If weekly unemployment claims are a good proxy for the health of the economy, then the chart above demonstrates that equity prices have risen in line with an improving economy. Lots of wiggles and mini-panics along the way, but the improving trend in both series remains intact.

The current PE of the stock market is very close to its long-term average, even though corporate profits are at near-record levels relative to GDP. Stocks may be fairly valued, but they are not overvalued by these measures.

The earnings yield on the S&P 500 is still above the yield on BAA corporate bonds. This shows that the equity market is still not very confident in the outlook for earnings, since it is willing to forego the appreciation potential of stocks and give up yield at the same time, in exchange for the relative security of bonds, which are senior in the capital structure.

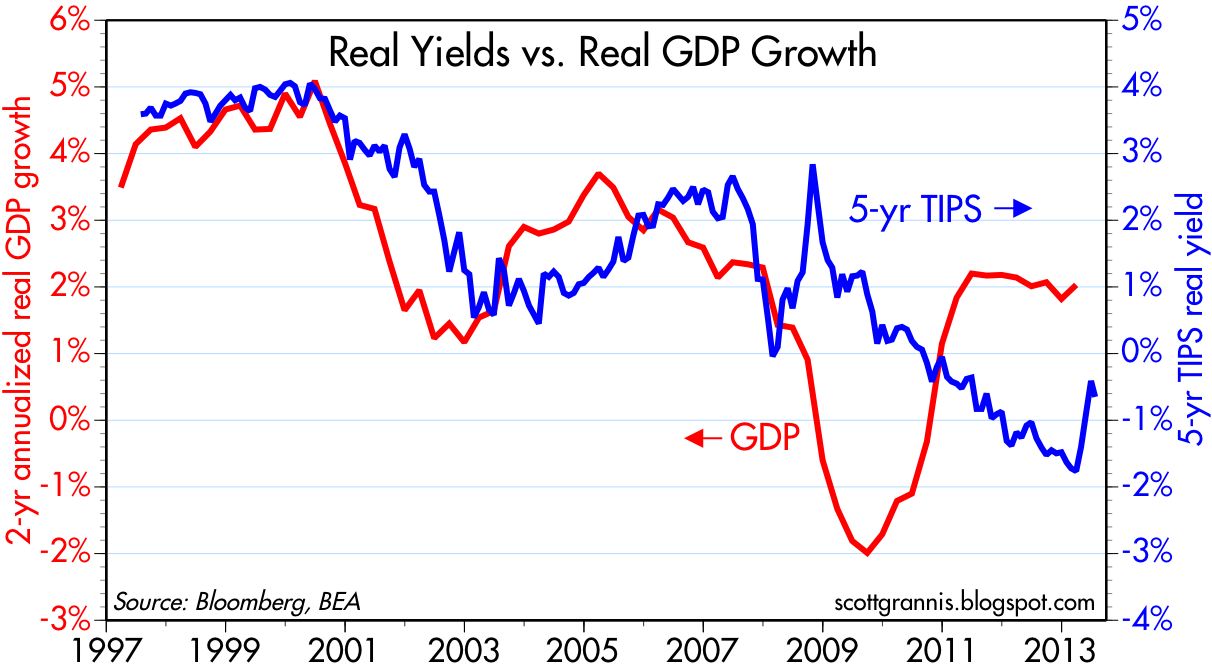

The two biggest changes on the margin in financial markets in recent months have been the decline in gold prices and the rise in real yields (or, if you prefer, the decline in TIPS prices). Both have been tightly correlated for the past 6-7 years (see first chart above). Both TIPS and gold are classic inflation hedges, so their declining prices are symptomatic of declining concern over the outlook for inflation. But as the second chart shows, the recent decline in inflation expectations (the green line) is quite modest when viewed from an historical perspective.

As the chart above suggests, the big rise in real yields/decline in TIPS prices has a lot more to do with the market's outlook for real growth that it does with the market's inflation expectations. The very low level of real yields several months ago was symptomatic of a market that was quite pessimistic about the prospects for growth. Investors were willing to pay very high prices for gold and TIPS because they feared that very weak growth prospects raised the risk of losses in alternative assets. Gold and TIPS are "safe assets" that no longer command such a high premium because investors' fears, uncertainties, and doubts about the future have declined somewhat in recent months. This dovetails as well with recent modest rises in consumer confidence and increased bank lending.

Many worry that declining gold and TIPS prices signal and increasing risk of deflation. But as the chart above shows, it's more likely that gold has declined because it had previously risen by an extraordinary amount, far above the rise in other commodity prices. In the absence of any rise in the inflation rate, gold was going to have a very tough time remaining at such elevated levels. Gold is now in the process of realigning itself with commodity prices. Commodity prices are down from their 2011 peak, but they are still well above (130% above) their 2001 lows. This is all symptomatic of a market that not too long ago had very big concerns about weak growth and rising inflation—concerns that have now been somewhat assuaged. There's nothing here that would suggest deflation.

After a brief, QE-temper-induced uptick, credit spreads have settled back down to their lowest levels since the Great Recession. They are still substantially higher than they were during times of relative tranquility and strong growth (e.g., 1997 and the mid-2000s), but they do not reflect any deterioration in the economy's health, nor any great concerns. The market is now saying that an earlier-than-expected end to QE is not necessarily a bad thing for the economy. The economy will very likely not suffer if the Fed proceeds with a tapering of QE prior to the end of this year.

As the first of the above charts shows, the Vix index of implied equity volatility (a proxy for the market's degree of uncertainty) is relatively low, having declined in fits and starts from extremely high levels during the Great Recession. The market is much less uncertain these days. The second of the above charts shows the ratio of the Vix index to the 10-yr Treasury yield (a proxy for the market's confidence in the health of the economy). Like the Vix index, this ratio has also declined in fits and starts from extremely high levels. You might say that this chart is showing the while the market is less uncertain about what the future holds, it is still not very optimistic about the economy's ability to grow—10-yr yields are only 2.5%, and that is very low from an historical perspective, lower even than during the Depression.

So we are making progress, and the economy continues to grow, albeit at a disappointingly slow pace. Uncertainty is down, pessimism has receded, but enthusiasm is still in relatively short supply.

12 comments:

The economy has certainly been slo-gro for years, and inflation well below 2 percent, the Fed's target---a target one might waive to get out of a recession.

We will see how the market reacts to tapering. Some say the market was calmed when the Fed signaled it will maintain QE. Why the Fed would curtail QE is a puzzle.

An even bigger puzzle is why the Fed is so mysterious and murky about its plans.

Japan ran a QE program 2001-6, coincident to their longest postwar expansion. When they stopped QE, they went back to deflation-ZLB-perma recession. Thus ending the QE program was a mistake back then, and may be for us too.

The very long-term trend in sovereign yields is down over the last 30 years. This may suggest that ZLB is the new adversary, not inflation.

Perhaps it is time to embrace QE as a conventional tool, more or less permanent.

If the option is to do a Japan...then QE becomes your new tool

@Benjamin, the forces behind US monetary policy advocate expanded austerity -- and betting against the Fed is usually a bad bet -- what I do not understand is why the Fed has not simply outlawed consumer lending to all but accredited investors (who earn more than $300,000 annually with more than a $1 million net worth) -- however you imagine this unfolding, my guess is the Fed is about to get dangerously real about austerity -- remember that the Fed measures its success in terms of the Federal economy, which does not include Main Street USA (which remains mired in economic depression as evidenced by long-term declines in real working wages, real home values, and the employment to population ratio) -- in fact, the Fed has a contemptuous view of Main Street USA -- my guess is that the Fed will soon figure out a way to outlaw consumer lending completely for all but accredited investors in order separate Main Street USA permanently from the central (Federal) economy -- the beneficiaries of Federalism from the military-industrial complex, the medical establishment, Wall Street, and Federal workers owe the Fed their gratitude -- those unfortunates along Main Street USA should be under cover watching out for the four horsemen of the apocalypse -- keep front of mind that throughout history, the US has never come to the rescue of the economically disenfranchised, which at times has included emancipated slaves, vast numbers of immigrants, and the American Indians -- life today is grand in the center (especially in Washington, DC) -- think "Hunger Games" and you will understand why monetary expansion is revolting to the top 1% in America -- the only good news is that ordinary people can escape the misery of the 99% crowd, and instead join the top 1% crowd simply by acquiring world-class skills that earn premium wages that convert into dividend and rent-earning equities over a lifetime -- the reality is that real working wages for those lacking world-class skills are regressing to global norms right before our eyes, a trend that will continue over the balance of the 21st century.

You wrote, The market was initially spooked by the prospect of a QE unwinding, but now has put those fears to rest.

I've been reading John The Revelator, specifically Revelation 13:1-4. And I've been reading Witness Lee on the Economy of God, specifically Ephesians 1:10, and my fears of a soon coming Financial Apocalypse have been heightened

The days of risk on investing, ONN, are over, though, done, and finished. Small Cap Pure Value, RZV, and Biotechnology, IBB, both traded lower today from market highs.

The short selling opportunity of a lifetime has developed. Look for strong derisking to come out of fiat asset invesment leaders, XIV, FDN, CARZ, PBS, IGV, IBB, RZV, PSCI, PBD, PPA, IAI, SPHB, SMH, XRT, PJP, EWN, PSP, UJB, KRE, TAN, RXI, WOOD, FLM, LNKD, RF, LYG, SMFG, BPOP, SLM, JPM, NNI, UBS, BLK, NMR, MKTAY, seen in this Finviz Screener ... http://tinyurl.com/l9l3bmp

The slight trade lower seen in the chart of the S&P 500, $SPX, SPY, to $1,692, very likely reflects a market high yesterday Monday, July 22, 2013, at 1696, as an Elliott Wave 5 High, as S&P High Beta, SPBH, traded, 0.3%, lower today, and, S&P Transports, XTN, traded 1.2% lower, today. Large Cap Financials, JKF, including Life Insurance companies, such as, PRU, seen in this Finviz Screener, rose to new rally highs, suggesting that a market top in the S&P 500 has been attained. S&P overweight Exxon Mobil, XOM, traded to an all time new high of 95.

Jesus Christ, operating in the economy of God, that is the political and financial administration plan of completing every age, epoch, era and time period, bringing forth its total fufillment, likely pivoted the world fully out of the era of investment choice and into the age of ditkat, today July 23, 2013; a process which He began on May 24, 2013, when the Interest Rate on the US Ten Year Note, ^TNX, rose strongly to 2.01%, serving as an “extermination event” which terminated Liberalism and introduced Authoritarianism; this rate rose again today from its recent low of 2.49% to 2.52%.

Volatility, ^VIX, finally rose. The walking dead market, that is the zombie market is likely over. Liberalism’s schemes of credit liquidity, AGG, FLAT, and carry trade, ICI, funded safehaven investing probably came to an end today, Tuesday, July 23, 2013. The safe haven rally in US Based stocks appears to be over, as the premium of Biotechnoloy over Emerging Markets, seen in the chart of IBB:EEM, has exhausted. And the safehaven rally in the Netherlands, EWN, appears over as its Electronic Equipment Manufacturer, PHG, and its Scientific Instrument Manufacturer, ST, traded lower. And the safehaven rally in Design Build Companies, FLM, appears over as its leader, JEC, traded lower. And the safe haven rally in Leveraged Buyouts, PSP, appears over as two of its leaders, IP, and GE, traded lower. There now be no more safe haven investments from the terror of bond vigilantes calling interest rates higher globally and the currency traders following suit with competitive currency devaluation.

The rise of Authoritarianism’s schemes of debt servitude, such as Greek Bailout III, and the Cyprus Bank Deposit Bailin, mean that wealth can only be preserved in the physical possession of gold bullion, or in Internet trading vaults such as Gold Is Money or Bullion Vault.

William-

Thomas Jefferson said the only thing more dangerous to a prosperous democracy than a standing military was a central bank ran by bankers.

Jefferson would not like our odds right about now.....

Scott, is this statement accurate: "by raising the interest rate it pays on bank reserves." ??

I believe you meant either lowering the interest rate it pays on bank reserves or raising the Prime rate. No ?!

I thought as a part of its stimulus efforts, the Federal Reserve had already raised the interest rate it pays on bank reserves to 0.25% so as to increase banks incomes when they desperately needed to rebuild their balance sheets.

William: You raise an important point. Yes, the statement is accurate. When the Fed decides to begin "tightening" policy, it will only be able to do so by raising short-term interest rates, beginning with the rate it pays on bank reserves. The funds rate is no longer an effective tool, because of the abundance of bank reserves. Instead of reducing the amount of reserves in order to raise the funds rate (the old way of tightening), the Fed will now have to raise the rate on reserves, and that will signal other rates to rise as well. This won't happen any time soon, however, but when it does it will be a welcome event in my book.

@William McKibbin, the Protection Bureau is the vehicle from which consumer lending will be curtailed.

Scott, if the Fed winds down the bond buying to zero while keeping the Fed Funds Rate at near zero (or not raising the rate it pays on reserves), what would be the likelihood of inflation then? And isn't that the course we're on?

Chris: the Fed has said that the unwinding of QE will occur in two phases: first, they taper the purchase of bonds to zero, meanwhile keeping short-term rates close to zero; then they begin to reduce their bond holdings while also raising short-term rates. That doesn't necessarily have to be inflationary. It all depends on when and by how much they do this, and what happens to the demand for bank reserves in the meantime. If they are slow to react, then banks will ramp up their lending activity, thus potentially expanding the money supply by more than the demand for money, and that could be inflationary.

Why would inflation expectations decline when market is less pessimistic about growth?

Whenever I read Your Post Allways got Something New

Laboratory Equipments

Post a Comment