Gold needs lots of fear and trembling to move higher. Note that gold prices peaked in the latter half of 2011, right around the time that the PIIGS crisis peaked (second chart, which shows the yield on 2-yr government bonds). Several countries, larger and more important than Greece, were flirting with default in late 2011, and the world feared the collapse of the entire Eurozone. At the same time that gold prices peaked, government yields and 2-yr swap spreads were on the moon. Today, 2-yr Portugal yields are a mere 80 bps, while 2-yr Spanish yields are 42 bps; 2-yr Eurozone swap spreads are only 40 bps. Yields and swap spreads are way down, and gold prices are way down; it's all part of the same story—less panic, a bit more confidence, and liquid, functioning financial markets.

Gold is falling because Greece is not a major threat and there is little or no evidence of any systemic risk. As the first chart above suggests, gold is also falling because the demand for safe assets (e.g., gold and 5-yr TIPS) is falling. (Note that I've used the inverse of the real yield on TIPS as a proxy for their price.) The world is still quite risk averse, as I noted yesterday, and gold is still trading at elevated prices: over the last century, the real price of gold has averaged about $550/oz. But things are slowly getting less risky, and investors are slowly becoming a bit less risk averse.

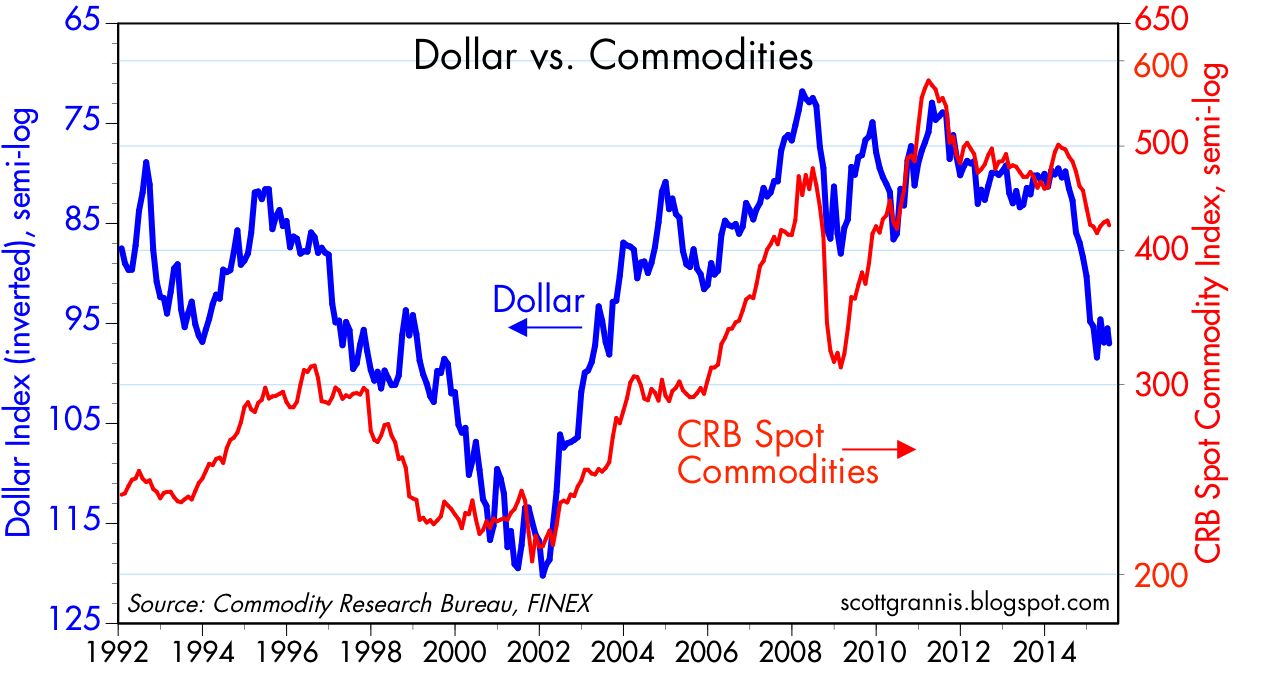

Gold is also falling because commodity prices are falling. Both are falling because on the margin the dollar has been strengthening. Gold and commodities are both a refuge of sorts when the dollar is weak and there are fears that monetary policies will lead to higher inflation. Markets are somewhat less concerned about that now, as inflation has remained quite low throughout the developed world even as central banks have been very accommodative.

Greece is bad for gold because Greece is not a compelling reason to pay up for the safety of gold.

Unless things take a big and unexpected turn for the worse, equity investors will find it hard to justify hiding out in cash, especially when cash pays nothing and yields on alternative assets (see chart below) are much higher, systemic risk is very low, monetary policy is accommodative, and there is no sign of any significant weakening in the economic outlook.

4 comments:

The bulk of gold demand today originates in India and China where it is used for jewellery and as a type of investment. The nation of India has been trying to monitor and tax gold which previously it has not.

It may be in the long run gold again appreciates; tthere are three billion people in India and China and living standards are rising.

The connection between western central banks and gold prices is curious. When the Fed printed up $4 trillion in QE, gold prices cracked.

I wonder if anyone anywhere has a good track on predicting gold prices.

OECD Composite leading indicators

"Composite leading indicators (CLIs), designed to anticipate turning points in economic activity relative to trend, continue to point to growth convergence across most major economies and within the OECD. { Meaning they are all approaching stagnation! }

The CLIs continue to point to firming growth in the Euro area, including France and Italy, and to stable growth momentum in Germany, Japan and India.

On the other hand, the CLIs point to easing growth in the United States, Canada, China as well as the United Kingdom, albeit from relatively high levels.

The CLI for Russia shows tentative signs of a positive change in growth momentum while in Brazil the CLI continues to point to a loss in growth momentum."

Downloadable .pdf with charts here: http://www.oecd.org/std/leading-indicators/CLI-July15.pdf

No need to worry about the stock market, China shows us what the government can do.

Have the central bank print money to make loans to brokerage firms to use for margin lending.

Cut interest rates.

Reduce bank reserve requirements.

Suspend IPOs (in order to reduce the number of shares available for trading to help keep supply short of demand).

Let companies voluntarily suspend trading in their stocks on the exchanges if their stock is declining.

Expand collateral for margin loans to include equity in homes on top of existing art work and antiques.

Have the central bank print money for a reserve fund to buy stocks (ETFs and mutual funds) directly.

Keep the housing boom going as a way to support stocks buy having the central bank print money to buy the debt of local governments which debt was used for real estate financing.

Ban pension funds from selling stocks in their portfolio.

Ban any large holder from selling stocks.

And they can put a time limit of say a year.

Finally, they can stock trading by creating a computer glitch.

YoBit lets you to claim FREE CRYPTO-COINS from over 100 unique crypto-currencies, you complete a captcha one time and claim as much as coins you want from the available offers.

After you make about 20-30 claims, you complete the captcha and keep claiming.

You can click CLAIM as many times as 30 times per one captcha.

The coins will stored in your account, and you can exchange them to Bitcoins or Dollars.

Post a Comment