debt to the black voters not to offer to a black woman. If she is the choice, the election cycle will be race baiting olympics. Depressing to think that no matter WHAT the outcome - Biden, Bernie, Trump - we are in for another 5 years of daily trauma.

Stacy Abrams says she was elected Governor of Georgia, so at least she has experience.

BOOM

Unanimous decision by Fed

Bingo!

I'm pleased the Fed today followed my advice. However, I need to reiterate what I said in the first part of this post. Cutting rates by 50 bps does not stimulate the economy; it's not a growth turbo-charger; it won't, by itself, cause the economy to grow faster. The rate cut was a response to market conditions.

I'll also reiterate my oft-repeated view that monetary policy is like a dance, with the Fed being one partner and the market being the other. It takes two to tango. Both partners send signals to the other, and they need to follow one another. The Fed has gotten the market's message.

The rate cut is an appropriate response to the market's need for more "money." Stronger demand for money implies lower short-term interest rates.

The Fed's rate cut effectively removes an impediment to growth. It makes it easier for the market to deal with the uncertainties surrounding Covid-19. It doesn't cure the virus and it doesn't boost economic growth. It may result in stronger growth, but the source of that growth will come from the other sources, not the Fed.

The market angst has far more to do with Bernie virus than Corona virus and no amount of fed cut is going to help if Sanders does well again today. He is by far the greatest existential threat the American economy has ever faced.

Scott: The rate cut is now an absence of a negative. It shrinks the gap seen in Chart #2. This is a big deal. Look at what has happened when the Fed let money be too tight for any length of time in the past... For now, we've avoided that.

Prediction: Not that far off we're going to see another round of QE. But this time, instead of buying Treasuries and MBS, the Fed will send it to the people in some form. It'll be a form of a helicopter drop. Trump will like it for the wrong reason and the fail-at-everything Dems won't want to be seen as opposing it.

Another point: It's driving me crazy when people say the Fed is out of ammunition or is running out of ammunition. The Fed is never out of ammunition because they can print money. Not only should everybody know this on a theoretical level, but we've all just lived through three rounds of QE! That's literally creating "ammunition."

OMG, 10 year trading at .97%!

WTF!

Full blown panic in the bond pits.

>The Fed is never out of ammunition because they can print money...

Are we all Modern Monetary Theorists now?

The Fed doesn’t “print money”.

Markets will crash back to Christmas Eve 2018 levels with a Bernie nomination.

Tonite’s Super Tuesday is scary.

Emergency Fed moves have almost always come at the early stages of a down move.

SPLV - TLT combo was barely down today, with market down nearly 3%.

Fed cut 50bps today.

Will market be mitigated?

We are going to need ever-lower rates to offset the cost of neither party having the guts to address entitlement reform. Not to mention the trillion dollar deficits we are now seeing, despite the "greatest economy ever!"

No matter who wins the Dem nomination, the race will have me thinking of a song lyric from way back when -- "clowns to the left of me, jokers to the right".

Tax revenues are up over 4% YOY, to all time highs.

Dont blame the all-time record high GDP, profits and paychecks for the massive deficit.

Revenue is not the problem.

Bernie is sufficiently dispatched tonite. Should bring relief to markets.

MIRACLE! Biden comes out of nowhere to sweep the nation!!!!

1% showing in Iowa to frontrunner.

The RIG is on.

Its his turn.

Looks to me like fed wasted a 50 bps rate cut on bernie virus obfuscated as corona virus.

Steve: That's fine. But I think you should ask yourself: What are Charts #2 and #4 telling me? I think a fair reading of just these two charts - corroborated by many other charts - suggests that the Fed was at least 50bps too tight and likely 75-100. And please note that these two charts reflect deep, liquid markets.

Money was too tight whatever the reason. The Fed took a big step in the right direction.

JBD: In fact, federal tax revenues are rising at a 6%+ pace. The problem is that spending is rising at a 9% pace.

Scott, you nailed it. "The problem is that spending is rising at a 9% pace." NO ONE in D.C. will give up the chance to get re-elected by addressing this. The clock is ticking on "it" hitting the fan.

Thanks for all the info you provide here. Greatly appreciated.

So I agree that fed spending is out of control but one would think logically that bond rates would rise when it becomes problematic. Clearly not the case now.

I read some interesting commentary today by an economic observer named Francis Coppola.

Conventional QE is like helicopter drops on Wall Street, but what we need is helicopter drops on Main Street.

I think there is a lot of Truth in this observation. The Fed prints money and injects it into globalized capital markets when it conducts conventional quantitative easing.

I think a holiday on payroll taxes in the US, offset by the Federal Reserve buying Treasury bonds and placing them into the Social Security Insurance Fund, would be much more effective.

By the way, Stanley Fischer, who is the former Vice Chairman of the Federal Reserve Board has come out in favor of variations of just such helicopter drops.

There are concerns that Main Street helicopter drops would lead to inflation. Maybe so. But with 10-year Treasuries offering less than 1%, I don't think that problem right now is inflation.

I do not advocate wagering, but if you believe Wall Street will not gain in the next several months through November, then you might want to take all your money and bet on President Trump to win re-election. I have never seen a less-appealing major presidential candidate than Joe Biden.

Benjamin, you cannot possibly prefer a Sanders POTUS over Biden. Former is dangerous and would be an existential threat to America, which he HATES. Latter is just stupid and a wimp which means not much would change. I'll take Biden seven days a week. Oh and if Trump keeps saying stupid S&%T about corona virus like he did on Hannity last night ("you should go to work") he can be beaten. Bonds are suggesting a recession also. POTUS 2020 is in play.

Steve--- President Trump is obviously His Own Worst Enemy. But evidently a large portion of the public find his antics appealing. And I confess sometimes I get a laugh out of President Trump. But Trump's policies are not that bad, and I even agree with some of them (though I am disappointed that Trump has not pulled US forces out of Iraq and Afghanistan as he suggested he would when he was campaigning).

But Joe Biden is such a poor campaigner that he actually makes the very annoying Hillary Clinton look acceptable in comparison.

Side note worth pondering: There were 1,100 crew members on the Diamond Princess. They ate and slept in common quarters. All must have at least been exposed to the coronavirus. Not one died.

I am not making light of anyone's death. But the coronavirus is in general not a threat to any non-elderly reasonably healthy adult.

The Tangerine Monster vs. The Dementia Patient. America's image is still searching for a bottom...

And won't find it anytime soon.

The S&P Low Vol - TLT combo was positive again today while stocks were down 3.4%.

Relative strength wins again.

God Bless Donald.

People should go to work.

Wash your hands often, and don’t touch your face. Wipe down surfaces with Lysol wipes.

It’s the flu.

If you have lung disease or a terminal illness, stay home.

Very long time reader thanks Scott.

Post a Comment