I'm now in Victoria Falls (Zimbabwe) and finally have some access to the internet (though quite slow). I picked up a cold somewhere out in the bush last week, so I stayed in the hotel this afternoon to catch up on the market rather than go out shopping with my wife. I'm still sorting through photos, and hope to post some interesting shots soon.

As I review the data of today and the past week or so, not much seems to have changed. (Indeed real changes only occur infrequently.) The economy is growing, but it is growing slowly and it is still about 10% below where it should be if it were to continue it's long-term trend growth of 3.1%, as shown in the chart above. It is this shortfall (aka the output gap) that is the source of the economy's still-high unemployment rate and the general sense of dissatisfaction and even anguish in some sectors of the economy.

The problem with this recovery is that it has been weak, much weaker than other recoveries following deep recessions such as the one we have just had. The Obama administration and Paul Krugman would have you believe that this weakness is due to a lack of fiscal stimulus (i.e., the trillion dollars of stimulus pumped into the economy so far has not been enough), but as I and most other supply-siders have argued for a long time, the economy's slow growth is most likely due to the fact that the fiscal stimulus that has been applied has been the wrong kind of stimulus. Instead of increased transfer payments and make-work projects we should have cut taxes; the way to help get the economy growing again is to make lasting changes to the incentive structure, in order to encourage people to work harder and corporations to invest in new plant and equipment and new ventures.

The Keynesian prescription for a stronger economy has once again failed, with the result that we have dug ourselves deeper into a debt pit and have very little to show for it. This should be the rallying cry for politicians to support efforts to keep the Bush tax cuts from expiring at the end of this year. Indeed, instead of allowing taxes to rise, we ought to at the very least cut corporate income taxes in order to encourage companies to invest the mountain of profits they have accumulated over the years. (Recall my oft-cited statistic that corporate profits have more than doubled since 1998, yet the S&P 500 hasn't risen at all over the intervening period.) Corporate profits after tax are now running at a $1.2 trillion annual rate, but they are effectively being used not to create new jobs but to fund the federal government's ineffective and wasteful spending. The way to speed up growth is simple: cut spending and cut taxes.

One thing that grabbed my attention in today's GDP numbers was the increase in the broadest measure of inflation, the GDP deflator. From a quarterly annualized low of -1.2% at the end of 2008, it has jumped up to 1.8%. This is a very important development because it directly contradicts established wisdom which holds that with a large output gap such as we have today, the economy should be experiencing deflationary pressures. On the contrary, inflation is now rising. I've been talking about this issue for almost two years now, warning that it is easy money, not a weak economy, that will drive inflation: easy money is now showing up as rising inflation (albeit still quite low from an historical perspective, but nevertheless definitely rising at a time when most Keynesian models would be forecasting deflation), even though the economy remains significantly below its long-term potential and there are plenty of idle resources out there. Thus, I see evidence in today's data that supports my rising inflation thesis.

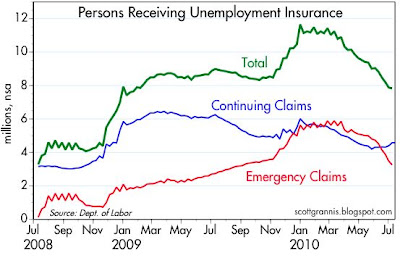

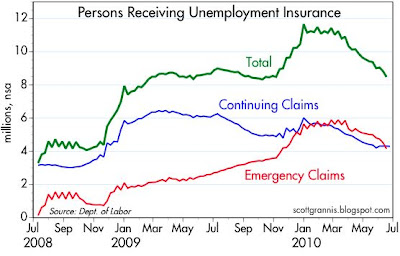

In other news, I see that the Chicago and Milwaukee purchasing managers' indices were both stronger than expected in July, and both remain at levels that strongly suggest continued economic growth. I also note that non-energy commodity prices (e.g. the JOC and the CRB Spot) have moved up in the past two weeks, and that bolsters my belief that the global economy continues to be healthy, and a healthy global economy in turn will help support the U.S. economy going forward. Importantly, I still no sign at all of the economy slipping into another recession or slowing down meaningfully.