The Chemical Activity Barometer rose 5.2% in the past 12 months, one of its strongest showings in seven years (the strongest being the year ended March, when it rose 5.6%).

This indicator almost always goes flat or declines in advance of recessions. Currently it points strongly to continued expansion.

This indicator has been a good leading indicator of growth in industrial production and economic activity in general. Currently it points to a substantial increase in industrial production in coming months.

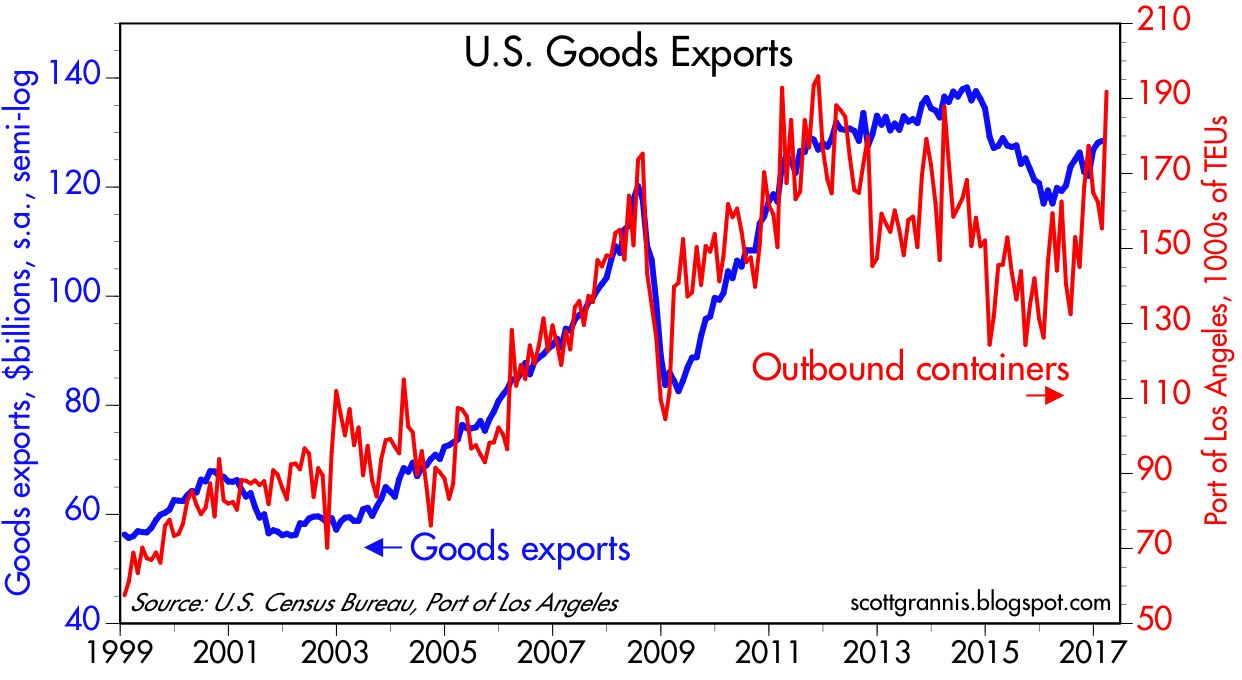

As the chart above shows, US goods exports have been rising for the past year, and that is corroborated by a sharp increase in outbound container shipments from the ports of Los Angeles. It's notable that US exports to China rose over 20% in the year ending February, after contracting over most of the 2014-16 period. Japan reports double-digit growth in both imports and exports in the year ending March, after declining over most of the 2015-16 period. According to the Netherlands Bureau for Economic Policy Analysis, the volume of global trade rose at an 8% annualized pace in the six months ended January 2017. Expanding global trade is an excellent indicator of improving economic conditions worldwide. Very encouraging.

Rising prices for industrial commodities over the past year or so—at a time when the dollar has been rising—tell us that global industrial activity has generally exceeded the expectations of commodity producers. Also very encouraging.

Yet despite the good global news, the US economy seems still to mired in mediocrity (i.e., 2% growth). That's not necessarily inconsistent with global strengthening, since trade is much less important to the US economy than it is to most other economies. But improving global fundamentals nevertheless provide strong underlying support for activity here.

It's premature to worry about a US downturn, and it's not unreasonable to remain optimistic that things will improve. It pained me today to learn that Trump wants to impose a 20% tariff on imports of Canadian softwood, since all that does is make life more expensive for US residents (UPDATE: Read Mark Perry's excellent critique of Trump's tariff here). But I'm encouraged that he seems pointed in a positive direction in the area of tax reform, and that there is important progress being made on healthcare reform.

8 comments:

I wonder how how the U.S natural-gas boom is playing into chemical production?

Happy I am for the good news; just wondering if the chemical industry is faring well for a while, as U.S. prices for natural gas are lower than global prices.

Dow Chemical wants to keep US gas cheap and at home. Obviously, producers would like to export natural gas.

If US natural-gas prices migrate to global levels, can we expect some chemical production to shift offshore?

For his entire life Trump has been a terrific self promoter. Bombastic over promiser and under deliverer. If the GOP can't get together on tax reform-as they failed on health care, we'll be LUCKY to match economic growth under O's term. So much for "animal spirits".

Trump's proposed 20% tariff on lumber from Canada is shocking if for no other reason than it will increase the cost of lumber in the US at a time when new construction is still trying to get some wind in its sails. On a different subject, I am having trouble digesting the chasm between stocks and bonds. I remain frightened by the markets.

https://www.bloomberg.com/news/articles/2017-04-25/-extreme-treasury-stock-schism-vexes-markets-amid-risk-rally

The chemical index is narrow coverage of the whole economy, and bullish.

Industrial production is broad coverage of the whole economy, and bearish.

One of these indicators is wrong.

It would be a bullish bias to focus on on the bullish narrow indicator, and ignore the bearish broad indicator.

Yet, that's exactly what this article did.

It's probably impossible to predict a recession if one looks for good news, and ignores bad news.

That's confirmation bias.

Cliff: you have missed the fact that the chemical index is a leading indicator of industrial production.

Scott Grannis: Do you suppose it is lumber prices, or tight, stipulative anti-competitive, anti-free market state and local property zoning that causes housing prices to be so high along the California coast?

Lumber prices are a factor in housing prices, of course, but zoning restrictions are almost certainly a bigger factor.

The chemical index has not been a leading indicator in the past two years.

Perhaps before that it was.

Post a Comment