A quick look at key market-based indicators of risk suggests that a U.S. recession is not very likely, and that there is little or no need for the Fed to do anything at this point.

10-yr Treasury yields have plunged to an all-time low of 1.5%, but 10-yr TIPS break-even rates show no sign of unusually low inflation expectations, and 5-yr, 5-yr forward inflation expectations derived from TIPS and Treasuries have actually been rising for the past 9 months and currently stand at 2.6%. This suggests that the decline in nominal yields is being driven not by declining inflation expectations—which in turn would be what we might expect if there were a need for the Fed to ease—but by sharply declining expectations for real growth. See my earlier post for more details on this theme.

Foreigners' insatiable demand for safe-haven assets that also offer a guaranteed yield is most likely the driving force behind the unprecedented low in Treasury yields, because it's hard to find evidence that the outlook for the U.S. economy is that dire. Plus, the decline in 10-yr yields began in earnest about the same time that the Eurozone financial crisis began heating up last summer, and 10-yr yields have closely tracked the decline in Eurozone equities.

The strong correlation between European economic conditions and 10-yr Treasury yields can be seen in the above chart (10-yr Treasury yields in white, and the Euro Stoxx equity index in orange). In contrast, U.S. equities have been trending higher for the past two years even as Eurozone equities have moved back to their 2009 lows. Clearly, the Eurozone is the epicenter of the world's growth and financial concerns.

I've shown this chart many times in the past several years, and it continues to be useful, because it strongly suggests that the U.S. economy is not currently at risk of a recession. What it shows is that every recession in the past 50+ years has been preceded by 1) a pronounced rise in the real Federal funds rate, and 2) by a flat or inverted Treasury yield curve. In other words, tight monetary policy has been the proximate cause of every recession in the past 50 years. Currently, we are very far from seeing either of those two conditions prevail, thus the likelihood of a near-term recession is very low.

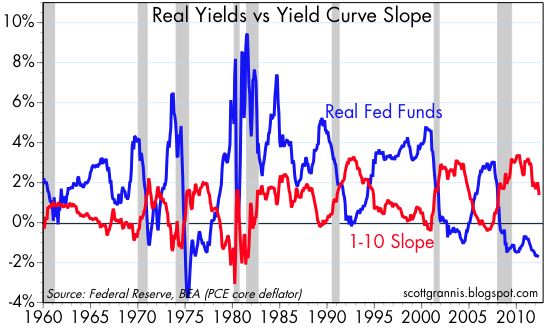

The logic behind this chart is fairly simple. The blue line represents the real Federal funds rate, which is one of the best ways of determining whether monetary policy is tight or loose—the Fed itself uses this as a gauge of how easy or accommodative policy is. The higher the real funds rate, the tighter monetary policy is, and very tight monetary policy is main tool the Fed uses to slow economic growth and reduce inflation pressures. To judge from this chart, whenever the real funds rate exceeds 3% it's time to start worrying about a recession. Today, however, the real funds rate is -1.6%, and it has rarely been lower.

The red line measures the slope of the Treasury yield curve from 1 to 10 years' maturity, and this is another way of gauging how easy or tight monetary policy is. A steep yield curve is the result of the bond market anticipating a future tightening of monetary policy. The steeper the curve, the more the market expects the Fed to tighten in the future; by the same logic, a very steep yield curve is an indicator that the Fed is very accommodative, and can't remain that accommodative for very long before it will have to start raising rates. A flat or inverted curve, on the other hand, means that the Fed is so tight that the market expects they will have to soon begin easing, because the market senses that the economy is suffering from high real yields and beginning to slow down. Currently, the yield curve is neither extremely steep, nor flat, nor inverted. This further suggests that the Fed is not as easy as the extremely low level of the real funds rate would suggest, but they are still easy.

That is, what has happened over the past year is that the Fed has become "less easy."

Since early last summer, just before the Eurozone crisis started heating up for a second time, the yield curve by this measure has flattened by almost 150 bps; and since mid-March, it has flattened by almost 100 bps, with almost all of the flattening coming from a decline in 10-yr yields. The chart above shows the steepness of the curve in a slightly different perspective, and here it should be obvious that despite the significant recent flattening of the curve, it is still a long way from being flat or inverted. In other words, the Fed is less easy than it was a year ago, but still easy.

We can also see evidence of less-easy monetary policy in the 15% decline in gold prices since last summer, in the 11% rise in the dollar, and in the 16% decline in the CRB Spot Commodity Index. (See the respective charts above.) If the Fed were really tight, commodities would be far lower than they are today; as it is, they are still significantly above the extremely low levels of 2001. Furthermore, the dollar would be much stronger that it is today, since it is still very close to historic lows and far below the highs of early 2002. All of these sensitive indicators of monetary policy have behaved in a manner consistent with monetary policy becoming less easy and dollars becoming less abundant.

2-yr swap spreads (above chart) are a good way of measuring how tight monetary policy is. When policy is very tight, dollars are in short supply and swap spreads tend to rise because systemic risk is rising and the economy is slowing; rising swap spreads are like the canary in the coal mine, warning that dangerous conditions are approaching. Although swap spreads have increased a little of late, they are still within what might be termed the safe zone—nowhere near high enough to indicate a serious problem. Again, this is consistent with monetary policy that has become less easy, but is still far from being too tight.

Credit default swap spreads can sometimes, but not always, be a measure of how tight monetary policy is. If policy is very tight, then dollars become scarce, the economy slows, and deflation risk rises, and all of those conditions increase default risk. In the chart above, we see that default risk has indeed risen of late, and currently is at a level that preceded the last recession. But taken in the context of other indicators which suggest that monetary policy is less easy but still "easy," I think it's safe to say that the cause of the rise in CDS spreads has very little to do with U.S. monetary policy and everything to do with the problems in the Eurozone. The market is legitimately concerned about the risk of Eurozone contagion, but so far there are no signs of recessionary forces building inside the U.S. economy.

How has the Fed become less easy if they haven't announced such a change in policy? That's easy: the Fed has become less easy inadvertently, because they have not responded to an increase in dollar demand from global investors. As a result, dollars have become somewhat less abundant in the past year. Not in short supply, simply less abundant. On the margin, there has been the equivalent of a modest tightening of monetary policy, but not by enough to threaten the economy. This is a very important distinction.

What this means is that the Fed should not feel greatly pressured to implement a third round of quantitative easing. The problems the world is facing are not because the Fed is too tight (like they were in 2008, when they failed to ease in response to a huge increase in the demand for dollar liquidity, which in turn led to a 25% plunge in gold and an unprecedented surge in swap spreads), but because of the trauma facing the Eurozone countries. There is very little the Fed can or should do to address that issue; it's simply not our problem.

This is not to say that there is zero risk of a recession, but rather to say that to date there are very few signs that a U.S. recession is imminent or even likely, and almost no indication that the Fed needs to initiate another round of quantitative easing.

21 comments:

you got your facts wrong. 5 year inflation expectation is NOT at 2.6%. It's only 1.7%.

Pretty much all you are saying is that as long as the Fed keeps rate at 0, we will never have recessions. You make economics sound like kindergarten stuff.

The 5-yr, 5-yr forward inflation expectation I cite is calculated by Bloomberg, and my own calculation confirms that. Moreover, this is the measure of inflation expectations that the Fed most prefers to follow.

I think I made it clear that the level of the real Fed funds rate is only one of many variables that can point to the likelihood of recession.

Where is Benjamin? I haven't seen him post for some time. I miss his persistent insistance on more Fed easing and our need to tolerate a little more inflation, and his warnings that we're in danger of becoming Japan.

Check out the bloomberg web site yourself. 5yr Treasury is at 0.68 while 5yr TIPS is at -1.03. You do the math.

http://www.bloomberg.com/markets/rates-bonds/government-bonds/us/

That is not how forward inflation expectations are calculated.

Although I was an early advocate for monetary expansion, that path was rejected in favor of austerity instead -- given that reality, the US should stay the course on austerity -- that means no money to bailout California, no money for mortgage holders, and no money for infrastructure development -- if austerity is to work, what is needed instead is a 40% cut in Federal and state spending -- that will mean eliminating popular programs such as Social Security, Medicare, and public education, but also ending overseas wars -- should these cuts lead to riots, the armed forces should be used to restore order regardless of the costs -- unfortunately, that's what austerity means -- what we see going down along the southern flank of Europe is a good preview of events still to come in America -- however, a good 10-15 year period of deep budget cutting is required to make austerity effective -- again, I was an early advocate for monetary expansion, but given the austerity path that America is now on, both Federal and state governments should go all out with cuts -- the good news is that austerity can work for investors, which is what America is all about -- accredited investors with cash are in a strong position to capitalize on the coming austerity measures.

Our beautiful Naples provided apartments and homes are among the advisable joint housing in the Naples extent. With our warm and deliberate staff, you testament be provided relocation options to fit your requirements and be healthy to select your perfect short-term or long-term accommodations.

naples corporate housing

If I have to guess, you are referring to 5yr inflation expectations 5yrs out, in other words inflation from 2017 to 2022. That's like light years away. Inflation expectation for the next 5 years is much lower.

"mmanagedaccounts said...

Where is Benjamin? I haven't seen him post for some time. I miss his persistent insistance on more Fed easing and our need to tolerate a little more inflation, and his warnings that we're in danger of becoming Japan."

Ben Jamin, is now an adviser for the Bank of Nippon..He told me that he has also had a Yen for it!

Thank you for the interesting and lengthy read, Mr Grannis.

"In other words, tight monetary policy has been the proximate cause of every recession in the past 50 years."

Have the Central Banks found a way to avoid further cessions?

I thought CDWs are insurance for bond issuers in case of missed payments or default?

I do not know what a tight monetary policy has to do with a traded insurance instrument..

Do CDWs not rise or fall upon the credit worthiness of the underlying bond?

Is it as simple as just the money supply??

If Bank Bernank reads this thread, then the Central Bank will take no action on June the 18th or the 19th..

Pragmatic-

What? If you are buying anything longer dated than a 5 yr. bond, you sure as hell want to know the 5yr inflation expectation 5 yrs. out...

Scott, Thanks for taking my suggestion yesterday and updating these likliehood of recession charts.

For those really interested in recession forecasting...subscribe to

RecessionAlert...I have no vested

interest in the service...but find it

very helpful in following the 9 to 10

models that attempt to forecast recessions...

Donny,

If you buy anything longer than 5yrs, you want to know what's going to happen 5 years out as well as the immediate 5 years. Then just look at 10 years. No reason to look at 5 years out forward only. I don't know why the Fed will care about inflation 5 years out more than the next 5 years if it shows deflation risk.

http://www.clevelandfed.org/research/commentary/2010/2010-5.cfm

Start here to learn how they figure 5 yr 5 yr out inflation expectations.

Yield curves do not invert during secular debt deleveraging contractions - I refer you to Japan for evidence.

Moreover, you are referring to a batch of data of a past - the post WW2 era - that is simply not relevant to the current predicament. The only historical period that can remotely be of relevance to the current situation is the Great Depression, the last major debt deleveraging event in US history.

As ECRI has pointed out, a recession is not only likely, it is extremely likely.

Hans asks: 'Have the Central Banks found a way to avoid further recessions?'

Unless this is a trick question: their credit expansions cause booms that inevitably turn into busts. It would be correct to state that they are the proximate cause of recessions.

Re: deleveraging. Yes, we have had a lot of deleveraging in recent years but that's not necessarily a bad or scary thing. Wanting to deleverage can be thought of as an increase in the demand for money. (Leveraging up is a decrease in the demand for money.) We have seen a huge increase in the world's demand for dollar liquidity in recent yearsr. Fortunately, the Fed has increased massively the supply of dollar liquidity via its QE efforts, which have created over $1.4 trillion of bank reserves. This has effectively prevented an experience such as we had in the Depression, in which a shortage of liquidity fueled a significant economic contraction. Not coincidentally, Bernanke is a student of these problems and has vowed to not let them repeat. So far, he has done a pretty good job.

Great insight as always Scott.

Steve

Thanks Steve

Post a Comment