If there is anything unusual out there, it's the fact that short-term interest rates have dropped some 70 bps this year, presumably because the bond market is guessing that there may be a Fed rate cut or two in the foreseeable future. I don't see the rationale for a near-term cut, but many argue that the global economy remains quite weak, and in any event our recovery—now in its 10th year—is growing long in the tooth. In short, markets are still quite cautious despite lots of encouraging news: swap and credit spreads remain quite low and stable, liquidity is abundant, real yields are low, the dollar is moderately strong and relatively stable, gold and commodity prices are relatively stable, and the threat of a trade war is receding almost daily.

I don't see the Fed doing anything near-term, but as the year progresses, I think the odds favor higher interest rates as the economy continues to build momentum.

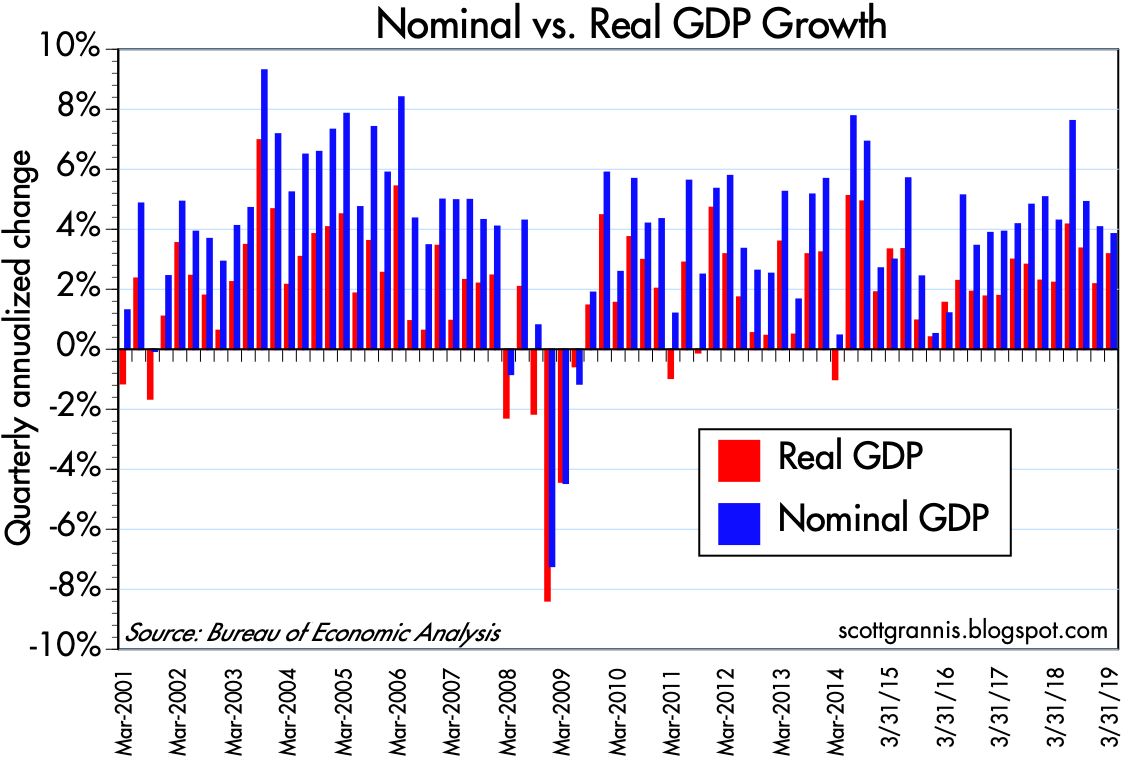

Chart #1

Chart #1 shows the quarterly annualized rates of growth of real (red) and nominal (blue) GDP. The red bars have been trending higher ever since 2016, but real growth is still weaker than we saw in the boom years of the mid-1990s.

Chart #2

Chart #2 shows the year over year growth of real GDP. Here we see a sustained spurt of growth beginning in late 2016 and continuing. Trump can claim to have delivered 3% growth as promised.

Chart #3

Chart #3 is my famous GDP Gap chart. It plots the level of real GDP on a semi-log axis, which makes a straight line equivalent to a constant rate of growth. Note that the economy grew on average by just over 3% per year from 1966 through 2007. Sometimes it exceeded that rate and sometimes (during recessions) it fell below that rate, but recoveries always brought the economy back to its 3.1% long-term trend. Unfortunately, the economic recovery since 2009 has failed, for the first time ever, to reattain a 3.1% growth path. In fact, it has only managed a bit over 2%, and that has led to a potentially huge shortfall. The economy today is about $3.3 trillion smaller (in terms of total annual output) than it might otherwise have been. That's a lot of annual income that potentially has been left on the table.

This of course begs the question of why the economy has failed to thrive as it did in every other recovery in the past. Demographics (e.g., baby-boomers retiring) probably accounts for some of the shortfall, but I'm suspicious of that argument: why is it that over the course of a year or so (2008-9) there was a mass exodus of workers from the workforce? Demographics work over multiple years, not just one or two. Why is it that business investment has been weaker in the current expansion than it was in the 1990s? Could it have something to do with the fact that federal debt is now almost 80% of GDP? Could it have to do with the increasing burdens of taxes and regulations? Could it have something to do with the expansion of federal transfer payments (money taken from some people and given to others) from $2 trillion in late 2008 to now $3.1 trillion?

For years I've been blaming the shortfall in growth on Big Government (i.e., growing tax and regulatory burdens, anti-business climate, burgeoning entitlement programs), but it's a tough argument to prove. However, it's encouraging to see that growth has picked up since Trump arrived on the scene and began to reduce tax and regulatory burdens. Supply-side economics is being vindicated; the economy is responding positively to lower tax and regulatory burdens.

Chart #4

Chart #4 compares the burden of federal debt (debt owed to the public as a percent of GDP) to the level of 10-yr Treasury yields. A few things stand out. For one, more debt does not necessarily lead to higher interest rates. In fact, the relationship appears to be just the opposite: interest rates tend to rise as debt burdens fall, and vice versa. Second, beginning in late 2008 the burden of federal debt has surged to its highest level since the post-war period. Surely this must have had a dampening effect on economic activity, if for no other reason than the fact that the government spends money much less effectively and less efficiently than the private sector.

Chart #5

As Chart #5 shows, after-tax corporate profits also surged over the past decade, reaching record levels relative to GDP. Federal deficits have averaged about 5.3% of GDP for the past decade, while corporate profits have averaged about 9.4% of GDP over this same period. Corporate profits have been an important source of funds for the financial markets, but federal deficits have effectively consumed the equivalent of more than half of those profits. If the federal government had not borrowed so much, in part to fund a massive increase in transfer payments (which now consume almost three quarters of federal spending, up from 65% in mid-2008), the private sector would most likely have found more efficient uses for those funds and the economy would thus be stronger.

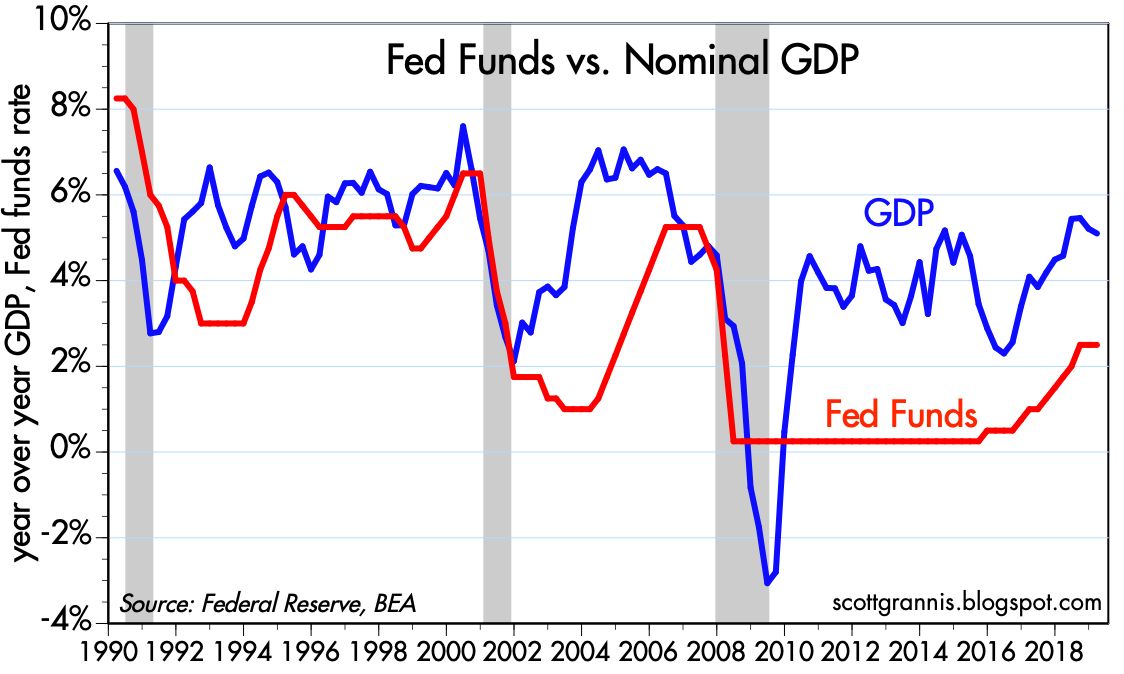

Chart #6

Some good news: Chart #6 compares the Fed funds target rate with the growth rate of nominal GDP. Recessions tend to follow periods in which the Fed pushes short-term interest rates up to and above the rate of nominal growth. That's otherwise called "tight money." It's similar to the flattening and inversion of the yield curve, which also typically precedes recessions (though as I pointed out recently, it also takes high real interest rates in combination with an inverted yield curve to do the trick). In short, it takes very tight monetary policy to kill the economy. Today, monetary policy is nowhere near tight.

Chart #7

Chart #7 shows 5-yr nominal and real yields, and the difference between the two (green line), which is the market's expectation for the average annual rate of inflation over the next 5 years. Here we see that inflation expectations are very much in line with historical experience, at just below 2%. We also see that there has been a pronounced decline in short-term interest rates this year: 5-yr real yields are in fact down about 70 bps from their high last December.

Chart #8

Chart #8 compares the trend growth rate of GDP with the level of 5-yr real yields. Real yields have a tendency to rise and fall in line with the economy's underlying strength. When the economy was booming in the late 1990s—growing an impressive 4-5% per year—real yields were trading in a range of 3-4%. By the mid-2010s, the economy was growing at a much more modest 2% rate, and real yields were around zero. Real yields picked up over the course of 2017 and 2018 as economic growth started to accelerate. So the 70 bps decline in real yields this year is the bond market's way of saying that the economy's growth rate is going to be on the decline for the foreseeable future, averaging perhaps 2 - 2.5% instead of the current 3%. Put another way, the bond market thinks the economy is going to be so weak that the Fed is going to have to cut interest rates. Inflation is not an issue, as Chart #7 shows; it's all about real growth and real yields.

If there's anything out of the ordinary here, it's interest rates, which appear too low given the fact that the economy appears to be picking up speed.