Economic growth is a function of two major factors: growth in the number of people working, and growth in the output of those working (i.e., the productivity of labor). For most of the current business cycle expansion, which has been the weakest post-war expansion on record, productivity has been

unusually weak, averaging about 1% per year. Prior to the Great Recession, productivity averaged over 2% per year. Productivity and jobs growth are in turn a function of investment, and investment—no surprise—has been unusually weak for the past 9 years, despite the fact that corporate profits have been

unusually strong. Investment is the seed corn of future growth, since investment builds new businesses, creates new jobs, and gives workers the advanced tools necessary to increase their productivity.

Something has been holding back the economy, and it might be as simple as a general unwillingness on the part of business to expand and invest in new plant and equipment. Confidence is key, and confidence has, until fairly recently, been low.

Risk aversion, by the same token, has been rather high.

(Note my supply-side bias: Supply-side economists believe that investment, hard work, and risk-taking are what drive the economy, not spending. In our global economy, total spending can never exceed total production. Increased production (supply) is the key to increased spending (demand). Beware of all those economists who say the economy is weak because the consumer is not spending enough; they are not seeing the whole picture.)

If the economy is going to grow by 3% or more, productivity is going to have to increase (and maybe jobs growth, but not necessarily), and that means that investment is going to have to increase. Increased investment is likely to follow from lower corporate tax rates, and from increased confidence and an increased willingness to take risk. Thanks to the bulk of Trump's policies, we have the essential ingredients for a stronger economy: lower tax rates on business and business investment, reduced regulatory burdens, and a more business-friendly climate in Washington. There are early indications that the economy is picking up steam (e.g., business investment is up in the past 18 months, and real yields are up), but it's still premature to declare victory.

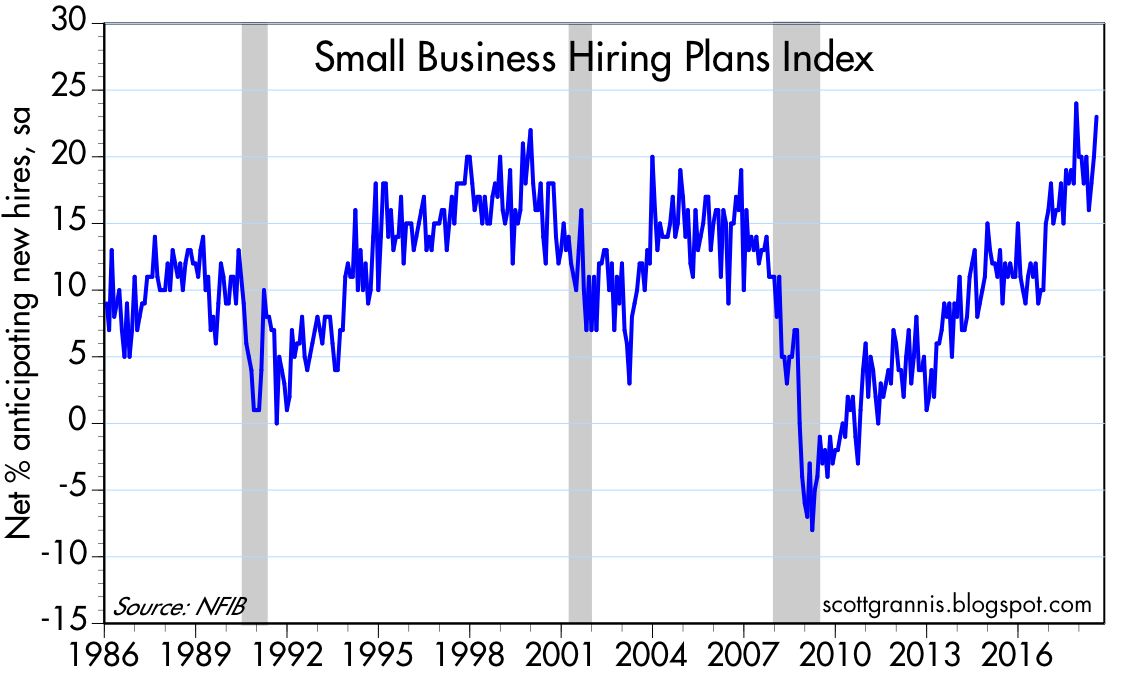

Here are two charts which are particularly impressive in this regard, since they document a pronounced and sustained increase in small business optimism and hiring intentions—an increase that dates to December 2016, just days after Trump was elected. Small businesses generate the vast majority of new jobs, and they are a vital source of innovation and productivity. These charts argue convincingly for a stronger economy in the months and years to come, thanks to increased business optimism and investment. (Both charts reflect survey results as of July '18, released today.)

Chart #1

Chart #2

Unfortunately, things are never so straightforward. While we undoubtedly have the essential ingredients in place for a significant pickup in economic growth, we also have—from the same pro-growth Trump who advocated for lower tax and regulatory burdens—an escalation of tariffs, which suppress growth by making imports more expensive for everyone.

I think Trump's ultimate objective is to reduce tariff barriers. I think he sees higher tariffs as a negotiating tool to eventually arrive at a reduced and even zero-tariff world. But for his negotiations to succeed, he has to convince our trading partners (particularly China) that he is willing to sacrifice some portion of US growth to achieve a result that would eventually be a win-win for all concerned. Suffice to say that this is a delicate balancing act. I'm optimistic he will succeed, but my confidence in that belief is not as strong as I would like it to be.

In short, Trump's tariffs are, for the time being, a headwind to growth, while his other policies are a tailwind.