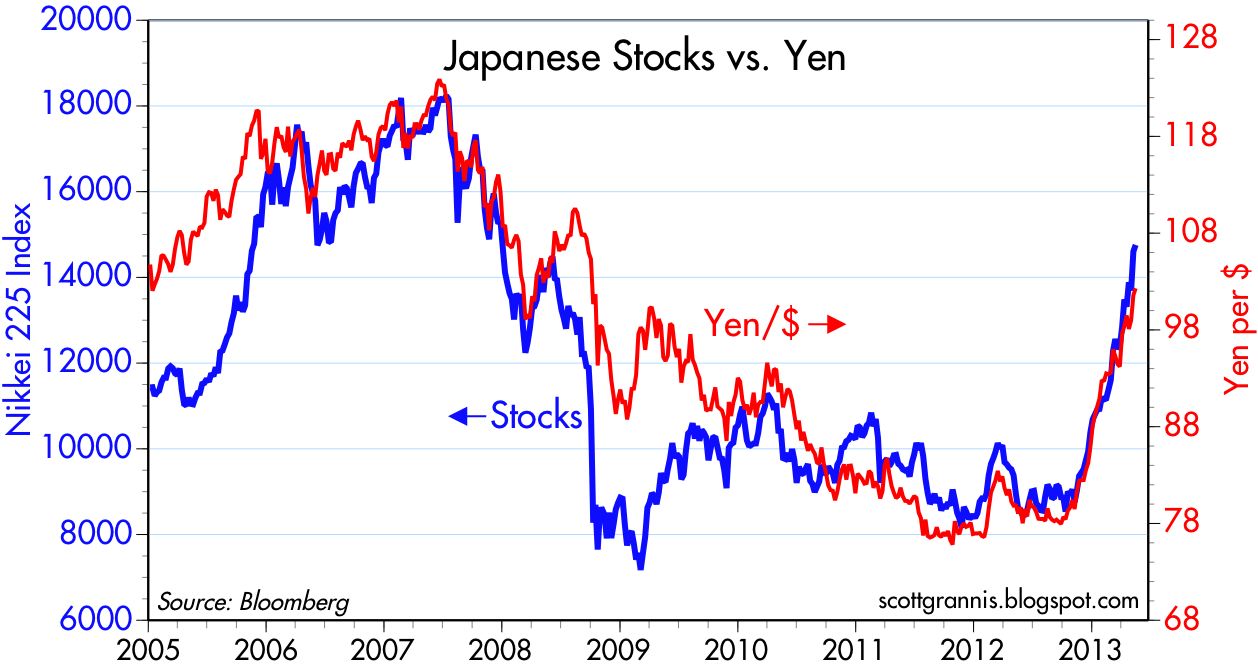

The strong inverse correlation between the yen and the Japanese stock market is a predictable result of monetary stimulus that reverses deflationary pressures that had been generated by the yen's relentless climb against all other currencies.

The chart above shows the yield on 10-yr Japanese Government Bonds (JGBs). Note that yields are now higher than they were when the BoJ announced last November its intention to start buying lots of bonds. Yields fell for several months, but in the past few days they have soared as the market begins to realize that monetary stimulus designed to get rid of deflation, coupled with the promise of fiscal stimulus and other growth-oriented reforms, have already managed to stimulate the economy. As Bloomberg notes in a recent release:

Prime Minister Shinzo Abe's stimulus probably helped the Japanese economy grow the most in a year, adding to pressure on 2013's worst-performing bond market. Gross domestic product likely expanded an annualized 2.7 percent in the three months through March ... Japanese bonds declined 14 percent in dollar terms this year ... Inflation expectations rose to the most since at least 2009. Abe's push for monetary and fiscal stimulus to overcome more than a decade of deflation is invigorating demand among consumers ... The economic rebound is also spurring expectations that consumer prices will increase as the yen tumbles, causing bond yields to surge in spite of a doubling of debt purchases under BoJ Governor Haruhiko Kuroda. Consumer sentiment is improving and consumption is gathering steam at an unexpectedly rapid pace...

In short, to be effective, monetary stimulus must achieve the opposite of its stated goal, which is to reduce interest rates. Rising interest rates go hand in hand with stronger growth and rising inflation expectations.

The same scenario, but to a lesser degree, is now playing out in the U.S. As the above chart of 10-yr Treasury yields shows, yields are now higher than they were when the Fed announced its QE3 program in September, and when they increased the size of monthly purchases last December. Yields are up despite concerted buying by the Fed because the market is raising its expectations of U.S. growth.

This is also a good illustration of my long-held view that the Fed cannot artificially manipulate interest rates. Treasury yields have been very low not because of Fed bond purchases, but because the market was very pessimistic about the prospects for economic growth. Rates are now moving higher despite ongoing Fed purchases because the market is adjusting upwards its expectations for growth.

The above chart attempts to show how real yields on TIPS tend to track the underlying growth potential of the U.S. economy. When the economy was booming in the late 1990s, TIPS real yields were about 4%. But in recent years economic growth has moderated significantly, and real yields have fallen. The recent increase in 5-yr TIPS yields doesn't look like much in this chart, but it has been on the order of almost 60 bps, and that is significant. Despite the recent increase, the current level of TIPS yields is still consistent, I think, with a market that holds little hope for any meaningful economic growth in the years to come.

4 comments:

Now is the time to acquire world-class skills that earn premium wages that convert into dividend and rent-earning equities over a lifetime -- we are likely living through a once in a lifetime opportunity for those without wealth to acquire a mighty estate that will weather generations -- if only more people understood the opportunity before them...

Japan is proof tight money does not work, and that central banks, at times, have to be aggressive and sustained in their stimulative policies.

The idea of printing money to boost real output is heresy to many. But sometimes, one has to abandon religion to get things down.

Billy McKibs.

Summer of 2011... Weren't you the one who was recommending on Steve's message board that we all buy gold back when it was selling for 1900 an ounce?

Why yes you were!

In addition to being a supply sider, you´ve acquired a noticeable market monetarist streak!

Post a Comment