Commodity prices just keep on rising. Does this pose a threat to economic growth? I don't think so, and this post offers a few reasons why.

The CRB Spot Commodity Index is my favorite measure of non-energy commodity prices. While it is indeed making new nominal highs almost daily (first chart), and prices have almost tripled in the past 10 years, on an inflation-adjusted basis these same commodities cost about the same today as they did in 1970. Believe it or not, we have seen commodity prices do a complete round trip over the past several decades, and they are now back to where they started. (Incidentally, this same index of commodity prices rose about 15% from 1960 to 1970 in nominal terms, while it fell about 8% in real terms.)

As the second chart above suggests, monetary policy has had a lot to do with the big, secular swings in real commodity prices. Easy money throughout the 1970s induced a worldwide preference for hard assets, and commodity prices were relatively expensive back then as a result. Tight money in the 1980s and 90s undermined that preference by making financial assets (especially bonds, which offered unusually high real interest rates during most of that period) more attractive, and by increasing the effective demand for money by restricting its supply. For most of the past 10 years, the Fed has been generally accommodative (especially in the past two years), and the world has once again gained a new appreciation for hard assets. If tight money depressed commodity prices in the 80s and 90s, easy money has now removed that depressant from the market. And if commodities were cheap in the 80s and 90s, they are now no longer cheap and perhaps only somewhat expensive relative to their long-term historical price range.

Oil prices are still a bit shy of their all-time nominal highs, but they are rising daily, and at this rate we could see $145/bbl oil again (the high-water mark in mid-2008) before the year is out. As the chart above shows, peaks in oil prices have a strong tendency to coincide with recessions. Is this causation or coincidence? I would argue that high oil prices are not the cause of recessions, but rather are symptomatic of the easy money and rising inflation that have lead the Fed to tighten monetary policy—and it is tight money that has caused almost all recessions. Regardless, should we worry about a double-dip recession because of rising oil prices today? For one, I seriously doubt we'll see a recession anytime soon, because monetary policy is not going to be tight enough to cause a recession for a long time. On the contrary, monetary policy is currently very accommodative, and this significantly mitigates the negative impact of rising energy prices.

Another good reason not to worry about rising oil prices is that the U.S. economy has become much less dependent on oil over the years, and real oil prices are only marginally higher today than they were in the early 1980s. As the chart above shows, our economy requires 58% less oil to produce a unit of output today than it did in 1970.

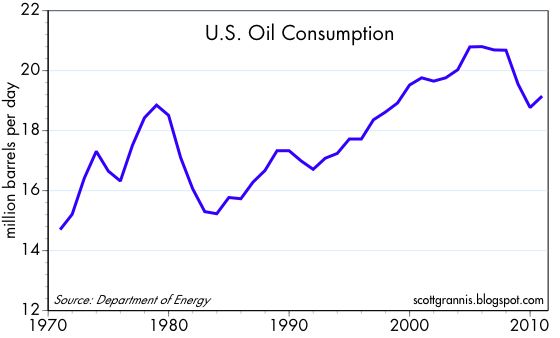

The major surge in oil prices in the 1970s led to a massive effort to reduce oil consumption and become more energy efficient. As a result, U.S. oil consumption today is about the same as it was in 1980, even though the economy has grown by 125% in the intervening years.

Meanwhile, today's relative high oil prices are already encouraging more drilling and exploration; Baker Hughes reports that world oil and gas drilling activity has soared 75% since mid-2009. And expensive oil will undoubtedly encourage more conservation and further the search for and development of alternative energy sources.

Oil is once again expensive, and gasoline is about $4 per gallon. That's unfortunate and painful for many, but it's not a catastrophe by any stretch.

5 comments:

Scott, I do not believe there is a shortage of oil, why then are gasolene prices soaring.

Also with the coming inflation do you have any thoughts whether it will drive real estate prices higher.

Thank you,

Jay

I think monetary policy has already been easy enough to give a significant boost to real estate prices once the banks get close to selling off their excess inventory of foreclosed homes, the economy strengthens, and incomes rise. Real estate stands out today as being among the cheapest asset classes around. Rising inflation is almost always good for real estate.

Re oil prices: don't forget that we have an "artificial" shortage of oil today since the U.S. government has severely restricted offshore drilling permits and geopolitical turmoil in the Middle East threatens to further restrict supplies. Oil demand, meanwhile is very strong as countries like India and China rapidly enter the modern age and their demand for energy rises.

Regardless of US monetary policies, oil prices will crack sooner or later. More than $100 a barrel, and all sorts of alternatives and conservation moves make sense. Crude oil demand goes flat from here.

Indeed, let it ride at $100 for a few years. OPEC may find it has ruined the market for good.

Erratic supplies, threats and price spikes--that is not how to build a customer base.

How much oil is left? Might need to factor that into your model.

Listening to the middle East talk about how much oil they have is about as smart as listening to TEPCO tell you radiation levels are safe for your kids.

We are heading towards another pivot point but you are probably right we have some time before we get there.

Post a Comment