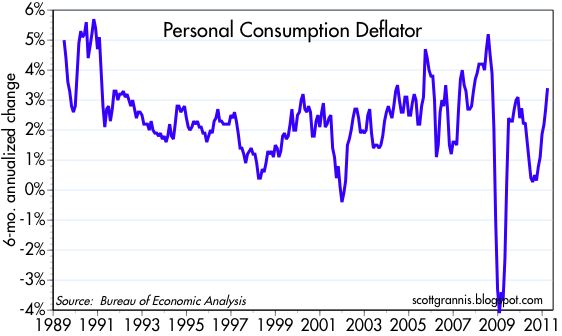

On a year-over-year basis, inflation according to the Personal Consumption Deflator remains within the Fed's target range.

On a shorter time frame, however, the pace of inflation is picking up. Over the past six months, the headline PCE deflator is up at a 3.4% annualized rate, and the Core PCE deflator over the past three months is up at a 1.9% annualized rate. The fact that both headline (total) and core inflation (ex-food and energy) are rising at a faster rate at the same time is consistent with the fact that the Fed is indeed in an accommodative mode, and willing (and wanting) to let all prices rise. They are getting their wish, which is not surprising. The rise in measured inflation is still relatively tame, however, but it will be very important to see how this unfolds in coming months.

This last chart shows the major sub-components of the PCE Deflator (services, durables, and non-durables). Since 1995, headline inflation has been subdued by a previously-unprecedented decline in durable goods prices (i.e., this is the first time in the history of this series that the blue line has declined on a sustained basis). It is probably not a coincidence that 1995 marked the first year in which China pegged its currency to the dollar (thus stabilizing and eventually strengthening it), which in turn set the foundation for strong export-led growth. This chart also helps explain why there is so much confusion over whether we should worry about inflation or deflation, since there is evidence of both.

The chart also tells a very interesting story. Since 1995, service sector prices have risen by 55%, while durable goods prices have fallen by 26%, for a 110% relative price change (this is roughly equivalent to saying that one hour's worth of work in the service sector today buys twice as much in the way of durable goods as it did in 1995). To the degree that China's exports of durable goods have contributed to this relative price shift, it is a testament to how the increased productivity of the Chinese workforce has resulted in a significant rise in living standards for workers in the industrialized world. Contrary to what uninformed critics say, global trade is a win-win situation for all concerned.

6 comments:

testing comments

Scott -

So what do you think of an investment in TBT here? Still too early??

Thanks.

Can't say I find sub-2 percent rates of inflation to be a worry, except that such rates might be too low. The USA economy probably needs a long slug of mild inflation to pay down debt and revive real estate.

Our federal government runs chronic deficits, and will for decades. Mild inflation pays off that debt, and prevents it from growing relative to GDP. I would prefer balanced budgets, but that will not happen.

The strength in commodities is actually a good sign showing strong global demand.

Japan has had tight money for decades and commodities boomed. We will have the same luck fighting commodities inflation through tight money.

Commodities are global markets, and we are becoming a smaller portion of the global economy with every year.

If anything, Bernanke is being cautious, I think too conservative. John Taylor, Milton Friedman and Bernanke all visited Japan, and all advised heavy QE for Japan.

I think that advice is correct, although maybe now Bernanke can consider reducing interest payments on bank reserves.

Hello, I'm curious as to how you can rely on these government inflation indicators. It has been well documented that baskets of goods used to measure CPI in particular have been meddled with over time to skew perceived inflation to the downside. The folks at Shadowstats.com have run their own indicators that go to show what inflation looks like without this meddling. Other than give us insight into Fed Policy (based on these doctored inflation numbers) then I see little reliability in using such indicators to measure actual rates of inflation. What are your thoughts here?

Re the reliability of government statistics. I'm aware of the criticisms of govt stats, and of shadowstats.com. I have spent decades using and manipulating govt stats and I have yet to find that the numbers don't make sense. I think it would be very difficult if not impossible for those who put together the numbers to fudge them by any meaningful amount without the manipulation becoming obvious.

The only case of govt stat manipulation that I'm aware of is in Argentina, where the official CPI numbers don't make sense at all, and there are legions of analysts who believe the same.

Fed leadership (sic) are praying for inflation. The don't care if they spend a devalued currency - just as long as their pockets are full.

Post a Comment