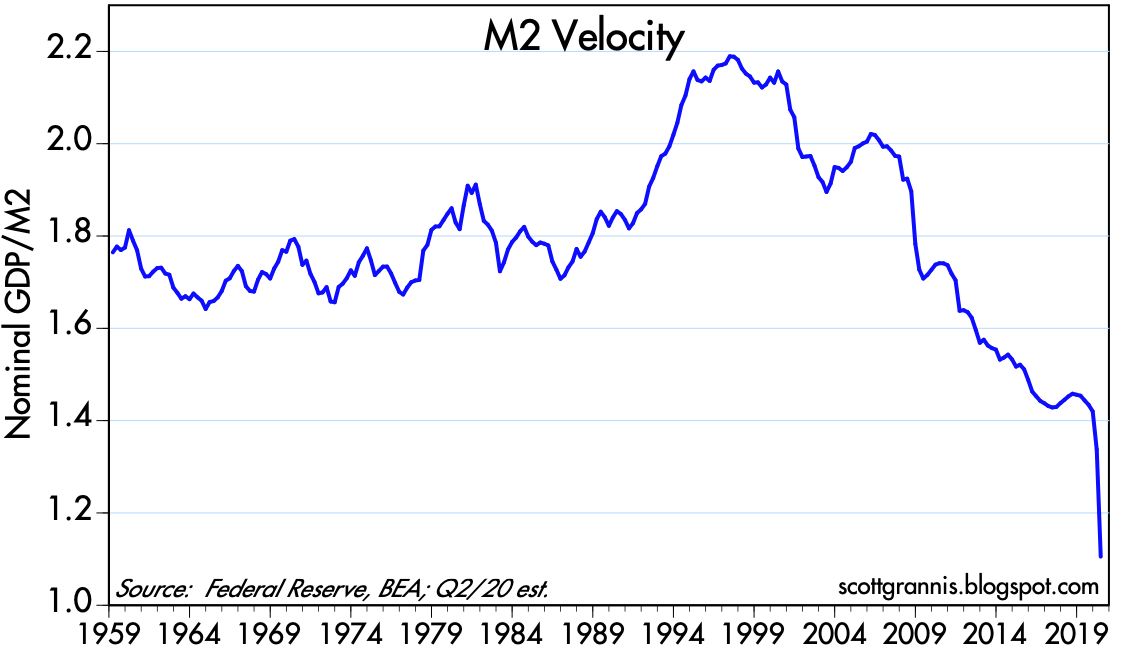

Chart #1

In the 3 months leading up to May 11th (latest data available), the M2 measure of the US money supply has increased at an 82% annualized rate. In the past six months, it's up at a 40% annualized rate, and in the past year, M2 has increased by over 23%, and these numbers will go higher in the next week or two. This is serious, Argentine-style money growth. The big question now is whether so much monetary expansion will give us Argentine-style inflation.

Chart #2

Chart #2 shows the year over year growth rate of Argentina's M2 money supply, which is up 97% in the past year. From late 2010 through early 2018, Argentina's money growth averaged about 30% per year, and inflation was in the neighborhood of 25-30% per year. Given the recent surge in money creation, inflation in Argentina is going to be approaching 100% before too long.

Chart #3

Chart #3 shows what a decade or so of rapid money growth has done to the value of the Argentine peso. Since early 2007, the peso has fallen from just over 3 to the dollar to now 117; that translates into a 97.5% loss of value vis a vis the dollar. Since the Argentine government locked down the economy fiercely in order to fight Covid-19, revenues have all but dried up. The only way it can pay the bills is to literally print money.

I've been an avid student of monetary policy and inflation ever since I spent four years living in Argentina in the late 1970s. Back then, inflation averaged about 125% per year, and during a visit to the country in the mid-1980s I was fascinated to watch hyperinflation unfold: prices almost tripled within the span of three weeks. In 2015 I wrote a post on the subject of inflation and Argentina, in which I explained that the conditions in Argentina that allowed a huge increase in inflation didn't exist in the U.S., despite the Fed's massive expansion of its balance sheet and the creation of trillions of dollars of bank reserves. Unlike the US, the government of Argentina relies on direct printing of money to finance its deficit, whereas the U.S. government finances its deficit by selling bills, notes and bonds. When the Argentine government needs to finance a budget shortfall, it can "borrow" money directly from its central bank in exchange for an IOU, which in practice is never repaid. In essence, the Argentine central bank simply runs the printing presses whenever the government needs money, and the government pays its bills with monopoly money.

Will the same happen to the US? I sincerely doubt it, but it's not impossible.

In 2013 I wrote a post entitled "The Fed is not printing money," which addressed in detail why the Fed's monetary expansion in the wake of the Great Recession was not inflationary. Over the years since then I have consistently argued that the Fed's huge expansion of bank reserves was unlikely to lead to higher inflation since the Fed was correctly supplying reserves to accommodate the banking sector's demand for safe assets (bank reserves are functionally akin to T-bills). Inflation only happens, as Milton Friedman taught us, when the supply of money exceeds the demand for it. And indeed inflation has remained relatively low and stable for most of the past decade—which in effect proves that the Fed was not "printing money."

The key feature of the US monetary system is that the Fed can not create money directly—only banks can do that. The Fed can, however, make it easier for banks to create money by increasing the supply of bank reserves. Banks need reserves in order to collateralize their deposits. The Fed creates reserves by buying securities (e.g., Treasury bills, notes and bonds, and more recently, mortgage-backed securities and some corporate bonds). In effect, the Fed buys securities and pays for them with bank reserves. But crucially, reserves are not money that can be spent anywhere. The Fed simply swaps reserves for notes and bonds, thus transmogrifying longer-term securities into short-term, risk-free securities. Reserves have become equivalent to T-bills, since they are default-free and pay a floating rate of interest.

In times of great uncertainty and surging money demand, like today, the Fed fills the market's need for short-term safe securities by buying riskier securities and paying for them with risk-free reserves. If banks don't want to hold the reserves they can use them to support increased lending, which indeed does result in a monetary expansion. But if that expansion exceeds the market's demand for money, then higher inflation will be the result. The fact that inflation so far has not risen is proof that the Fed's actions have not been inflationary. Excess reserves—which now total $3.2 trillion—have served to satisfy the banking system's demand for risk-free, short-term assets, and more recently to satisfy the public's demand for a massive increase in bank savings deposits and checking accounts, as shown in Chart #4, which in turn has been turbo-charged by all the uncertainties and disruptions caused by the Covid-19 panic:

Chart #4

Looking ahead, the most important question becomes, "What happens when the Covid uncertainties decline and the demand for risk-free assets declines?"

If the Fed does not reverse course in a timely manner (e.g., by selling notes and bonds and extinguishing bank reserves), then we will find ourselves flooded with unwanted money. And as Argentina has demonstrated, that can lead to a big increase in inflation.

And that is what my friend Nuni Cademartori is illustrating in the cartoon which follows. Too much money erodes the value of money. I've got stacks of million-peso Argentine notes printed decades ago that today are worth about the same as toilet paper.

Let's hope this does not come to pass in the US: