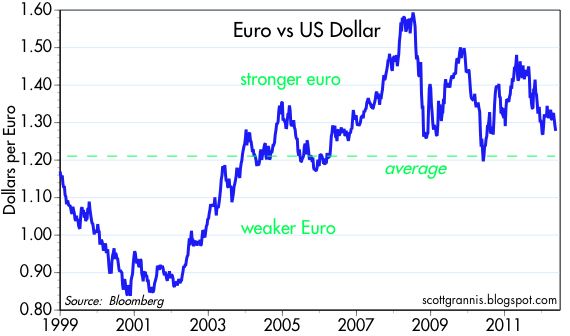

With the world's worst fears dominated by events unfolding in the Eurozone, and with the euro's continued existence a key question, I offer some charts which perhaps provide some useful perspective. Despite all the fears of cataclysmic outcomes, the euro has actually strengthened vis a vis the dollar since its 1999 inception, and the euro today is trading about 10% above its purchasing power parity relative to the dollar by my calculations. This suggests that the ECB has been doing a pretty good job of defending the euro—better even than the Fed.

The euro today is slightly higher against the dollar than it was at its inception. It's been a long roller-coaster ride, but I see nothing here that would point to an imminent collapse. What seems more likely is a further gradual decline of the euro vs. the dollar.

The euro (using the DM as a proxy going back prior to the inception of the euro) has been trending higher against the dollar for the past 40 years, primarily because inflation in Europe has been lower than in the U.S. Purchasing power parity theory conforms with this experience; the currency with lower inflation should outperform, over time, the currency with higher inflation (the inflation differential between the U.S. and the Eurozone is reflected in the green line on the chart). The inflation differential that has favored the euro is ultimately the result of tighter monetary policy in Europe. The gap between the blue and green line suggests that the euro is about 10% "overvalued" against the dollar, which means that an American tourist in Europe is likely to find that most goods and services cost about 10% more in Europe than they do in the U.S. By the same logic, European tourists to the U.S. are likely to find that things are about 10% cheaper here.

The ECB can take credit for maintaining the purchasing power of the euro even as the world's demand for euros has weakened as a result of the Eurozone crisis, even as the world's demand for safe-haven currencies has been intense, and even as the Eurozone financial crisis has required the ECB to inject massive amounts of liquidity to shore up its banking system. But the strains are showing, and I think the euro is likely to weaken some more.

This chart shows the price of gold in the world's three major currencies. Here again we see that the dollar has lost purchasing power against the euro (because the price of gold has risen more in dollar terms than it has in euro terms). The yen has been the strongest currency of all for the past several decades; the price of gold in yen today is still less than it was at the gold's peak in the early 1980s.

The dollar is weak against the great majority of the world's currencies, and the Fed's Real Broad Dollar Index shows indeed that the dollar is very near its all time lows. But the euro's resilience in the face of great adversity, and the dollar's rather extreme weakness in general, don't mean the dollar is doomed. I've been arguing for awhile that the dollar was likely to rise this year against other developed currencies, because I think the economy is going to end up doing better than expected, and I continue to believe a stronger dollar is likely. The ECB is going to have a tough time maintaining its tight-fisted stance (relative to the dollar, that is), since the Eurozone financial system is still far from being out of the woods, and the Bank of Japan already is making a real effort to keep the yen from appreciating further. If the ECB and the BoJ have to further expand their balance sheets to achieve their goals, this could result in additional supplies of euros and yen relative to the dollar, thus supporting the dollar's value in a relative sense. And if the U.S. economy continues to beat expectations, then demand for the dollar could strengthen, and that in turn could provide a tailwind for the Fed's efforts to drain liquidity as the economy improves.

11 comments:

Scott...I have a question..can you

explain the significance ( if any) of

the large drop in the 3 month euribor..the 3 month euribor on October 28,2011 was 1.59%...today it

is .68%...comparatively speaking the

2 year euro swap spread was 97 on October 28,2011 whereas it is 92 today not a significant drop...are

we talking apples and oranges here??

Mostly apples and oranges. Euribor, like Libor, is the rate large banks charge each other to lend excess funds for short periods. It is generally closely tied to the expected short-term target rate of the respective central banks. A declining Euribor/Libor rate thus means the market expects central bank target rates to fall. Swap spreads, on the other hand, are in a sense a measure of the default risk of large banks. Spreads and rates don't always, nor do they have to, move together.

If America was more fiscally responsible, I suspect that the Gyro would be trading at less than par.

IMHO, the outlook for Europe is bleak, on many fronts. The European Economic Sphere and it's script, was designed in part to challenge America both politically and economically. In this aspect, the Brits were indeed very wise.

In order to succeed, it will have to destroy all vestige of nationalism to the refrain - we are all now Europeans! That mechanism will require the continuation of socialist policies. GL with that.

In the subset of the EES, will you always have failing states, who know full well that there is always a bag of largess awaiting the unfortunate, under the guiding principle of - it takes a village..

I hope I live long enough to see the demise of this unnatural alliance..

Why exactly is the Yen so strong against gold and the dollar. It would seem like the same things that are causing some people to claim that the dollar is doomed would have weakened the Yen.

Interest rates there are barely above zero and deflation is a bigger worry than inflation. It doesn't seem like there's a coherent story for why the US needs to start bringing down the deficit today that also explains the Japanese experience. Am I missing something?

Japan is proof that monetary policy can keep a currency strong even if government debt and deficits are huge, and even if the economy is lackluster. Debt doesn't create inflation and weak currencies, central banks do.

Could it also be that Nippon is the world's largest creditor nation?

Scott- I'd agree and I certainly think that the Fed sets interest rates. THe question then is what's the argument against the US say cutting payroll taxes to 0 in an effort to expand our underperforming economy and then putting them back when our growth is back on trend? With control over interest rates at the central bank, then why shouldn't the government use fiscal policy to smooth out aggregate demand?

KD: the only solution that will work is a supply-side solution. That involves cutting back the size of government, and cutting taxes permanently while at the same time drastically simplifying the tax code. The government has to stop suffocating the private sector. Payroll tax cuts are worthless, since they don't change incentives on the margin (since no one believes they will be permanent) and they only grow the deficit.

Scott- How can you be sure it's a regulation issue rather than a consumer balance sheet issue? It seems like there's a pretty clear connection between the still high private sector debt levels and lower consumer spending. I can see an argument that no matter what incentive structure the corporate sector gets, they can't expand without demand levels improving. Profits are pretty high right now without any real improvement in hiring or wages, so it's hard to make the case that the supply side is where the policy help needs to come.

KD: you've got the cart before the horse. Demand doesn't create growth. Growth creates demand. Growth comes from working harder, inventing new stuff, making things cheaper, and investing/taking risks. "Supply creates its own demand," as F. Say famously wrote. Corporate profits could fuel a huge investment and employment boom, but risk remains high: tax rates are already very high, and the threat of higher tax rates and more regulation becomes a significant barrier to new investment. The public sector is soaking up most of the earnings and idle resources of the private sector and doing nothing productive with the money.

I don't mean to be disagreeable, but that's what the internet is for?

I'm not so sure that's right. There's obviously a mix of the two so it's not 100% supply or demand led. But if I'd like to build a shopping mall or add 50% to my company's production capabilities that decision is will be based on what I think I can sell. An engineering firm doesn't lay off people if it has a full order book and restaurants will hire more staff if they have more diners. I can certainly see how regulation and tax uncertainty would be a drag so I don't mean to ignore it, but the current problems are huge and I can't believe that in 2008 everybody suddenly decided to go Galt all at once. The balance sheets suddenly becoming a problem makes more sense I think.

Post a Comment