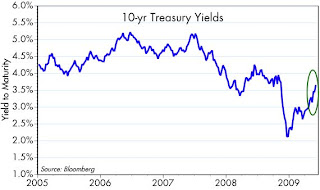

I've been talking about rising yields on T-bonds for most of the year, and saying that this was good news. It's good because it means that a) the market is losing its fear of deflation and b) the market is becoming more optimistic about the prospects for growth. Eventually, rising yields will be a sign of worrisome inflation expectations, but not yet. We're probably headed in that direction, as suggested by the steeper yield curve which is being driven solely by rising long-term yields and stable short-term yields. But inflation expectations remain "anchored" within the recent historical range of 2-3%.

I've been talking about rising yields on T-bonds for most of the year, and saying that this was good news. It's good because it means that a) the market is losing its fear of deflation and b) the market is becoming more optimistic about the prospects for growth. Eventually, rising yields will be a sign of worrisome inflation expectations, but not yet. We're probably headed in that direction, as suggested by the steeper yield curve which is being driven solely by rising long-term yields and stable short-term yields. But inflation expectations remain "anchored" within the recent historical range of 2-3%.Rising yields are a negative for the owners of Treasury bonds, but not for the owners of corporate bonds, since the spreads on the latter are contracting at least as fast as the yields on Treasuries are rising. So this chart is not a bad sign for corporate America. It's a warning sign for Uncle Sam and Obama, however, since it means the government's borrowing costs are rising. That may eventually be a good thing, since debt worries (which are absolutely genuine now) could help derail Obama's plans for further growth in government (e.g., cap and trade and universal healthcare).

UPDATE: I should add that, although 10-yr Treasury yields are a major determinant of mortgage rates, mortgage rates have not risen by much from their lows this year. Certainly not enough to create a significant problem for the housing market. Rates are still pretty close to all-time lows. This could change going forward, to be sure, but to the extent Treasury yields rise further it will be because the economy—and by inference the housing market—is doing much better. A stronger economy would almost certainly be able to support 6% fixed conforming mortgage rates, should it come to that. Then there is the other factor too: rising yields help boost demand for housing, since fence-sitters will be encouraged to act rather than wait.

5 comments:

What are your thoughts on the impact of rising yields on the housing market?

Rising yields are very bad for the housing market. Scott will say that they are good because they show signs of normalisation and subsiding fear etc.

Note my recent post on the subject of how higher rates will impact the housing market.

You've mentioned before that you are long TBT. I am too, but I keep wondering about the oft-mentioned daily reset, inherent decay problem (the negative residual after bonds go up x one day, and down x the next;i.e., (1 +2x)(1 - 2x)). So what does TBT offer that can't be achieved through shorting Treasurys or TLT?

Buying TBT and shorting Treasuries should theoretically give similar results. For the average investor, I think the main difference, assuming you are willing to trust the managers of TBT to do what they say they will do, is that the transaction cost of buying and selling TBT is likely an order of magnitude less than buying selling and buying Treasuries. The bid/ask spread on bonds for retail investors is a killer, almost prohibitive.

One thing I don't profess to understand, however, is how the managers of TBT are able to be short Treasuries without losing ground over time due to negative carry (i.e., when you short a bond you need to pay out the difference between bond yields and Libor). Every time I check it, it looks like they are able to track the inverse performance of Treasuries very closely, and I can't spot the effect of negative carry.

Another way to be short bonds, and probably the best, is through a short futures position. I don't happen to have a futures account at the moment, and don't want to be tempted now that I'm retired, so I default to TBT.

Post a Comment