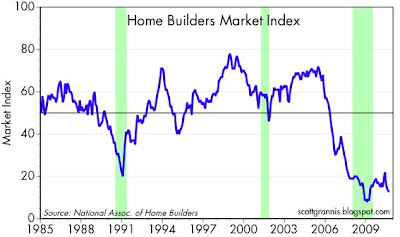

The National Association of Realtors reported today that existing home sales rose only marginally in August, leaving them at very depressed levels (third chart above). The National Association of Homebuilders' survey of market conditions was flat in August (first chart above) and remains at depressed levels. About the only thing positive to be gained from current news on housing is that the inventory of homes for sale (second chart above) has been relatively flat for the past year or so. This, despite the expected flood of foreclosed homes coming on the market. All of this is consistent with the relatively depressed levels of new applications for home mortgages, and with the very low level of mortgage interest rates.

Housing is still very weak. Residential construction has fallen to 2.5% of GDP, it's lowest level in recorded history. This is not new news—it's been making headlines for many months. Are conditions deteriorating even further? That is possible, judging from the drop in existing home sales in recent months. But the recent decline in sales may also be payback for the burst of sales late last year and earlier this year, both of which were propelled in large part by government subsidy programs. If that's the case, then the recent weakness is just an unintended consequence of government meddling in the markets. That's not surprising.

Whatever the case, housing is not contributing to the economy's strength. Growth has to come from other sectors, and without a housing rebound it's going to be tough to post impressive growth numbers for at least the next year. But we've known that for some time—this is not new news.

Are other sectors of the economy growing? Absolutely, yes. Industrial production is up significantly. Exports are up significantly. Tax collections are up (meaning incomes and profits are up). Commodity prices are rising across the board. Private sector jobs are up 1.8 million so far this year, according to the household survey of employment. Default rates are way down (suggesting much stronger than expected cash flows for most businesses). On balance, the weight of evidence continues to point to growth, albeit growth that is still quite short of the levels which we should be seeing if this were a normal recovery. The economy is fighting the headwinds of a massive expansion of government spending and regulations, and all the uncertainty surrounding a rapid buildup of debt. The future course and strength of these headwinds will be decided within the next few months by the electorate. I think the electorate is going to vote overwhelmingly for Change, and the change will be a positive for the economy.

1 comment:

The Fed has its ducks lined up to make this economy hum. Some quantitative easing, and we could get a real roaring recovery.

If real estate clicks, we will firing on all cylinders, with lot of gas in the tank (cash on sidelines) and zero inflation threat.

I agree with sentiments that Obama has been a poor leader economically--but jeez, we have been through that before and worse (like 2000-2008).

Maybe "gridlock" in DC will spur investor optimism. I have a feeling once something clicks, we get solid secular bull markets in property and equities.

The Fed is being far too timid, I guess emulating the Bank of Japan. What a role model.

Too tight money is like watching an anorexic friend fade away.

Ain't no inflation demons out there. Japan has had deflation for 20 years, come what may in commodities. It didn't matter.

So why is the Fed cowering in the corner?

Post a Comment