There are lots of things going on in the world, with the most significant, in my view, being the threat of nuclear war in/with North Korea, followed by deteriorating US-Russia and Mideast relations. On the domestic front, Trump has yet to make meaningful progress on an alternative to Obamacare or on tax reform, but he has made important progress with most of his nominees. However, if we don't get substantial progress on healthcare and taxes before year end, the economy could weaken as uncertainty mounts and people delay income and investment decisions. In the meantime, the nascent

rebound in the manufacturing sector and the likelihood of improving

corporate profits should sustain the economy for the next several months; but for now, the economy continues to plod along and markets are less than enthusiastic about the future.

What follows are updates of some of the more important charts—all based on market-driven prices—that I am following. These tell us what the market is thinking, as expressed in the prices of the dollar, gold, real and nominal interest rates, equity prices, volatility, swap and credit spreads, and commodity prices. As I read the charts, the market seems relatively unperturbed by all the turmoil, and hopeful that better times lie ahead. This in turn makes the market vulnerable to any shortfall vis a vis expectations, so now is one of those times to be cautiously optimistic rather than gung-ho.

If the US economy were a company, then the value of the dollar would be a good proxy for its relative attractiveness and its future prospects. The chart above shows two of the best measures of the dollar's value, on an inflation-adjusted, trade-weighted basis. By either measure, the dollar is moderately above its long-term average We can infer from this that the Fed has not printed more dollars than the world wants, though it might be guilty of supplying too few. On the other hand, it would appear that the dollar is one of the currencies in most demand, and that is encouraging since it means the US is attracting investment, and investment is the seed corn of future growth.

The chart above illustrates the tendency of commodity prices to move inversely to the value of the dollar (note that the dollar axis is inverted). In the past few years, however, both the dollar and commodity prices have moved higher. This is worthy of attention. I think it tells us that the rise in commodity prices has little or nothing to do with a monetary reflation (because a plentiful supply of dollars tends to boost the prices of most things (aka inflation), but rather more to do with a general strengthening of the global economy at a time when the US economy is expected to be one of the engines of stronger growth. Again, this is encouraging.

The chart above shows the very strong correlation between industrial commodity prices and emerging market equities. That makes sense, because emerging market economies tend to specialize in the production of raw materials. I believe the rise in commodity prices reflects a general strengthening of global economies, so what's good for commodities is good for just about everyone, especially emerging markets. And as I pointed out in

December 2015, emerging markets and commodities had been severely beaten up and prospects for their recovery were bright.

For years I've been amazed at the correlation between gold and TIPS prices, as shown in the chart above (note I use the inverse of the real yield on TIPS as a proxy for their price). The common denominator of both markets is the way they serve to protect people from risk. TIPS are a good hedge for inflation, they are default-free, and they are the only asset that guarantees investors a real rate of return if held to maturity. Gold, on the other hand, is a classic port in a storm for just about anything that makes people nervous about fiat currencies or government excesses. Gold and TIPS have been in a rough holding pattern for the past several years. Declines in gold and TIPS would likely coincide with improvements in the global economic outlook. That they have not yet fallen meaningfully is therefore a good sign that markets are still somewhat risk averse and less than optimistic.

It's almost always the case that stocks tend to weaken as fears tend to rise, as shown in the chart above. But the current level of fear and uncertainty (as reflected in the ratio of the Vix index to the 10-yr Treasury yield) is still quite modest compared to what we've seen in recent years. The Trump era seems to have brought with it a calming effect on global markets.

Swap spreads are some of the best coincident and

leading indicators of financial market and economic health. Spreads have been rising for the past year or so both in the US and in the eurozone, so that could be a sign of deteriorating economic and financial fundamentals. I've tended to dismiss the current rise in US swap spreads, however, because they are still within what we consider to be a "normal" range (20-35 bps); if anything, they were exceedingly low at the end of 2015 and only now have recovered to more normal levels. Eurozone swap spreads have moved substantially higher, however, and that is cause for concern. My guess is that eurozone swap spreads are elevated because of concerns that France could pull a "Frexit," and this could undermine the stability of the euro and the eurozone economy. This risk is not trivial, and is not one to dismiss lightly—unless you believe (as I do) that the demise of the eurozone would not be necessarily a bad thing. For the moment, I note that credit default spreads on French debt are declining (i.e., the market is worrying less about a Frexit since the political left seems to be ascendant for the moment), but this still bears watching.

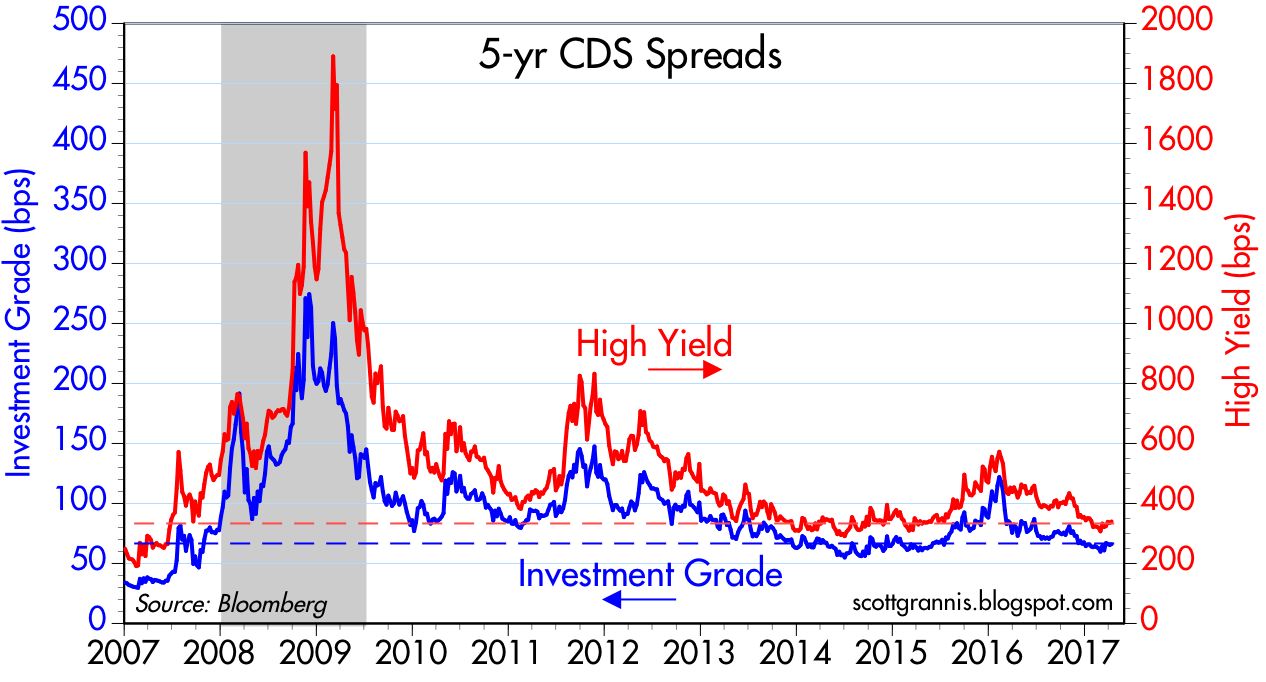

Speaking of credit default spreads, the chart above shows that they are relatively low here in the U.S., and that further suggests that systemic risks are low and markets are relatively confident about the future.

One persistent and salient feature of the past 6-7 years has been Treasury yields in the US that are very low relative to inflation, as the chart above shows. Some observers dismiss this with the argument that the Fed is keeping interest rates artificially low, but I'm not a buyer of that line of thinking. I think Treasury yields are very low because markets still have a palpable degree of risk aversion, and are thus willing to pay a lot for the protection of Treasuries. We see this same phenomenon all over the developed world: sovereign yields are unusually low. Most investors have a choice between holding Treasuries and holding riskier assets; that the price of Treasuries is unusually high relative to other assets (e.g., the earnings yield on the S&P 500 is substantially higher than the yield on 10-yr Treasuries) must therefore mean that investors are very distrustful of the outlook for the economy and for corporate profits. In other words, very low Treasury yields are a strong and reliable indicator of a market that is less than optimistic, to say the least. Show me an optimistic/enthusiastic market, and I'll show you nominal Treasury yields that are much higher than they are today.

The difference between nominal and real yields is a measure of the market's inflation expectations. In the chart above we see that inflation expectations over the next 5 years (the green line) are 2%, and not surprisingly, that is what the CPI has averaged over the past few decades. Markets are not concerned about rising or falling inflation right now; it's steady as she goes. Kudos to the Fed for having managed monetary policy surprisingly well over the years.

The chart above is my attempt to show that the level of real yields on TIPS can and does tell us a lot about the market's expectations for real economic growth. Real growth has averaged about 2% during the current expansion, and 5-yr TIPS yields have averaged about zero. You can invest in the economy and expect to get an average real return of 2%, or you can invest in TIPS and earn a guaranteed zero real rate of return. Guaranteed real rates of return should always be less than expected real rates of return, should they not?. If and when TIPS yields rise significantly, this will be a good indicator that the market is expecting economic growth to accelerate. For now, it may be the case that the market is buoyed by Trump expectations, but to judge from TIPS yields, there is little or no evidence of much optimism.

The chart above shows the 6- and 12-month growth rates of private sector jobs in the US. If anything, jobs growth has slowed over the past few years, from just over 2% to currently about 1.7%. The manufacturing sector looks to be picking up, but the overall economy remains on a sluggish growth trend that of late has been declining modestly on the margin. No sign here of a Trump bump, and it's premature to expect one: we need to see meaningful tax and regulatory reform (or solid reasons to expect such) before getting excited.