The August ISM manufacturing report beat expectations (55.7 vs. 54), and was generally strong. As the chart above suggests, this is consistent with an acceleration of economic growth in the current quarter relative to the second quarter's 2.5% growth, possibly to something in the range of 3-4%. This is quite encouraging, even if it means that the recovery is still only modest and sub-par.

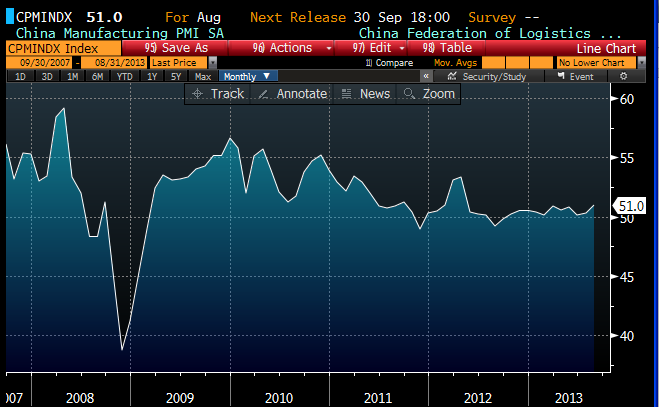

Export orders were relatively strong (top chart), and this suggests that conditions overseas are improving. As the second chart above shows, conditions in the Eurozone are indeed improving. As the third chart shows, manufacturing conditions in China also have improved, albeit only marginally. Nevertheless, this is a positive, since the world has feared that conditions in China are deteriorating. China's economy is probably growing at a 7% rate; although that is only modest by Chinese standards, it is still more than twice the growth rate of developed economies. A growing China is supportive of global growth in general.

The prices paid component of the ISM report shows neither inflation nor deflation concerns.

The employment sub-index was marginally positive, and still reflects a business climate that is lacking in confidence. Although business conditions are improving, things could be a whole lot better.

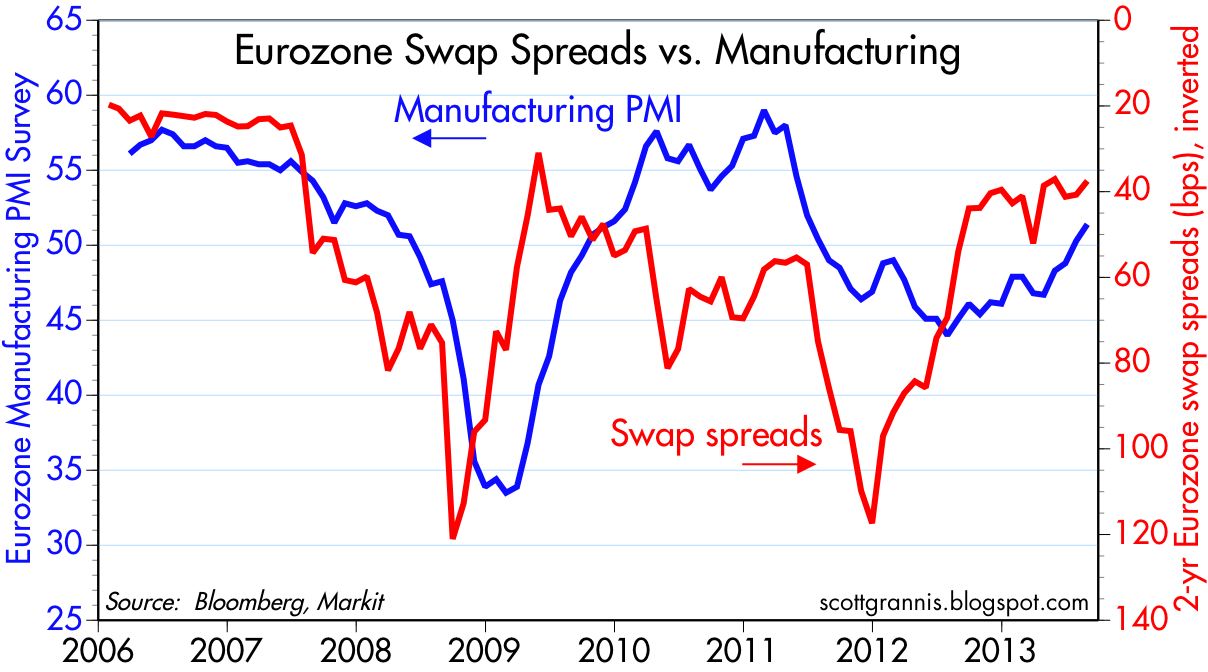

As I've noted dozens of times in the past several years, swap spreads are good leading indicators of economic health; a healthy financial system is, after all, a necessary condition for a healthy economy. As the above chart shows, Eurozone swap spreads have indeed been excellent leading indicators of Eurozone manufacturing activity. Swap spreads are still somewhat elevated in the Eurozone, but they are declining on the margin, suggesting that manufacturing activity is likely to continue to improve.

Finally, the new orders sub-index was quite strong in August, and that augurs well for manufacturing activity in the coming months.

It is ironic—but symptomatic of a market that is still lacking in optimism—that risk assets should be struggling of late despite the relatively widespread improvement in the global growth outlook. The logic driving the market these days seems to be that better-than-expected news means higher-than-expected interest rates, and that in turn means that growth will be worse than expected in the future. I don't buy it (I think higher interest rates in today's environment imply stronger growth in the future), but that seems to be the current mood of the market: good news is somehow bad news.

1 comment:

And don't forget, Japan is showing signs of life under an aggressive pro-growth monetary regime...

China and Japan together now have a larger GDP than the USA and consume far more resources, such as steel, copper, aluminum, etc, everything except oil....

Still, growth likely sluggish in the USA due to our central bank tight money policies....

Post a Comment