Stocks initially sold off, Treasuries rallied, and gold fell, all signs that the market was disappointed there would be no more quantitative easing. But as often happens, the market's initial reaction was subsequently reversed. What that tells me is that, upon reflection, the market has decided that the Fed did the right thing. We don't need more QE to get the economy going.

The one thing the Fed could do to help would be to more forcefully explain to the world that monetary policy cannot stimulate growth. The Fed has done just about all it needs to do in order to accommodate the world's massive appetite for dollar liquidity; doing more would only risk inflation and a weaker dollar. To get the economy moving again we need stimulative fiscal policy, and by that I mean government spending cuts, a broadening of the tax base via the elimination of deductions, loopholes, and tax credits, and a lowering and flattening of tax rates.

Just in case you missed it, do read David Henderson's essay today which explains how gigantic cuts in government spending at the end of WW II not only failed to tank the economy but actually led to a huge boom. The Keynesian view that cuts to government spending would hurt the economy are unfounded. With government spending now close to record post-war levels, reducing the burden of government would unleash powerful private sector forces that would almost surely boost economic growth.

To recap the state of monetary policy, the chart above shows bank reserves, which are currently about $1.6 trillion following the Fed's two rounds of quantitative easing.

Of that total, $100 billion of reserves are currently "required" in order to back bank deposits per our fractional reserve banking system. That leaves $1.5 trillion which are "excess" reserves sitting idle on the Fed's balance sheet. Banks have been slow to use the massive amount of reserves the Fed has dumped into the system via its purchases of MBS and Treasuries. That's mainly because reserves are now functionally equivalent to 3-mo. T-bills, since the Fed now pays banks interest on the reserves they hold. In fact, reserves are even better in a sense than T-bills, because reserves earn an interest rate of 0.25% while 3-mo. T-bills only yield 0.09%. Banks are holding reserves because they want to bolster their balance sheets and because they are still very risk averse. The extremely low level of yields on T-bills is proof of the intense demand for safety. Indeed, if the Fed had not engaged in quantitative easing there would have been an acute shortage of risk-free dollar liquidity, and that could have precipitated a global depression and/or deflation.

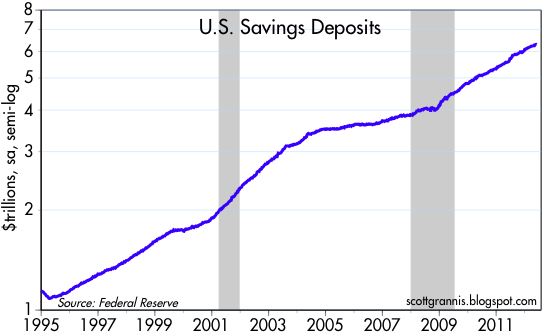

The entire world in fact is still very risk averse, and you can see that in the huge growth of savings deposits in U.S. banks, which now total some $6.3 trillion. Savings deposits have surged from a low of 10.6% of GDP in 1982 to over 40%, and much of that increase has occurred over the past 4 years, as can be seen in the chart below, which shows the ratio of savings deposits to nominal GDP.

Other signs that the Fed has done enough quantitative easing can be found in the following charts.

2-yr swap spreads are back to normal, a sign that the banking system is functioning normally and systemic risk is low. Banks have access to all the liquidity they need; the world is not starved for liquidity.

Not only is there no shortage of dollars, there is actually a relative abundance of dollars in the world to judge by the dollar's weakness relative to other currencies.

As the first of the two charts above shows, credit default swap spreads have fallen significantly from their recession highs, a good sign that credit conditions have improved dramatically. Spreads are still somewhat elevated, however, but I would argue that has little to do with Fed policy and everything to do with the ongoing Eurozone financial crisis and the extremely low level of short-term Treasury yields, which in turn is being fueled by the world's extreme risk aversion. As the second of the two charts above shows, corporate bond yields are about as low as they have ever been: credit spreads are still elevated because low corporate yields are being compared to exceedingly low Treasury yields. The fact that the world is happy to buy investment grade corporate debt with yields as low as 3.8% suggests the outlook for corporate profits is excellent. And indeed, corporate profits are very close to record-high levels, both nominally and relative to GDP.

On the margin, gold and commodity prices are off their recent highs. Many analysts argue that this is a sign that the Fed has inadvertently tightened policy and that more quantitative easing is therefore necessary. My interpretation is somewhat different: I think the recent "weakness" in gold and commodity prices is a sign that monetary policy has become "less easy." Gold and commodity prices are still trading at very lofty levels compared to where they were 10 years ago when the Fed first embarked on an ambitious program to easy monetary policy. Monetary policy was indeed tight in the late 1990s and early 2000s, but that's certainly not the case today.

Finally, as this chart shows, forward-looking inflation expectations are not displaying any evidence at all that the Fed is too tight. This chart shows the market's implied 5-yr inflation rate 5 years in the future (i.e., the expected average annual inflation rate five years from now for the subsequent 5 years, as derived from TIPS and Treasury prices; i.e., the expected average inflation rate from 2017 through 2022), and it is right around where it has been for a long time—neither high nor low. This is the Fed's preferred measure of inflation expectations. In the absence of any decline in inflation expectations, such as occurred in late 2008, and in the fall of 2010 and 2011, it would have been very hard for the Fed to justify another round of easing today. If anything, I would note that inflation expectations have increased slightly this year.

16 comments:

We need infrastructure spending along with a broadening of the tax base.

As for spending cuts, when do we pay for the wars being waged and the Medicare drug benefit that Republicans enacted?

When that's done, we can cut spending.

You need to read the Bernanke tea leaves. They point to all systems go later this year. The entire banking system is now dependent on low rates, money printing, and bailouts.

But everyone knows this by now...

I absolutely concur that federal agency and entitlement spending should be cut. I just wish the GOP and D-Party concurred with that.

On monetary policy, I contend Grannis is fighting the last war.

The prime enemy is no longer inflation, nor the goal a "strong" dollar.

A strong dollar is one that helps exports and the US tourism industry. Deflation may be a larger threat and then inflation.

On exchange rates: Alone, they tell us little. It may be our major trading partners are running monetary policies that are too tight (certainly true in the case of Japan). If they wish to suffocate themselves, that is their business, but it is no reason to try to keep the dollar in a certain trading range, and asphyxiate ourselves also.

Conversely, if our major trading partners suddenly printed a lot of money, we should not try to keep up and keep the dollar in a certain range.

The dollar, which retreated against major currencies in the Bush jr. Administration, has been about flat since Obama took office. If one follows Grannis' reasoning, that means the Fed printed a lot of money in the Bush jr years, then firmed up under Obama.The dollar is back to 1990s levels. Is that strong or weak? Seems a little high to me---US manufacturing doing well now, but I still do not see tourists coming to the USA. It may be we have little to offer---Cleveland is not Bonn or Fiji---but it may be the dollar should be lower.

I hope the right-wing orthodoxy can adjust to the world of the 2010s, instead of the 1970s. Yes, less federal spending---and more monetary bullishness.

Given the austerity track (the opposite of monetary expansion) that the US is now on, the situation in Ireland is probably a good picture of where the US is going in the coming year -- austerity measures will be designed to rout public services and employment in detail -- moreover, small businesses will increasingly be wiped out as the Main Street depression expands under the weight of austerity -- people who make a living along Main Street will see their wages continue to decline if they can even remain employed -- however, the restructuring of the US into a Federal economy means the end of regional and local enterprise, as well as state government -- it's all part of the "big strategy" of central bankers who hate Main Street and adore Federally-sponsored enterprises.

The good news is that large public corporations in the US will do well under the emering corporate-government alliance that is likely to accelerate under a Romney administration -- assuming Obamacare, Social Security, and Medicare are repealed, there will be no reason for poor people (those earning less than $250,000 annually) to remain in the US -- the real possibility of massive emigration by US citizens over the balance of the century is increasingly likely for survival of those who are unable to earn world-class wages.

Massive emigration out of the US will serve to ease the unemployment problem, the requirement for public education, and the need for social welfare -- in contrast, accredited investors with means and skills will be looking forward to the best of times.

Emigration out of the US is likely to begin in earnest once the Romney administration takes the reigns of power and imposes martial law over the countryside to enforce the most severe forms of austerity and political repression, which is likely to lead to the end of society as we know it within Romney's first term -- in particular, retirees without means will find survival difficult to impossible under Romney's vision for the future.

As for accredited investors, "the future looks bright -- gotta wear shades!"

More about Ireland here:

http://www.vanityfair.com/business/features/2011/03/michael-lewis-ireland-201103

PS: Still more about Ireland here:

http://en.wikipedia.org/wiki/2008%E2%80%932012_Irish_financial_crisis

"The Keynesian view that cuts to government spending would hurt the economy are unfounded." (from your commentary on the Henderson essay).

Don't know in what work of Keynes you found such a statement. Keynes' great contribution to economic thought (writing in 1935)was that AGGREGATE demand drives the macroeconomy. Obviously in the 1946 through 1949 period greatly increased aggregate demand from the private sector replaced the USG spending on war production.

BTW: A great deal of the increased private demand in the immediate post-war period could easily be said to be USG sponsored. VA housing loans, GI education benefits, continued suppression of interest rates by the Fed, etc. An economic success story to be sure, but it hardly leads to the conclusion that "reduced USG spending led to a boom".

"...reducing the burden of government would unleash powerful private sector forces that would almost surely boost economic growth."

If by the burden you mean federal tax receipts as a percentage of GDP, then this era is the least burdened economy since 1949-50. Tax receipts are running about 3% of GDP less than the post-WW11 average. So there is about $450 billion additional dollars in the private sector and there is no supply side boom. Hmmm...

Dr. McKibbin thanks for the irish article in Vanity Fair. Its misty and rains a lot here (and getting worse in the 9 years I've been here)so the vague shapes you see could be fairies or piles of gold. Yes the Irish are delusional - they won independence (Britain no longer needed it for strategic reasons) - there was a Celtic Tiger (Germans are good savers but dumb investors).

"Savings deposits have surged from a low of 10.6% of GDP in 1982 to over 40%"

I wouldn't key off of the 1982 low. It's a data break. There was a reclassification of savings deposits as a result of the deregulation of the savings and loan industry in 1982. So from 1979 to 1982 money left traditional "savings deposits" institutions and flowed to "non-savings deposits" S&Ls and which were then reclassified as deposit savings. But the doubling of savings deposits since 1980 is about right.

Re the burden of government. The true burden of government is not measured by taxes as a % of GDP, but by spending as a % of GDP, as Milton Friedman told us long ago. Ultimately, all spending must be paid for by taxes, either now or in the future.

"Ultimately, all spending must be paid for by taxes, either now or in the future."

Other than during a brief period near the end of the Clinton presidency, no one in two generations has paid current or future taxes for spending in excess of receipts.

The Keynes dictum should be amended: The long run is a misleading guide to current affairs. In the long run we are all equally dead after our free lunch.

Regarding paying for past and future obligations, I agree that taxes are required in both cases -- however, those with means will soon be looking for safehavens in countries that are debt-free, defense-spanding free, and entitlements free -- watch and learn -- capital flight is the obstacle to paying down past and future obligations in any manner -- which is exactly why default in some form is the historical norm of empires...

More on spending: Even if the current generation never pays for all the spending that occurs today through higher taxes, the level of spending is still the best measure of the burden of government. By spending money the government appropriates resources from the private sector by taxing and/or borrowing. Those resources are arguably consumed in a manner which is less efficient than if they had been consumed by the private sector. To the degree that spending involves transfer payments from those that work to those who don't, spending creates perverse incentives, weakening the economy. Government spending therefore wastes scarce resources and creates anti-growth incentives, all of which is a burden on the economy.

I hope you consider financial repression as governmnent spending. What do you think that is costing taxpayers annually???

Eventually economists will stop patting Bernanke on the back for 'saving' us from a depression created by none other than the Federal Reserve itself.

"Stocks initially sold off, Treasuries rallied, and gold fell, all signs that the market was disappointed there would be no more quantitative easing. But as often happens, the market's initial reaction was subsequently reversed. What that tells me is that, upon reflection, the market has decided that the Fed did the right thing. We don't need more QE to get the economy going."

I guess you spoke too soon. Seems the market is very disappointed that there is no QE3. Not yet at least.

"Government spending therefore wastes scarce resources"

Then Americans love the appropriated waste of scarce resources to the tune of $5trillion.

Half of U.S. publically traded debt(liability)is owned (asset) by Americans which gets passed down from generation to generation. The only issue is the distributional aspect as the asset is becoming increasingly concentrated in the upper decile.

Americans can tell foreign asset holders of the pubic debt (and I'm not advocating this tact)... China, Japan etc. to eff off and then there are no wasted resources.

___________________

BTW, on second thought, your savings deposit thought should be the ratio to financial assets not GDP. A quick look at the Fed's Flow of Funds Table B.100 shows that the ratio increased from 13% in 2005 to 16% today. No big swing.

Post a Comment