To recap the key monetary events of the past two years: Massive government transfer payments during the Covid era ended up being monetized and stored in bank saving and deposit accounts by a public largely unable and not very willing to spend the funds. As a consequence, the M2 money supply grew by some $6 trillion over the two-year period ending March 2022, a pace that far exceeded anything in our monetary history. All that extra cash was fine—as long as the public was willing to hold onto it. But when people emerged from their Covid cocoons in early 2021, they unleashed a tsunami of spending which overwhelmed supply chains and boosted prices for nearly everything. Inflation, as a result, surged to almost 10% by last June.

Where things stand today: The monetary fuel for the inflation fires is running out. As I've been reporting for most of the past year, M2 growth is slowing dramatically and inflation has most likely peaked. The Fed has been slow to react from the very beginning, unfortunately, but it is already apparent that no further rate hikes are needed.

Meanwhile, the market and the Fed are worried about the wrong thing. Yesterday Bill Dudley gave voice to these concerns when he said that "the Fed needs to restrain economic activity" in order to bring inflation down. That's just plain wrong; inflation is not a by-product of economic activity, it is the by-product of unwanted money. Case in point: economic growth in Q3/22 and Q4/22 is quite likely to be 3-4%, up from -1% in the first half of the year, while inflation is quite likely to have declined from the 8-9% pace of the first half of the year to 4-5% in the second half. Moral: economies thrive with lower inflation and struggle with high inflation. Today's sharply higher interest rates have strengthened the demand for money, thus mitigating the inflationary potential of what is still an elevated level of M2.

The following charts update this most important of all stories.

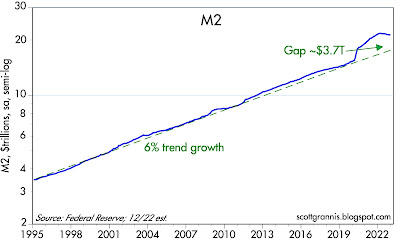

Chart #1

As Chart #1 shows, the $6 trillion M2 bulge is shrinking, both nominally and relative to the size of our growing economy. Excess money is being withdrawn, and lower inflation is the inevitable result.

Chart #2

Chart #2 shows how surging growth in the M2 money supply (blue line) was fueled by massive government deficits of equal size (roughly $6 trillion). Fortunately, over the course of the past year the money-printing press has largely shut down: ongoing deficits are no longer being monetized, and meanwhile M2 is shrinking.

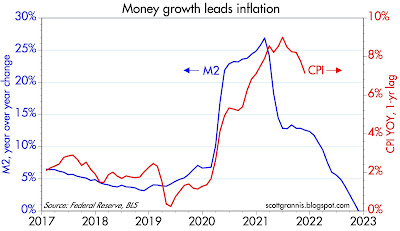

Chart #3

Chart #3 compares the year over year growth of M2 (blue line) with the year over year growth in the Consumer Price Index (red line) lagged by one year, in order to show that the big surge in M2 that occurred in M2 from 2020 to 2021 explains quite well the surge in inflation that followed about one year later. The big drop in M2 growth which began a year ago is responsible for today's lower inflation. The chart further suggests that inflation could easily drop to within range of the Fed's 2% target later this year or by early next year.

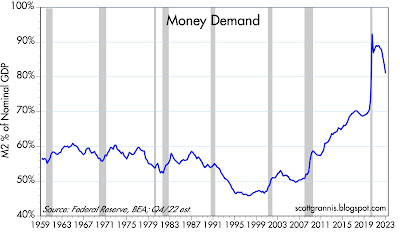

Chart #4

Chart #4 is one of the most important charts, in my view, yet very few people are paying attention. It shows the ratio of M2 to nominal GDP, which I've called Money Demand. In essence, it shows how much of our annual incomes (using GDP as a proxy) we are willing to hold in the form of readily spendable cash, bank deposits, money market funds, and savings accounts (using M2 as a proxy). The ratio soared in the initial phase of the Covid era, and it has been falling ever since mid-2020. The Fed's job this past year has thus been to keep the demand for money from collapsing, since that would result in even higher inflation, and they are doing that by raising interest rates. As the next chart shows, it's working.

Chart #5

The Fed has been driving monetary policy by looking in the rear-view mirror and ignoring the explosive growth in M2. That's why they were late to react to last year's inflation surge. They have since reacted forcefully by engineering an unprecedented surge in interest rates which has kept the demand for excess M2 from collapsing. Inflation pressures have fallen significantly, and the outlook for inflation is likely going to continue to improve, thus making further rate hikes unnecessary. If my analysis is correct, the mood of the market could improve substantially in coming months.

35 comments:

Hi,

Do you mind to comment on the Burry Tweet:

Inflation peaked. But it is not the last peak of this cycle," he said. "We are likely to see CPI lower, possibly negative in 2H 2023, and the US in recession by any definition."

He added: "Fed will cut and government will stimulate. And we will have another inflation spike. It's not hard."

I’m not sure I understand what he means by “stimulus” in this instance?

Thanks

I think Burry is predicting that the Fed will lower rates (which to his mind is “stimulative” but not necessarily so) and the government will also “stimulate” by spending even more money (which I firmly believe is never stimulative). He further assumes that the “stimulus” will somehow be monetized and that will create yet another round of inflation such as we have recently seen.

The problem as I see it is that deficit spending is not normally stimulative and it is most importantly not normally monetized. The 2020-2021 period is unique in monetary history: the entirety of deficit financed spending was done with printed money. Normally, deficit spending is funded by selling bonds, which absorbs money from the private sector and gives it to the government; no money is created in the process. This “stimulus” is not stimulus at all because a) it doesn’t create money and b) the government ends up spending the money less efficiently than if it were left in the hands of the private sector.

So he is making a lot of assumptions that I think are pretty speculative.

Wow, your smart Mr. Grannis. re: "the mood of the market could improve substantially"

There's upside left in wave 2 in the Elliott Wave theory.

https://danericselliottwaves.org/

If you add currency + demand deposits and then subtract that sum from M2, the percentage, drop in money demand, has reached low levels. It has dropped from .86 in 2008 to .66 in 2022. The most recent drop in 2022 was the greatest. Hence, R-gDp has risen.

Salmo you obviously say a lot of interesting and most of the time downright prescient stuff, but this Elliott Wave nonsense ain't it. Satanists and NWO and somehow vaccines tying it all together just screams of too much time in your mother's basement. You seem smarter than all of that and I think you should leave Generic Daneric alone in his kooky house with all the rest of the perpetual homeschoolers. Even my 5 year old can draw random lines between events that have already happened.

Technical point:

"All that extra cash was fine—as long as the public was willing to hold onto it. But when people emerged from their Covid cocoons in early 2021, they unleashed a tsunami of spending which overwhelmed supply chains and boosted prices for nearly everything."

And:

"That's just plain wrong; inflation is not a by-product of economic activity, it is the by-product of unwanted money."

In your first of those 2 comments, you say that it isn't the extra money, per se, that's the problem, since people sat on it for a while with no issues. It was only until they started spending it when it began creating inflation.

But in the 2nd of the two comments, you tell us that it is the "unwanted" money itself which created the problem.

Those are a bit contradictory: In the first one you say that the spending of the money created the problem. Spending money is an "economic activity." But in the 2nd you say that inflation is not a by-product of any "economic activity."

If people decided to just sit on that extra money in perpetuity, never doing anything with it at all, it would never have created any extra inflation. It was only when they did decide to do something with it en masse that it did create a problem.

Thus, it is not the extra money in and of itself which is the problem, it is what people do with that extra money. "Doing" something with money (namely, spending it) is an economic activity. Thus, it is indeed "economic activities" (in excess) which creates inflation, not the "extra/unwanted money" in and of itself.

Granted, as long as people have a lot of extra/unwanted money they are bound to spend it, which will create extra inflation, so it may seem like the extra/unwanted money created the problem, but that is not strictly true. The extra/unwanted money is merely the fuel; you need consumers to decide to actually light the fuel to create a fire. It is the act of lighting the fuel that creates the fire (inflation), not the fuel itself.

"New data from JPMorgan Asset Management published Monday shows estimated "excess savings" from U.S. households now stand at $900 billion, down from a peak of $2.1 trillion in early 2021 and roughly $1.9 trillion at the beginning of last year.

These savings have been drawn down as the personal savings rate has fallen sharply from historic highs seen during the pandemic.

The latest data on personal income and outlays from the BEA, released on December 23, showed the personal savings rate stood at 2.4% in November, down from a record high of 33.6% in March 2020."

re: "sit on that extra money in perpetuity". That's called secular stagnation, a deceleration in the velocity of circulation.

Bernanke’s “wealth effect” doesn’t work. Link: “Changes in Wealth and the Velocity of Money”.

Changes in Wealth and the Velocity of Money (stlouisfed.org)

The FED needs to ignore its "employment mandate." Plain and simple.

Of course, the Philips curve was denigrated in the 60's.

The FED also needs to get rid of interest on reserves:

https://fred.stlouisfed.org/series/RESPPLLOPNWW

Re the Phillips Curve: It boggles the mind that the Fed continues to view the economy through a Phillips Curve lens. It's a theory that originated in the 1800s and has never, ever, been confirmed by the facts. It is even counter-intuitive. As a great example, if high unemployment were necessary to bring inflation down, Argentina would have had zero inflation for the past several decades. Instead they have had a miserably weak economy and persistently high inflation (double digits). Inflation is so obviously a monetary phenomenon. Why can't the Fed with all of its PhD economists understand this?

John A: I think you are making a distinction without a difference here. Deciding to hold less money in the bank is not my idea of economic activity. It is a change in the demand for money, which can respond to all sorts of incentives. Inflation is the result of an excess of money relative to the demand for it. If the demand for money falls, then there is unwanted money which can drive inflation higher.

Scott: If one decides to hold less money in the bank, what exactly does that entail? Can one "hold less money in the bank" without "spending" it? Forgive me if I'm wrong, but there is spending, and there is saving. Right? Is there anything else I'm missing? Even paying off debt is spending, because it is debt from something one already bought (that is, spent on a car, a house, an investment, etc.). Thus, if you are holding less money in the bank - that is, reducing your savings - you've really no other choice but to "spend" it. And any spending is "economic activity." At least in my book it is.

John A: you need to think of it in collective terms. The public currently holds about $20 trillion in bank deposits, savings accounts and retail money market funds. One person can decide to reduce his cash holdings by buying something, but then the person on the other side of the transaction ends up with more cash. If everyone decides to spend down their cash holdings by a significant amount, the amount of money in the banking system doesn't change, but it's likely that a lot of prices have increased in the process (i.e., inflation occurs). Cash can disappear, however, if people decide to pay off loans, because that $20 trillion was created by banks that made loans to people; when you pay off a loan, the bank absorbs the cash and writes off an asset (thus reversing the initial loan transaction). As inflation increases, eventually incomes increase and nominal GDP increases. Thus the denominator in my money demand equation goes up while total cash (M2) stays the same or drops. In this manner the percent of total incomes (essentially equal to nominal GDP) held in cash falls. I

Scott: "If everyone decides to spend down their cash holdings by a significant amount, the amount of money in the banking system doesn't change, but it's likely that a lot of prices have increased in the process (i.e., inflation occurs)."

So, you're once again saying that it is the spending of some extra money that increases inflation, not the mere existence of the extra money itself. If I understood you correctly, in this case you actually gave me an example of where no extra money was created, but because people suddenly spent a lot more by drawing down their savings, inflation went up.

It seems as if you're agreeing with me without knowing that you're agreeing with me.

The saying should correctly be: "Inflation everywhere is a spending phenomenon." It may seem to be a "monetary" phenomenon only because episodes of excess money creation happen to lead to more spending, and thus, more inflation. But it isn't the excess money creation in and of itself which led to the extra inflation, it was the fact people decided to spend all that extra money, which created supply shortages of goods and the resulting inflation.

^The root cause is the money creation (think of Milton Friedman's helicopter money experiment).

But key modulating factors are the propensity and ability to consume (or spend).

That is the error in macro. Banks don't lend savings. Deposits are the result of lending. All bank-held savings are un-used and un-spent, lost to both investment and consumption. That is the single source of secular stagnation, the deceleration in Vt.

1961: Edwards: “It seems to be quite obvious that over time the “demand for money” cannot continue to shift to the left as people buildup their savings deposits; if it did, the time would come when there would be no demand for money at all”

The shift ended in 1981.

Banks aren't intermediaries between savers and borrowers. Banks always create NEW money whenever they lend/invest with the nonbank public.

https://fred.stlouisfed.org/data/PMSAVE.txt

Personal savings, U.S. Bureau of Economic Analysis

Release: Personal Income and Outlays fell from 2021-03-01 $5732.7 to 2022-11-01 $461.2

How much dis-savings is left?

https://fred.stlouisfed.org/series/PSAVERT

The Consumption of durable goods prices peaked at the same time long-term monetary flows peaked:

https://fredblog.stlouisfed.org/

What is really surprising (especially in hindsight) is how little inflation (and how transitory it's been from a larger historical perspective) was caused in spite of the massive and coordinated monetary and fiscal forced increase in savings.

Of course, in the aggregate, people have more money in their accounts (balanced by higher government debt) --- (note: unequal distribution; lower 50% no more) --- so one has to wonder if, everything else held constant, going forward effective demand will be lower.

That may be one aspect that Micheal Burry is considering as an input.

Hi @Salmo,

"The shift ended in 1981."

The advent of Yuppie? What is the significance of that year in your view? Thanks.

N-gNp went to 19.2% in the first quarter of 1981. That was because of the "time bomb" (which was predicted). I.e., the widespread introduction of ATS, NOW, and SuperNow accounts. All of the sudden you could write a check on your savings accounts.

This propelled Vt from 135 in 1980 to 177 in March 1981.

The "Great Inflation" was due to the monetization of time deposits.

The sharp rise in DD velocity (bank debits to deposit accounts) was the consequence of a variety of factors; the daily compounding of interest on savings accounts; the increasing use of electronics to transfer funds; the introduction of MMFs etc.

Then the DIDMCA impounded savings.

See: Was the 1982 velocity decline unusual by john Tatom, in Aug/Sept 1983 Review.

Interest is the price of credit. The price of money is the reciprocal of the price level. The "Fisher Effect" (“tendency for nominal interest rates to change to follow the inflation rate”) will be denigrated.

We also discussed whether and why a Phillips curve-centric model for forecasting inflation has returned to the forefront of policy making.

Evans: Policy makers can't have a forecast that’s "just sticking your finger up in the air and seeing where the wind’s blowing."

https://twitter.com/NickTimiraos/status/1612193623860281346?s=20&t=nAN4MmcLazkeGtMTgoQxUg

That’s a pretty lame explanation from Evans. But then most of the Fed’s discussion of the factors that affect inflation is lame. It’s amazing that they NEVER mention the money supply! Everything but. I’ve read so many articles and essays on inflation that are extensive reviews of everything going on in the economy, EXCEPT they never mention the money supply. Given the explosive growth in M2, and the subsequent explosion of inflation, it’s simply mind-boggling that no one even mentions the money supply.

I remember back in 1980-82 when financial market analysts held their breath before the weekly release of the M2 numbers—it was the most important event of the week. Why? Because Volcker’s objective revolved around restricting growth in the money supply through the use of higher interest rates. Nowadays, you will struggle to find a mention of M2, even though it is now only released on the fourth Tuesday of every month. A skeptic might argue that the Fed is trying to bury M2.

Thanks @Salmo for another good suggested read!

Question:

Would rising wages in such a lower inflationary environment increase M2?

^about rising wages

A big surprise in the December NFP report is the large revisions to wages for October and November 2022 which significantly changes the trend.

Real personal income excluding current transfer receipts continues to disappoint.

Wages don't create inflation. Typically, they respond to changes in the price level. Inflation is a monetary phenomenon.

My response to this post: Amen, amen, amen.

Concerning wages, as with interest rates, there is a real and a nominal component.

For interest rates, the Fisher equation is: nominal interest rates = real interest rates + inflation.

For wages, the equation is nominal wages = real wages + inflation

For wages, the inflation part follows general inflation trends (although there could be some push or pull components and even, under very specific circumstances, a tendency to self-perpetuate or entrench inflation trends).

Food for thought:

Historically (before 1975), there was a tight correlation between real wage growth and productivity growth which was relatively high. Since then, productivity growth has been slowing and real wage growth has decoupled even lower than the slower productivity growth.

There are many reasons for that but easy money and the ample reserves regime seem to be part of the problem (not the long term solution).

I think Burry comment above with what will happen on inflation has some legs, there will be second spike. It has precedent....the consumer is going nuts with credit....look at the fed numbers on consumer credit, especially revolving, a spike like no other...

DTI and PTI components of lending will increase denials....

From Atlanta Fed:

Business Inflation Expectations Unchanged at 3.0 Percent - January 2023

Inflation expectations: Firms' year-ahead inflation expectations remain relatively unchanged at 3.0 percent, on average.

https://www.atlantafed.org/research/inflationproject/bie

---30---

3%? That is only 1% above the Fed's target.

A little worrisome in the Atlanta Fed report is that businesses are reporting lower profit expectations.

I think the Fed can go slow. There is no crisis regarding inflation. It is annoying, yes, we all wish it was zero.

But 3% inflation is very livable, and people need jobs, and businesses need sales. If mild inflation is the cost of strong job markets and strong sales...then let's live with mild inflation.

Off-topic: The "Economic Problem"/"scarcity"- The hard work and productivity produces this:

https://acsjournals.onlinelibrary.wiley.com/doi/full/10.3322/caac.21763

"...the cancer death rate continued to decline from 2019 to 2020 (by 1.5%), contributing to a 33% overall reduction since 1991 and an estimated 3.8 million deaths averted."

https://acsjournals.onlinelibrary.wiley.com/cms/asset/3f0831ea-eb31-4d7a-b460-cb24264d63c5/caac21763-fig-0002-m.jpg

Note- this kind of data is indicative of a much "cleaner" environment in terms of cancer causing agents such as radiation and chemicals (trace levels)- contrary to what the average person probably thinks.

The US is the source of 80% of medical innovation. Get rid of the free market, and watch this progress grind to a halt.

@wkevinw

Not all you suggest is wrong.

Also, the US remains the undisputed leader in healthcare innovation.

But.

Cancer statistics is one of the few areas in healthcare outcomes where the US does slightly better (unadjusted) compared to other developed nations (only looking at health outcomes and without considering costs). When adjusted (ie for smoking levels), the relative advantage in cancer statistics is even less. Note that a lot of the decreasing mortality figures is related to lower smoking prevalence and... lower lung cancer prevalence etc. Other significant factors are better screening and marginally better treatments. A "cleaner" environment is not one of the contributing factors.

Example of supporting evidence for the above:

https://jamanetwork.com/journals/jama-health-forum/fullarticle/2792761

-----

Back to the productivity aspect related to this thread (inflation etc)

Healthcare in the US is a growing tapeworm on the underlying productive capacity. For example, in order to achieve marginally superior health outcomes in selected categories, the US spends about twice as much in healthcare dollars as the median developed country elsewhere.

There's got to be a more productive way to obtain better health outcomes. The idea is not to get rid of the private market but to get more out of it. My bet is that the US will eventually figure it out and one of the ways is to stop producing excess private savings (and cost of living crisis for the bottom 50-70%) arising from incremental public debt, cheaply financed.

Post a Comment