Earlier today the FOMC temporarily rattled markets by signaling an increased likelihood that they would raise short-term rates by 25 bps at their next meeting, December 16th.(Bloomberg's implied probability of a rate hike by the December meeting rose from 35% this morning to 48% by the close.

In my view this is good news, if only because it shows that the Fed is somewhat less concerned about the economic outlook. Optimism has been in short supply for a long time now, so it's good to see less pessimism. A more-confident Fed can easily lead to more-confident markets, even if it means higher interest rates. (To be more specific: even if it means that interest rates will be less extremely low.)

In the meantime, the economy continues to grow, albeit relatively slowly, corporate profits continue to be relatively strong, markets continue to enjoy abundant liquidity, and key indicators of systemic risk remain unusually low. Moreover, it's hard (at least for me) to find evidence of irrational exuberance; on the contrary, I see lots of evidence that suggests the market is still cautious.

Arguably, it doesn't matter much whether the December FOMC meeting results in a rate hike or not. Regardless of whether the interest the Fed pays on reserves is 0.25% or 0.5%, short-term rates will be very low and monetary policy will most likely not pose a threat to economic growth for quite some time. The only thing likely to make a big difference to the outlook is the expectation of a pro-growth shift in fiscal policy, and that won't come until we get closer to next year's elections.

The equity market continues to shed its fear and uncertainty, as reflected in the decline in the ratio of the Vix index to the 10-yr Treasury yield. As fears of a China and oil patch meltdown recede, equity prices have risen.

The prices of gold and 5-yr TIPS (here proxied by the inverse of their real yield) have been slowly declining for the past several years. I have interpreted this to mean that pessimism and fear have been slowly replaced by optimism, because both gold and TIPS are assets that protect you from uncertainty. Even at current levels, gold is still trading at a substantial premium to its long-term average price in constant dollars, which I estimate to be around $500-600/oz. At today's 0.28%, real yields on 5-yr TIPS are still very low from an historical perspective, suggesting the market's expectations for real economic growth are still relatively anemic.

The real yield curve is still positively sloped (i.e., the difference between 5-year real yields and real overnight yields, shown here as the blue and red lines, respectively, is positive), which suggests that the market fully expects the Fed to be "tightening" policy in the years to come. This is to be expected in the early and middle stages of an economic expansion. If the market were really worried about a Fed tightening, and if the economy were really vulnerable to higher rates, the real yield curve would be flat or inverted, as happened prior to the past two recessions.

Inflation expectations (the blue line in the chart above shows the market's expectation for the average annual increase in the CPI over the next five years) are relatively low, but I think this is mainly the result of the significant decline in oil prices (red line) over the past year, as the chart suggests. As I've argued

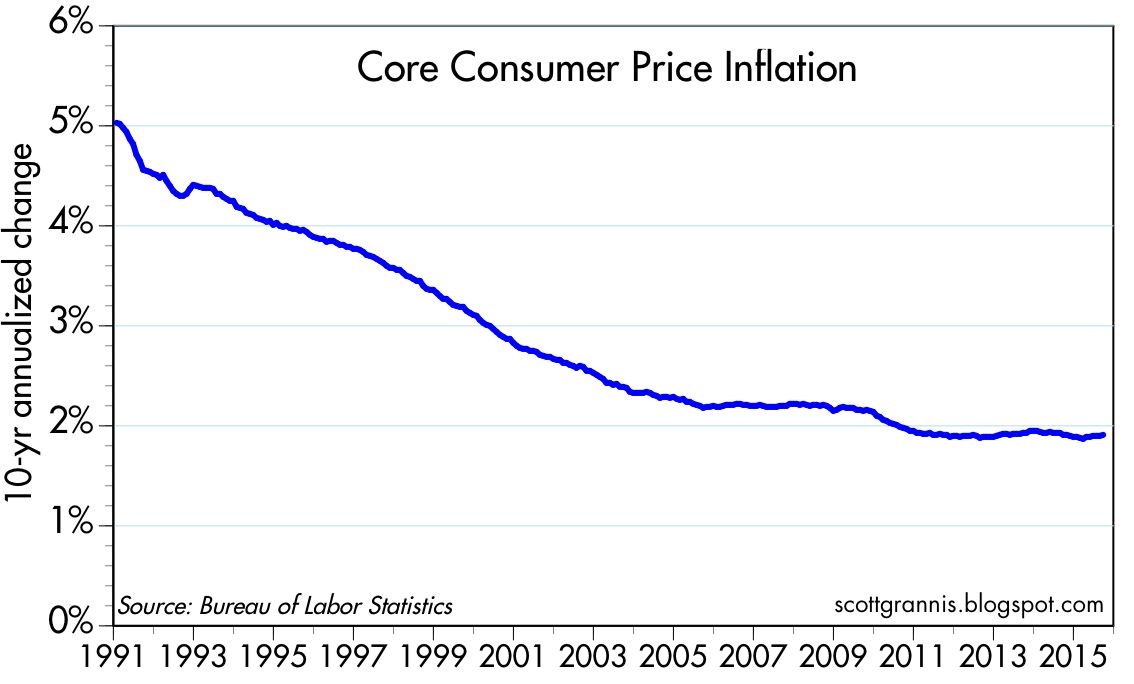

previously, the core and non-energy versions of the CPI have been running right around 2% for many years, and are likely to continue that pace. Today's low inflation expectations do not necessarily reflect monetary policy that is too tight.

The link between significant changes in real oil prices and inflation expectations holds up over long periods, as the chart above suggests.

2-yr swap spreads, shown in the chart above, are about as low as they get. If the economy and/or financial markets were really in trouble, swap spreads would be much higher. Current levels suggests that liquidity is abundant and systemic risk is very low. This is one of the healthiest indicators to be found anywhere, and it has gone largely unnoticed for years. Swap spreads are not only good coincident indicators, but also good leading indicators, and today they are telling us that economic conditions are likely to improve over the next year or so.

The S&P 500 closed today with a PE ratio of 18.5, according to Bloomberg. From an historical perspective, this is only modestly above average. Considering that corporate profits relative to GDP are at or near record levels (10% now vs. a long-term average of 6.5%), today's slightly-above-average PE ratios reflect a degree of caution and restraint.

I also find caution and restraint in the pricing of AAPL. As the chart above shows, Apple's PE ratio today of 13 is not only much lower than the market's PE, but also near the lower end of its historical range. This, despite the fact that Apple's earnings have surged over 40% in the past year, and the company is sitting on a mountain of cash—which makes its effective PE ratio more like 10. This means that the market is pricing in the expectation that Apple's earnings are likely to be flat or down for the foreseeable future. This is not unusual, since it has happened before: Apple's PE ratio was just above 10 in the first half of 2013, despite years of very strong double-digit earnings growth. That proved prescient, since Apple's earnings were subsequently flat to down for the next year. I would note, however, that while Apple's stock price averaged just over $60 in the first half of 2013, today it closed at nearly twice that.

It's fine to be cautious, but it may be premature to be bearish.