The chart above compares top tax rates to tax revenues as a % of GDP. (Comparing taxes collected to the size of the economy is the only meaningful measure of revenues.) Note that despite the huge reduction in tax rates in the early years of the Reagan administration (early 80s), revenues hardly fell at all, and in fact increased at a fairly impressive rate through the late 80s and 90s.

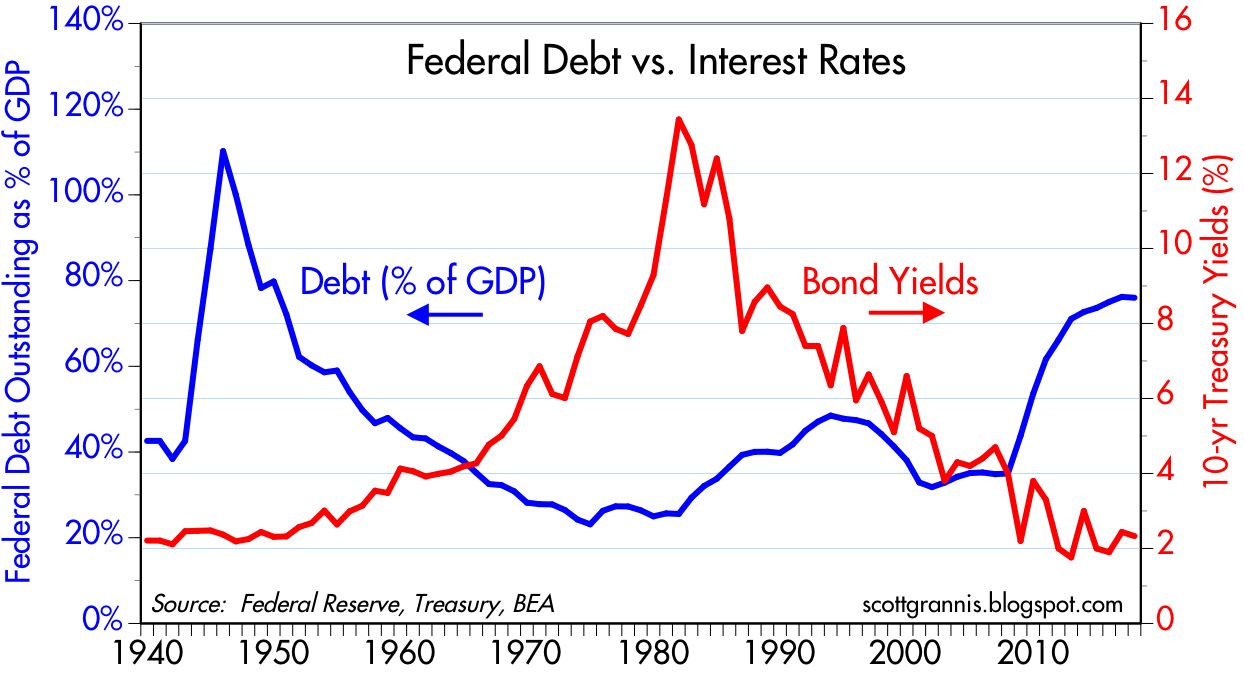

There is not a shred of evidence to suggest that rising federal budget deficits have any impact significant impact on interest rates. In the chart above we see that huge increases in the budget deficit have occurred alongside very low interest rates. Predicting higher interest rates as a result of rising deficits is not supported by the experience of the past.

As the chart above shows, recessions almost always result in very weak tax collections. No surprise: recessions cause incomes and employment to fall; the tax base shrinks and revenues decline. Periods of economic growth almost always cause revenues to rise.

Federal spending almost always rises as a result of recessions. Politicians can't resist spending extra money to "stimulate" the economy, and automatic stabilizers like food stamps and unemployment insurance kick in. The most important influence on revenues and spending is the health of the economy.

The Reagan tax cuts did little if anything to worsen the deficit, which began rising in the wake of the recessions of '81 and '82. The current deficit, relative to GDP, is well within the range of post-war experience.

The chart above makes it clear that people respond to incentives, especially when it comes to taxes. Prior to the increase in capital gains taxes in late 1986, capital gains realizations surged. They then fell dramatically, coming in at about half what the CBO had projected prior to the hike in the capital gains tax rate. Note also that declining capital gains tax rates in the late 90s saw a big increase in capgain revenues—exactly the opposite of what an accountant would have projected. The capital gains tax is the only tax you can legally avoid, by the way. All it takes is not selling something you hold at a gain. If we reduced capital gains taxes tomorrow I would bet a lot of money that federal revenues would rise. I for one would sell a lot of things that I have avoided selling. I would also diversify my portfolio in the process, and I would be much more willing (and able) to invest in new things. As it is, a lot of my money is tied up in gains that pain me to realize. It's the same story for corporations who refuse to repatriate their profits. It's therefore hard to overestimate the potential impact of true tax reform.

The chart above shows that federal spending and revenues today are very much in line with historical experience. The weakness in revenues of late could very well be driven by the anticipation of lower tax rates. Taxpayers have lots of ways to postpone or defer income, just as they can postpone or defer capital gains—if they think there is a chance that tax rates will fall in the future. Corporations can postpone or defer new investment as well. Thus, it's not wise to promise tax cuts in the future and then delay their implementation. That was the mistake that Reagan made with his first round of tax cuts; revenues promptly declined because people were waiting for the second round of cuts.

Meanwhile, there is still little if any evidence to suggest that the market has priced in any meaningful increase in the economy's health. People may be postponing income in anticipation of lower tax rates, but nobody's betting that the economy is going to pull out of its 2% annual GDP growth rut anytime soon.

The chart above compares the real yield on 5-yr TIPS to the real Fed funds rate. It's best to think of the red line as being the market's forecast for the average level of the blue line over the next 5 years. Right now the market is not expecting the Fed to do much more in terms of raising the real rate of short-term interest rates in coming years. That expectation, in turn, is very likely driven by the belief that the economy is going to be stuck in its 2% growth rut for as far as the eye can see.

The chart above confirms that from another angle. Here we see that real yields tend to match the economy's growth rate trend. The current level of real yields is consistent with economic growth of about 2%. If the market were more enthusiastic about the economy, TIP yields would be much higher.

The gold market agrees. The prices of gold and TIPS have been strongly correlated over the years. My interpretation of this is that people are more inclined to buy gold when the economy is weak, and less inclined when it is strong. If the market really believed the economy were about to break out of its 2% growth rut, real yields would be a lot higher and gold prices a lot lower. Why hold gold if the economy is improving? Better opportunities can be found when the economy is healthy and chugging along. Gold and TIPS have been meandering around the same levels of several years, all the while the economy has been stuck in a 2% growth rut.

23 comments:

Well great post, and certainly federal deficits and rising federal debt to GDP ratios have not seem to have hampered real growth since 1980. James "Doomsday Is Pending" Grant is perplexed (to put it extremely mildly). Many have predicted more federal debt would ruin America. Well, here it is, lots of it, and piling up.

See especially Chart 2 (I will hector Scott Grannis again to number his charts), which does show sharply rising debt to GDP levels since 1980. So we are in a 40-year run of rising indebtedness, and no end in sight. Worse, I suspect the political will to reverse this trend does not exist in our two parties. A salve may be that interest rates could stay low for another generation or two.

Will the Trump tax cuts make this worse or better? Indeed, to be honest, why do federal debt to GDP levels start rising coincident to the Reagan tax cuts (which I liked)? The numbers-crunchers say the Trump cuts will add another couple trillion to the federal debt pool, which is nearly $20 trillion. Will that matter? The global debt pool is $200 trillion. It is hard to imagine federal debts can raise global interest rates, which are set globally.

The old GOP'ers of the post-WWII era (Everett Dirksen, Eisenhower) were very conservative about paying down debt to GDP levels. We also had explosive GDP growth through the 1950s and 1960s when the federal debt to GDP level was falling, not rising. Maybe James Grant is onto something?

Well, let us hope there is an escape hatch somewhere out there, from these seemingly locked-in rising levels of federal debt. Maybe it is QE, or maybe helicopter drops, or maybe another Clinton Administration, that thought unless it balanced the budget, the bond market would go nuts.

Are we the next Greece or Puerto Rico? Or Japan? Argentina? Give it another 20 years, and we will find out.

I am beginning to sound like James Grant, no?

Scott,

Again a most helpful article.

Thank you for all the writing and easy explanations& charts your provide.

Chart 1 shows the largest marginal tax rate cut, by far, was in the Reagan years.

Chart 2 shows a large rise in the federal debt as a percentage of GDP in the Reagan years.

Gross Federal Debt tripled in the Reagan years, from $900 billion to $2.7 trillion.

Ford and Carter in their combined terms could only double it.

It took 31 years to accomplish the first postwar debt tripling,

yet Reagan did it in eight years.

Cliff: the only meaningful measure of federal debt is the ratio of debt held by the public to nominal GDP. That is the true burden of the debt. By that measure, Reagan increased the nation's debt burden by 14 percentage points, to about 40% of nominal GDP. Obama raised our debt burden by 28 percentage points, to 76% of nominal GDP. The increase in the nation's debt burden under Obama was about equal to the debt burden accumulated by all presidents prior to Nixon.

I would only add that the major culprit of the Reagan deficits was spending, not tax cuts.

The first chart is extremely misleading because of the small population that actually pay the top tax rate. This is akin to claiming everyone can run the marathon in around 2 hours because Olympic distance runners can do this.

Furthermore, the small population that do pay the top tax are the wealthiest Americans. Lowering the top tax rate will benefit them and no the majority that aren't not so wealthy.

Perhaps this is a more honest and transparent point that is supported by your chart?

Give a huge tax brake only to a small population of the wealthiest Americans will not lower the overall tax revenue.

At the end of the day, what is your goal? If you want to preach to the choir, what would you have really accomplished when you reflect on your death bed?

However, if you want to bring all Americans together, trying to fool them will only widen the chasm.

Re the top 1%. Those who pay the top tax rate are wealthy, no argument there. But they are also the ones who can make the biggest difference if allowed to keep more of what they earn. Regardless, it is almost always the case that when the top rate is lowered significantly, so are all the other rates—so this chart is a valid representation of important changes in tax rates that can have huge incentive effects throughout the economy.

When top margin rates exceed 25-30%, as they do today, I think that is not on criminal, but foolish. Those who make a lot of money can do all sorts of things to avoid paying taxes. It would be much better if they were given an incentive to invest, take risk, create jobs and make even more money. When the government confiscates money from the wealthy we all suffer. Cutting punitive tax rates is not giving the rich a break, it's reducing the penalty to being rich. Everyone, no matter how much they make, should have the right to keep most of what he makes. To think otherwise is to be petty, greedy, envious, and foolish.

The rich always spend their money better than politicians. Government wastes the money it confiscates from the rich. The rich invest the money they can keep, and that's what creates jobs and prosperity.

WELL SAID, Scott Grannis!!

Scott, I tend to agree very closely with most of what you write regarding the direction of the economy and current conditions. However, I don't find your first chart convincing. Cutting the top rate that nobody paid, to a rate that perhaps more were willing to pay, while eliminating loopholes, seems a long way from demonstrating that reductions in the top individual rate drive increased compliance so as to maintain overall tax revenues. CBO studies I looked into years ago indicate that cutting corporate rates creates jobs, cutting capital gains rates appears to create some jobs but the data is not definitive, and that cutting individual rates has zero impact on job creation.

As for Reagan vs Obama... well, I voted for both, and consider them both good but flawed Presidents. Putting that aside, I don't think either of them had any idea who was going to buy the debt issued by the Treasury to fund their respective deficit spending. The economy during Obama's Presidency also endured 3x the job losses (clearly inherited, as were the Reagan and Bush 1 recessions), on top of automation and globalization inhibiting the recovery, so I find most comparisons are far from apples to apples.

The Trump tax reforms don't seem likely to happen. The elimination of the deduction for state taxes is a huge monkey wrench, but also Trump hasn't shown much leadership ability. I'm a fan of tax reform, but I'm not enthusiastic about this approach.

Well said. Thanks for the easy explanation of the article.

Jobs

Job

Reagan tripled the national debt

Obama doubled the national debt.

The true burden of the debt is not the % of GDP,

it is the annual interest payments.

Since there is almost no chance that any of the debt will be paid back

(rolled over, yes paid back, no), there is no sense to growing the debt so fast

BEFORE the huge burden of financing senior citizen "welfare" for the baby boomers

(Medicare, Social Security, Medicaid and Govt. employee pensions).

The interest rates on government debt may be unusually low now,

but will they always be low?

The debt will always be there, and is likely to grow fast

as baby boomers retire and start getting Social Security

and Medicare -- both are actually pay as you go welfare programs --

so the risk of rising interest rates on that debt will remain.

If a large expansion of debt results in good economic growth,

as under Reagan, at least there was some payback.

The large increase of debt under Obama

was accompanied by unusually slow growth = what payback?

Also:

There have been some myths here and elsewhere

about US corporate taxes being the highest in the world:

That is not correct.

That claim completely ignores value-added taxes in every other major nation !

Also, actual corporate taxes paid by U.S. companies

have only been lower during the last recession

(measured as a percentage of pre-tax profits).

In addition, corporate profit margins are much higher than average now.

Corporate stock prices are at or near record valuations by many measures, now.

With all the good news on the corporate tax rates ACTUALLY PAID,

high corporate profit margins,

high corporate stock valuations,

and high corporate executive pay,

there is no economic justification

for making corporations even more profitable

by slashing the corporate tax rate now ...

... unless your goal is to be demonized by Democrats,

lose the Republican majority in the Senate in 2018, and

and lose the Republican Presidency in 2020.

I'm sorry I have a really hard time taking your column seriously today. During the Obama years you were Deficits are bad, deficits ar bad. Now that its Republicans in charge deficits are ok!

What you mean is deficits are OK as long as I get my tax cuts...I get that

Hypocrite!

One point I'm making here is that lowering tax rates is not necessarily bad. I'm not arguing at all that deficits are good. But I would add that deficits that result from a reduction in tax rates can end up being a good thing, if the lower taxes boost investment and productivity. The Obama deficit was driven primarily by government spending, and I have always argued that increased government spending does not and cannot be good for the economy. I resent being called a hypocrite, by the way, since I take pains to be consistent in my arguments.

The entire deficit and growth argument seems like a red herring to me. In reality, the Triffin dilemma explains all that is needed at the moment. The Triffin dilemma is the conflict of economic interests that arises between short-term domestic and long-term international objectives for countries whose currencies serve as global reserve currencies. Basically, the deficit and debt have to continue to grow in order to provide enough liquidity in the worldwide dollar market to retain reserve currency status and the privileges that provides to the superpower with that status. Without the increase in deficits and debt loads, the reserve currency status would be in danger due to a dollar shortage. So, why all the bickering back and forth between the left and right regarding this simple dilemma? Seems like a simple red herring to me.

Also, the US GDP equation is GDP = C + G+ I + NX, with G representing governmental spending. Factoring in increased deficit spending, the G component of GDP can be materially altered by the government undertaking of increased overall debt.

Scott – I am curious what your thoughts are on the Triffin Dilemma and the lack of discussion on this topic in any mainstream economic publication

As an experimental scientist, I'm going to be cautious about data that is affected by so many input variables. But, ignoring that caution for the moment...

Chart 1 tells me, as Scott says, that income tax revenue is fairly insensitive to top marginal tax rate. (Given this info only, I'd argue that lower is better.)

Chart 2 tells me that debt can be reduced over an extended period of time (post-WWII through 70s) while marginal tax rates are, by today's standards, extraordinarily high.

I've seen other charts, from more liberal sources, that show that the overall tax burden (not just income tax) has been shifting steadily for a while from the very wealthy to lower strata of wealth. Is this true? Of course, one could argue that the lower strata of wealth obtain more services from the government (SS, etc.). I always struggle with this argument because it is simply impossible to quantify how much benefit someone like Bill Gates or the Walton family obtains from government spending. But, ignoring this "fairness" argument, is it beneficial (to GDP, to median household wealth, to whatever measure you like) for the tax burden to be shifted this way? I'm a pretty clever guy but not in the highest wealth strata, maybe almost in the 5% from a family that was perhaps in the 30%. What is the argument that untaxed wealth is more productive when it is in the hands of someone in the highest wealth strata rather than mine? (Hey, I might agree for some individuals you could name! But for your average very wealthy person?)

This is from a fellow named Lars Christensen, and I think maybe right.

"Contrary to the perception of many policymakers and commentators, we use an econometric study of 10-year bonds in 21 countries since 2000 to show that yields have not been driven lower by lax monetary policy.

Instead, the decline has been driven by three factors: low inflation expectations, ageing populations and tighter financial regulation (Basel III).

As for monetary policy, it has not been too easy. The problem is just the opposite: monetary policy has been too tight and inflation expectations have fallen in consequence. This has put downward pressure on rates and yields over the past decade.

In this edition of the Monitor, our econometric study is also used to analyze the impact of recent and forecast demographic trends on global bonds. This analysis shows that demographic factors will also weigh on global bonds yields, skewing the risk decidedly to the downside.

Structural changes on the bond markets have also caused an increase in money demand across countries. This has significant implications for the conduct of monetary policy. Most important, central banks around the world – and especially the Federal Reserve – should re-think whether they can and should ‘normalise’ their key policy rates and balance sheets."

---30---

Trump can just about re-make the FOMC next year. I hope he errs on the side of growth-mongers.

The GOP is caving on the deductability of state tax. Without that exclusion there is no tax bill. You guys are deluded if you think anything close to this will pass. The GOP can't agree on a damn thing and you think something significant will pass? Get real. IF anything passes-and I have serious doubts-perhaps a reduction in corporate rates and an increase in exemptions. Big freakin deal. No game changer. The dems are playing cat and mouse until next years election and will continue to be obstructionist.

Steve

The Dems are not playing a cat and mouse game...nobody is talking to them!

The GOP wants to control all aspects of the legislation, there are no Dems on any meetings -- their input is unwanted.

The Kennedy and Reagan tax rate cuts did wonders for economic growth but focusing on the chart that presents tax revenues as a percent of GDP hides the fact that growth did occur.

Tom: good point

I wish canada would lower taxes like US is trying to do. We increased the top tax rate to 53% when we voted in a majority liberal government. And now they are going to bring thr hammer down on small incorporated businesses.

So frustrating.

Lower the taxes. It's healthy for everything.

I would love to see this come though.

Re the GDP equation (GDP = C + G + I + NX). The equation makes sense, but only up to a point. Increase government spending is politician's favorite way of "stimulating" the economy, but it doesn't necessarily work. The key here is to realize that government can't spend more without taking resources from the private sector, which then has fewer resources. There is no free lunch. When government commandeers funds from the private sector, the net result could well be a smaller, weaker economy. Because government doesn't always spend money as efficiently and as productively as the people who earn the money.

So additional government debt is not necessarily a good thing. But taking on a reasonable amount of debt is not necessarily a bad thing either. What's important are the incentives that are in place. If tax rates are cut in a meaningful way, then an increased deficit is likely to be overshadowed by a stronger economy, because reduced tax rates create a bigger incentive to take risk and work and invest.

And of course, a deficit in our trade accounts needn't be a problem at all (contrary to what Trump thinks), because a trade deficit is always balanced by a surplus in the capital account. Capital inflows help fuel investment, and that strengthens the economy.

aadhar.download

check aadhar status

Post a Comment