Here are some charts and thoughts to round out the picture:

Chart #1

Chart #1 compares stock prices (blue line) with a measure of the market's fears and uncertainties (red line). When fear (the Vix index) rises and uncertainty rises (i.e., as strong demand for the safety of 10-yr Treasuries pushes yields down), stock prices have a strong (and understandable) tendency to weaken. Most of today's concerns revolve around Trump's tariff wars, as has been the case for most of the past year.

I note that the S&P 500 rose at a 14% annualized rate during 2016 and 2017, boosted no doubt by a significant reduction in corporate tax rates. But gains have been only about half as much from 2018 to today. The latter is most likely more suggestive of future returns than the former. Still, the prospect of 7% price gains plus 1.5% dividend gains going forward—while in line with long-term trends—is an order of magnitude larger than the returns on 10-yr Treasury bonds. The equity risk premium is still compelling for those willing to take the risk.

Chart #2

Chart #2 compares an index of manufacturing health (red line) with the quarterly annualized change in real GDP growth (blue bars). The relationship between the two has weakened considerably in the past decade, however. And regardless, the huge decline in the manufacturing index over the past two years has failed to put it in territory that in the past has coincided with recessions. At current levels, the ISM index suggests that overall economic growth in the current quarter will probably be 1-2%, which not surprisingly happens to be the market's current consensus.

Chart #3

As Chart #3 shows, the big decline in the manufacturing index began early last year with Trump's imposition of punitive tariffs on Chinese goods. But as the chart also suggests, we have probably seen the worst. The Markit manufacturing index has turned up of late, as has the Eurozone manufacturing index.

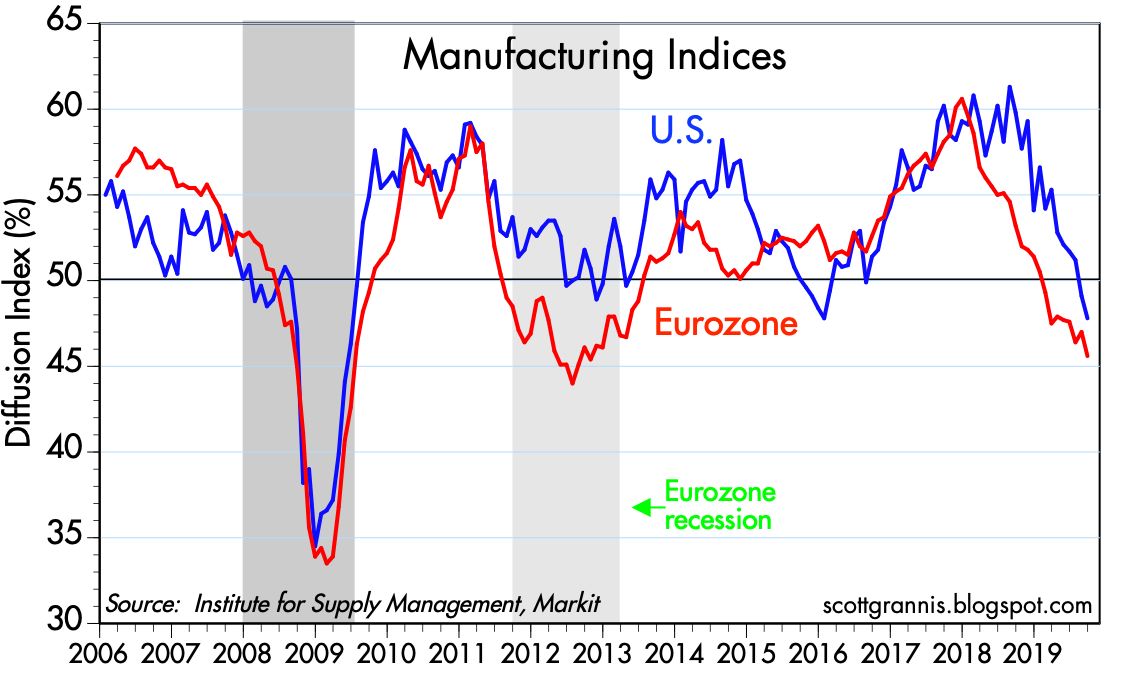

Chart #4

Chart #4 compares manufacturing conditions here and in the Eurozone. Both have weakened during the Trump tariff wars. Conditions appear to have improved a bit in the Eurozone of late.

Chart #5

Chart #5 shows the relationship between real yields on 5-yr TIPS (a good proxy for real yields in general) and real GDP growth (which I measure over a rolling 2-yr period to get a proxy for the market's perception of trend growth). Not surprisingly, real yields tend to track real economic growth trends. A very strong economy demands high real yields, whereas today's near-zero real yields point to modest 2% real growth rates. In short, the bond market is priced to 2% real growth for the foreseeable future. That's not enough to convince the Fed to raise rates, but it's slow enough to justify the current low level of rates.

Chart #6

Chart #6 compares the level of the Chinese yuan with the level of China's foreign exchange reserves. For the past several years, the Chinese central bank has been targeting stable forex reserves, which means that strength or weakness in the yuan is a direct reflection of changing demand for yuan. Under this monetary regime, if capital tries to leave the country, the central bank allows the yuan to weaken; if capital flows turn positive, the yuan strengthens. The yuan has fallen about 11% vs the dollar since Trump's imposition of punitive tariffs on Chinese goods. This reflects deteriorating expectations for the Chinese economy and it also serves to lessen the impact of tariffs on US consumers, since a weaker yuan gives exporters the ability to lower their prices (since they receive more yuan for a given level of dollar sales) in order to offset the impact of US tariffs. Bad for China, but good for the US.

Chart #7

As Chart #7 shows, the weaker yuan has caused Chinese inflation to rise relative to US inflation. A weaker yuan makes the prices of all imported goods rise, and that helps fuel a rising price level in China.

Chart #8

As Chart #8 shows, thanks to a decline in the yuan's value vis a vis the dollar, US tariffs have not impacted China's exports to the US as much as higher China countervailing duties (and a weaker yuan) have negatively impacted China's imports of US goods. The Chinese economy is suffering as a result: rising inflation, weak currency, declining imports and exports, and slowing economic growth.

Chart #9

Chart #9 shows that world trade volume has been flat to slightly down as a result of global tariff wars. Nobody is benefiting from Trump's tariffs. But if they convince the Chinese to reform their ways, and Trump responds by reducing or eliminating tariffs, then the world will be better off in the end. That's my hope.

Chart #10

Chart #10 shows that business investment has been relatively weak for the past several years. That's disappointing given the significant reduction in corporate tax rates, but it's somewhat understandable given the general climate of fear, uncertainty and doubt (FUD), which in turn is driven in large part by the potential for tariff wars to foster global economic weakness.

Chart #11

Chart #11 shows that capital goods orders—a good proxy for business investment—have been flat for the past year, thus reinforcing the message of Chart #10. Business investment has been and continues to be a disappointment, and that is keeping the economy in slow-growth mode.

Chart #12

Jobs growth in the US has slowed over the past year, but with modest productivity growth (~1%) this suggests that 2% economic growth is likely to continue. Slow jobs growth is likely the product of weak business investment and a shortage of experienced labor.

Chart #13

Chart #13 shows the remarkable and unprecedented decline in weekly unemployment claims. This reinforces the idea that the slowdown in jobs growth has more to do with a reluctance to invest on the part of business and a shortage of qualified labor, rather than businesses reacting to a deteriorating economy by cutting back. What turnover remains in the labor market is mostly a function of workers looking for new opportunities. How many people do you know who have been given an unexpected pink slip this past year?

Chart #14

Chart #14 shows Bloomberg's survey of consumer confidence/sentiment. It has risen strongly since Trump won the 2016 election. Every measure of consumer sentiment is at relatively high levels from an historical perspective. And why not? Layoffs have never been so low relative to the size of the labor force. The unemployment rate is very low. Real median family incomes are at record highs. Mortgage rates are near all-time lows.

Chart #15

As Chart #15 shows, households' financial burdens (recurring payments as a percent of disposable income) are about as low as they have ever been.

Chart #16

The housing market shows no signs of a bubble. Indeed, housing starts are still historically low and are likely still in an uptrend, judging by builder sentiment (see Chart #16). Applications for new mortgages (not including refis) have risen 67% in the past 5 years, thanks to mortgage rates that are about as low as they have ever been. Yet the the volume of new mortgage applications today is only about half what it was at the peak of the housing market "bubble" in 2005-6. The housing market is on solid ground these days.

Chart #17

It's hard to find any sign of financial distress or instability. Chart #17 shows the all-important level of 2-yr swap spreads in both the US and the Eurozone. Very low spreads imply abundant liquidity and a very low level of systemic risk. This in turn portends a healthy outlook for the economy, since swap spreads have been good leading indicators of financial and economic health.

Chart #18

Chart #18 shows Credit Default Swap spreads, a highly liquid measure of generic credit risk. Spreads are very low, suggesting that the outlook for corporate profits—and by extension the economy—is healthy.

Chart #19

Chart #19 shows the classic measure of the slope of the Treasury yield curve. It's now slightly positive. The Fed's last interest rate cut brought short-term rates down to a level below that of long-term rates. This further suggests that Fed policy is not restrictive or otherwise threatening to the economy.

Chart #20

As Chart #20 shows, real, inflation-adjusted short-term interest rates are now roughly zero. Virtually all past recessions were preceded by unusually high real interest rates. Fed policy is once again accommodative. Borrowing costs are unusually low.

Chart #21

Chart #21 underscores just how risk-averse the world is these days. It shows the 3-mo. annualized rate of growth of bank savings and demand deposits. Despite short-term interest rates trading at historical lows, both in nominal and real terms, demand for "safe" deposits that pay almost nothing has exploded. Trump's election in late 2016 kicked off an impressive decline in money demand, but Trump's tariff wars have largely reversed this. While it's unfortunate this has occurred, it's important to recognize that any improvement in the global trade outlook has the potential to unleash a tsunami of cash.

In my judgment, it pays to remain optimistic.