Chart #1

As Chart #1 shows, there's a pretty close relationship between truck tonnage and equity prices. Today there is a sizable difference between the two, with truck tonnage suggesting the economy is virtually booming, whereas the equity market has been dominated by caution for the past year or so. Estimates by the Atlanta and NY Fed put real GDP growth in the current quarter at a miserable 1- 1.5%. As happened a few months ago (see Chart #11 in this post) the stock market may still be overly cautious about growth. Recall that Q1/19 growth came in substantially higher than expectations.

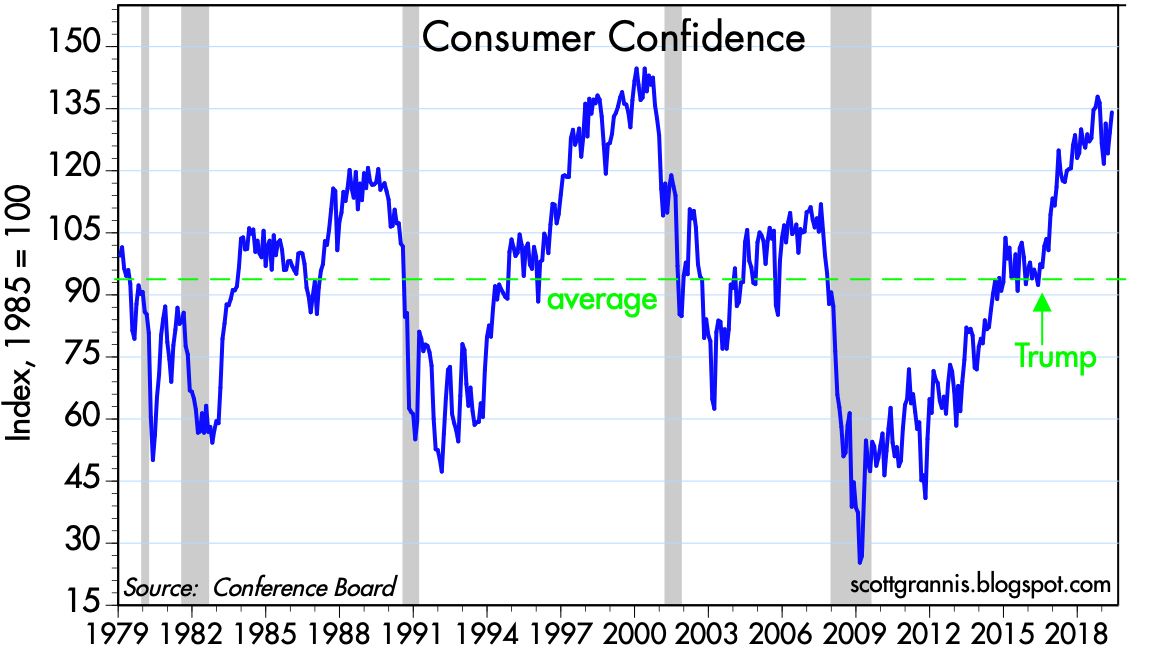

Chart #2

Chart #3

Charts #2 and #3 show the two major measures of consumer confidence (Conference Board and University of Michigan). Both have surged in the wake of Trump's election, and despite setbacks in late 2018 and early 2019, have rebounded of late. I won't try to minimize all the negatives that are out there (e.g., flat housing starts, flat car sales, tariff wars, very low bond yields, and expectations that the Fed will need to cut rates 2-3 more times to bail out a struggling economy). I'm just suggesting that things might not be as bad as the market thinks.

19 comments:

Keep On Truckin'!

I once read that the FTSE 100 has become so globalized it no longer reflects the real economy of Great Britian.

I wonder if there is a measure of truth in this as it pertains to the S&P 500 or the NASDAQ. Those two indexes seem very sensitive to what are, after all, minor fidgets in international trade as promulgated by the Trump Administration. The math for a 25% tariff on some Chinese goods bringing down the US economy just isn't there.

But an Apple, a BlackRock, a Walmart, an Amazon, a GM might get their tits caught in a wringer.

My hope is that the bad news is out on Trump tariffs and we can go forward from here. I think the tariffs will last the life of the Trump Administration and it may not be so bad if they become permanent.

Wow. That is quite a spike in tonnage.

I just tried to rent a van and found the inventory very tight.

I have seen suggestions that some of the change in truck tonnage is related to the completion of recent improvements in the Panama canal, meaning one now ships to the east coast rather than the west coast and uses trucks rather than railroads to move cargo to destinations.

I must be living in some parallel universe or something...

Today, Richard Clarida said these words: "If the incoming data were to show a persistent shortfall in inflation below our 2% objective..., then the FOMC would take into account the appropriate stance for monetary policy."

You can't make this stuff up. Not only has core PCE shown a persistent shortfall to 2%, but today - this very day! - the core PCE was revised downward from 1.5% to 1.0%. Honestly, it's often said how clued out these Fed mandarins are but this is staggering even for them. And Clarida isn't nearly the most hawkish. Where have they been? Do they pay attention to anything? On what basis are they NOT lowering rates?

Question to all the Fed governors: How do you explain the breakevens? I ask because this is a market-based metric for future inflation. Do you people really think you know more than the market?

I suspect the Fed is listening to Friedman in that changes in monetary policy result in long and variable lags. I think it's tough to get it right ex-ante, especially post financial crisis, long term trends in lower interest rates, globalization, the recent Fed policy innovations...

BTW. Scott has done an outstanding job helping clarify the mechanics of some of those FED innovations ie; Q easing, "transmogrifying notes, bonds, bank reserves," etc. The FED matching the money supply to offset the public's demand for holding dollars...

Well, Trump will do what he can to make things worse.

But, but, he did the tax cuts! He understands the economy!

The thing about these sort of populists with "strong ideas" is that

people support them for specific "strong" actions and ignore all the warning signs.

People cheer when these "strong" actions go into effect.

But, people like Trump don't stop. They can't, that's who they are. So they continue blasting everything in the same way, with tough measures. Those tax cuts that you thought it means he knows what he is talking about? Just a coincidence. He doesn't have a fucking clue.

People like Trump then go for the institutions trying to take them down.

If they succeed, they take over the country.

Happened quite a few times in history. Sadly, it's not hypothetical.

One can only hope the US will prevail, that people will wake up.

The bond market is FORCING the Fed to cut rates and damn soon.

The market is sending the Fed a strong message today: a rate cut is in order, if only in response to the degree of fear and uncertainty surrounding Trump's trade wars (which have expanded now to include Mexico). Trade/tariff wars reduce future economic growth expectations and create uncertainty. Both of those act to increase the demand for money. The Fed needs to lower short-term rates in response, in order to prevent an imbalance between the supply of and the demand for money. Commodity prices are relatively weak, and the dollar is relatively strong, and the combination is pushing inflation and inflation expectations down. Inflation expectations are now down to 1.6%, and real yields on TIPS have fallen significantly last December. A cut to 2.0% would seem warranted at this juncture.

Love the comment, Scott.

Btw, I jumbled my numbers in my last comment. Sorry for that. But the wider point holds, that we in fact have seen persistently sub-2% core PCE.

And I would like to see the aggressive question put to the Fed governors: What do you think the breakevens are telling us? Silence should no longer be accepted.

Grechster: I can't get very worked up over the fact that inflation expectations are 1.6% despite the fact that the Fed has been targeting 2.0%. I just don't see monetary policy being a tool that permits what are effetively microscopic adjustments to the inflation rate. Getting 1.6% when you're targeting 2.0% is plenty good enough for government work, in other words. In any event, I would always prefer 1.6% to 2.0%. Lower inflation is always better. In an ideal world I would like to see the Fed target zero inflation. Besides, as my Chart #2 in today's post shows, big swings in oil prices appear to result in similar swings in inflation expectations. Not everything is under the Fed's control, and the Fed shouldn't ever try to stabilize oil prices.

Truck tonnage can be deceptive and it appears to be now.

I believe railroad intermodal unit data are a better number, and they are telling a different story.

Intermodal units will become truck tonnage, so they are a slightly leading indicator.

( I do not rely on total railroad volume, because there can be large variations in how oil is transported -- by pipeline or railcar -- so the intermodal volume, that I have tracked for longer than I can remember, is the number to watch )

.

.

.

Here are excerpts from the latest May 29 weekly release, for the week ending May 25, 2019:

" ... U.S. weekly intermodal volume was 268,013 containers and trailers, down 8.3 percent compared to 2018."

" For the first 21 weeks of 2019, U.S. railroads reported ... 5,607,120 intermodal units, down 2.2 percent from last year. "

.

.

.

The first 21 weeks of 2019 are obviously much more important than the single week ending May 25, but that single week does not show a reversal of the 21 week down trend.

Data source ( always see first link for the latest data ), that I recommend you bookmark:

https://www.aar.org/aar_news/weekly-rail-traffic-data/:

Scott,

Is truck tonnage a leading, lagging, or coincidental economic indicator?

Bob Wright

Truck tonnage is close to being a coincident indicator, since it comes out with a modest lag of a few weeks.

Post a Comment