What follows are updates of some of the more important charts—all based on market-driven prices—that I am following. These tell us what the market is thinking, as expressed in the prices of the dollar, gold, real and nominal interest rates, equity prices, volatility, swap and credit spreads, and commodity prices. As I read the charts, the market seems relatively unperturbed by all the turmoil, and hopeful that better times lie ahead. This in turn makes the market vulnerable to any shortfall vis a vis expectations, so now is one of those times to be cautiously optimistic rather than gung-ho.

If the US economy were a company, then the value of the dollar would be a good proxy for its relative attractiveness and its future prospects. The chart above shows two of the best measures of the dollar's value, on an inflation-adjusted, trade-weighted basis. By either measure, the dollar is moderately above its long-term average We can infer from this that the Fed has not printed more dollars than the world wants, though it might be guilty of supplying too few. On the other hand, it would appear that the dollar is one of the currencies in most demand, and that is encouraging since it means the US is attracting investment, and investment is the seed corn of future growth.

The chart above illustrates the tendency of commodity prices to move inversely to the value of the dollar (note that the dollar axis is inverted). In the past few years, however, both the dollar and commodity prices have moved higher. This is worthy of attention. I think it tells us that the rise in commodity prices has little or nothing to do with a monetary reflation (because a plentiful supply of dollars tends to boost the prices of most things (aka inflation), but rather more to do with a general strengthening of the global economy at a time when the US economy is expected to be one of the engines of stronger growth. Again, this is encouraging.

The chart above shows the very strong correlation between industrial commodity prices and emerging market equities. That makes sense, because emerging market economies tend to specialize in the production of raw materials. I believe the rise in commodity prices reflects a general strengthening of global economies, so what's good for commodities is good for just about everyone, especially emerging markets. And as I pointed out in December 2015, emerging markets and commodities had been severely beaten up and prospects for their recovery were bright.

For years I've been amazed at the correlation between gold and TIPS prices, as shown in the chart above (note I use the inverse of the real yield on TIPS as a proxy for their price). The common denominator of both markets is the way they serve to protect people from risk. TIPS are a good hedge for inflation, they are default-free, and they are the only asset that guarantees investors a real rate of return if held to maturity. Gold, on the other hand, is a classic port in a storm for just about anything that makes people nervous about fiat currencies or government excesses. Gold and TIPS have been in a rough holding pattern for the past several years. Declines in gold and TIPS would likely coincide with improvements in the global economic outlook. That they have not yet fallen meaningfully is therefore a good sign that markets are still somewhat risk averse and less than optimistic.

It's almost always the case that stocks tend to weaken as fears tend to rise, as shown in the chart above. But the current level of fear and uncertainty (as reflected in the ratio of the Vix index to the 10-yr Treasury yield) is still quite modest compared to what we've seen in recent years. The Trump era seems to have brought with it a calming effect on global markets.

Swap spreads are some of the best coincident and leading indicators of financial market and economic health. Spreads have been rising for the past year or so both in the US and in the eurozone, so that could be a sign of deteriorating economic and financial fundamentals. I've tended to dismiss the current rise in US swap spreads, however, because they are still within what we consider to be a "normal" range (20-35 bps); if anything, they were exceedingly low at the end of 2015 and only now have recovered to more normal levels. Eurozone swap spreads have moved substantially higher, however, and that is cause for concern. My guess is that eurozone swap spreads are elevated because of concerns that France could pull a "Frexit," and this could undermine the stability of the euro and the eurozone economy. This risk is not trivial, and is not one to dismiss lightly—unless you believe (as I do) that the demise of the eurozone would not be necessarily a bad thing. For the moment, I note that credit default spreads on French debt are declining (i.e., the market is worrying less about a Frexit since the political left seems to be ascendant for the moment), but this still bears watching.

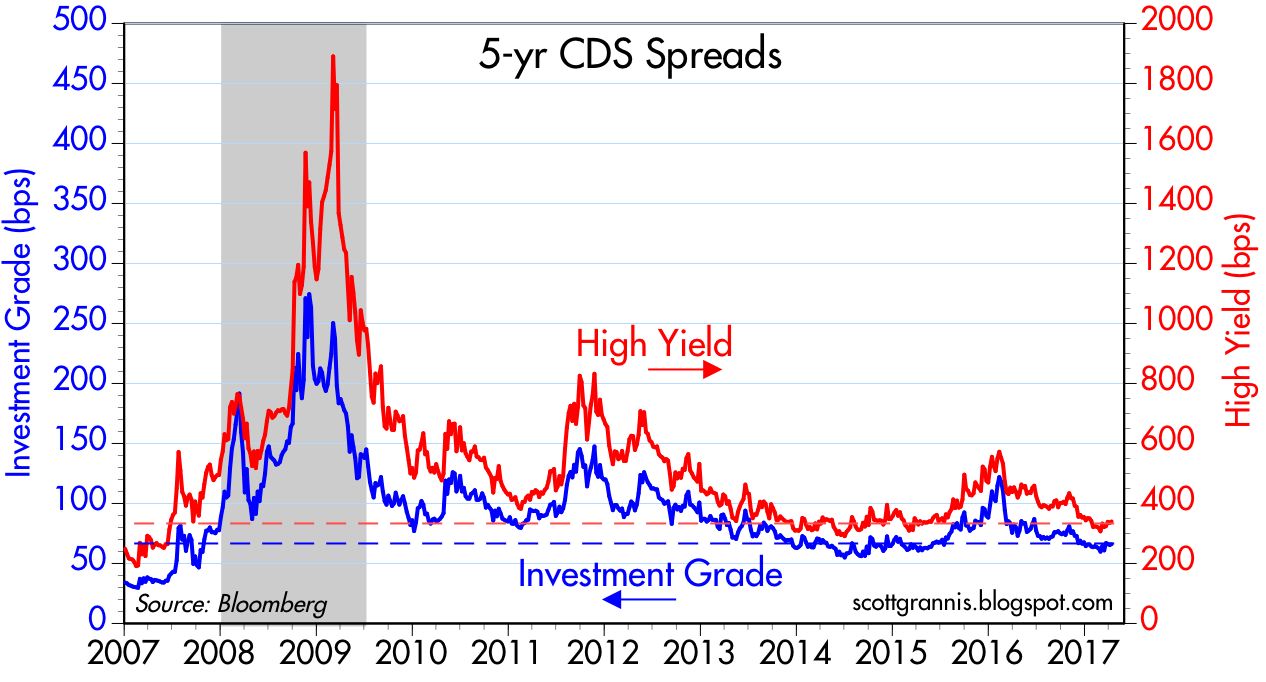

Speaking of credit default spreads, the chart above shows that they are relatively low here in the U.S., and that further suggests that systemic risks are low and markets are relatively confident about the future.

One persistent and salient feature of the past 6-7 years has been Treasury yields in the US that are very low relative to inflation, as the chart above shows. Some observers dismiss this with the argument that the Fed is keeping interest rates artificially low, but I'm not a buyer of that line of thinking. I think Treasury yields are very low because markets still have a palpable degree of risk aversion, and are thus willing to pay a lot for the protection of Treasuries. We see this same phenomenon all over the developed world: sovereign yields are unusually low. Most investors have a choice between holding Treasuries and holding riskier assets; that the price of Treasuries is unusually high relative to other assets (e.g., the earnings yield on the S&P 500 is substantially higher than the yield on 10-yr Treasuries) must therefore mean that investors are very distrustful of the outlook for the economy and for corporate profits. In other words, very low Treasury yields are a strong and reliable indicator of a market that is less than optimistic, to say the least. Show me an optimistic/enthusiastic market, and I'll show you nominal Treasury yields that are much higher than they are today.

The difference between nominal and real yields is a measure of the market's inflation expectations. In the chart above we see that inflation expectations over the next 5 years (the green line) are 2%, and not surprisingly, that is what the CPI has averaged over the past few decades. Markets are not concerned about rising or falling inflation right now; it's steady as she goes. Kudos to the Fed for having managed monetary policy surprisingly well over the years.

The chart above is my attempt to show that the level of real yields on TIPS can and does tell us a lot about the market's expectations for real economic growth. Real growth has averaged about 2% during the current expansion, and 5-yr TIPS yields have averaged about zero. You can invest in the economy and expect to get an average real return of 2%, or you can invest in TIPS and earn a guaranteed zero real rate of return. Guaranteed real rates of return should always be less than expected real rates of return, should they not?. If and when TIPS yields rise significantly, this will be a good indicator that the market is expecting economic growth to accelerate. For now, it may be the case that the market is buoyed by Trump expectations, but to judge from TIPS yields, there is little or no evidence of much optimism.

The chart above shows the 6- and 12-month growth rates of private sector jobs in the US. If anything, jobs growth has slowed over the past few years, from just over 2% to currently about 1.7%. The manufacturing sector looks to be picking up, but the overall economy remains on a sluggish growth trend that of late has been declining modestly on the margin. No sign here of a Trump bump, and it's premature to expect one: we need to see meaningful tax and regulatory reform (or solid reasons to expect such) before getting excited.

25 comments:

Great wrap-up by Scott Grannis.

Some stray thoughts:

Why "low" interest rates, which seem to be the new normal?

Well, supply and demand. There is a huge supply of capital, some artificial, such as sovereign wealth funds, and public pension plans. Insurance that is required by law or contract, and premiums are invested. Then there is the emerging middle classes globally, able to save for the first time in history. Of course, billionaires are being minted daily in the Far East.

There is still a generation of American savers who feel they are "entitled to a return on their savings." This may be a throwback to the fixed-rates on passbook accounts, set by the government and FDIC insured. I think my first passbook account, set up back in the late 1960s, paid 4.5%.

Unfortunately, your savings are becoming less valuable. You are also entitled to a loss on your savings, in free markets.

Low interest rates may be the new normal, or at least normal long enough for those of us with limited investing years ahead.

The Fed may try to artificially raise rates, and I think it is now, through its reverse repo program. I can't imagine this will work. Can the economy be choked into higher interest rates? Maybe rates can go up 100 basis points, without sorry results. We will see.

But as soon as the Fed cuts into the property markets, the rest will follow.

True, China is doing better. Europe slightly better. Maybe they can pull the global economy along,

The Fed appears reckless to me. Why are they raising rates? Is growth too hot---at 2%? This is hot?

Is inflation threatening to run away---at 1.7% by their preferred index, the PCE? This is hot?

The Fed's Labor Market Conditions Index is getting softer. Wages are way under control. Property is appreciating, but that is tied to property zoning, not general demand.

The Fed may also begin to liquidate its balance sheet, but why I do not know. That may constrain the supply of capital (and artificially raise rates), but it will not increase demand.

Interesting times.

I think the Fed is very mindful of the market's reactions to both its moves and its intentions. If the market starts to react negatively to the Fed's intention to move, I wouldn't be surprised at all to see the Fed back off. The Fed is a follower, not a leader, in this game. The Fed takes its cues from the market and the watches to see how the market reacts. It's a give and take thing.

In thinking about TIPS, the author wrote: "they are the only asset that guarantees investors a real rate of return if held to maturity." The investor is likely to have a capital gain in a TIPS investment at maturity. That gain is subject to capital gains taxes even though the gain is not real. The TIPS investor has not experienced any increase in purchasing power but must pay tax on these phantom gains. I find TIPS unattractive. YMMV

Re capital gains taxes on TIPS held to maturity. TIPS bonds are unique because their principal is adjusted over time by the amount of inflation. For example: suppose that today I buy a newly issued 5-yr TIPS bond for $1000 that carries a 1% real yield. Suppose also that inflation is 2% per year for the life of the bond. Every year the principal value of my bond increases by 2%, and I am paid a coupon equal to 1% of the inflation-adjusted principal of the bond each year in semi-annual installments. At maturity, the bond's principal value would be equal to 1000*(1.02)^5 = $1040.81. The 2% annual increase in the principal value of the bond is considered to be taxable income, as is the coupon payment of 1% of the inflation-adjusted principal. That is similar to the treatment of any bond which pays a nominal rate of interest, part of which (the part in excess of inflation) is considered to be a real rate of interest.

If held in a taxable account, the full nominal rate of interest received by the holder of TIPS (the coupon payment plus the inflation adjustment) is taxable, just as would be the coupon payment of any bond held in a taxable account. The tax can be avoided by holding TIPS—or any bonds, for that matter—in tax-exempt accounts such as IRAs, or it can be minimized by holding TIPS in the form of mutual funds or ETFs. TIPS held in a Roth IRA (which is never subject to tax) would pay a government guaranteed real yield equal to their coupon yield at purchase, in addition to the adjustment for inflation.

Your point is noted, since it is important to clarify that the effective real or nominal yield that an investor receives on TIPS or any bond is a significant function of whether the bond is held in a taxable or non-taxable account.

I liked the observation about emerging markets and commodities. The asset allocation diversification crowd sometimes simplifies things in buckets of US, Developed Intl (read Japan and Europe), and Emerging Markets. To me, the emerging market index IS primarily commodities. Not sure I make a good commodities trader.

The captcha stuff seems hard to me too.

Hi Scott,

I am a bit surprised that you do not at all comment on credit growth since it shows quite a down-turn lately. The development is quite similar to what happened before our more recent recessions. You don't think that credit growth has anything interesting to say about what the market thinks about the future?

Also, considering an extension of slower credit growth should we not expect slower money supply as well (especially if Fed holds true to its ambition to slowly size down its balance sheet)? And if so, would that be something to keep an eye on, or do you think that growth in money supply is irrelevant? (There are still plenty of excess reserves, but they do no good if the don't find their way into the markets do they?)

Cheers,

fred

I am never truly surprised at what markets do. They are capricious. Own that. Many have been expecting bond yields to back up significantly but voila! Here we are with the 10 yr at 2.24%. I agree with Benjamin that much of that is supply and demand. There is a LOT of $ out there looking for a home and as the baby boomers get older they become more risk averse. Even though stocks are up nicely over the past 12 mos there has been a net OUT flow of $ from stock funds and a large net IN flow to bond funds.

OF course the pundits are saying that bond holders are going to get hammered and maybe they will. But how long have we been hearing the same song from these so called experts? There are NO experts when it comes to market prognostication. IF the fed continues to raise short rates and that is a BIG if-I do not understand why that has to bad for bonds. Short rates do not govern long rates and higher borrowing costs is a drag on the economy which paradoxically is good for bonds.

Teresa, re credit growth: this has not escaped my attention, as I noted in a comment to the post preceding this one. For the moment I do not have any insights worth sharing beyond my aforementioned comment.

CPI delation in March.

Shelter costs moderating.

Could be nothing or canary in coal mine.

SEMPRE SBORRATISSIMA NEL CULO: ELISA COGNO (FRUIMEX BLOGSPOT-TORINO-ALBA). PUTTANA SATA-N-AZISTA CHE DIFFAMA SUL WEB A FINI KILLER! SEMPRE A FARE ORGE AD HARCORE-ARCORE DA STRAGISTA SPAPPOLA MAGISTRATI E NOTO PEDOFILO SILVIO BERLUSCONI! LAVA CASH MAFIOSO!!

1

SEMPRE SCOPATA E SBORRATA NEL CULO: ELISA COGNO (FRUIMEX SAS DI ALBA E TORINO.. NOTA ANCHE COME ESTREMAMENTE CRIMINALE "FRUIMEX.BLOGSPOT.COM")! DA CRIMINALISSIMA PUTTANONA BERLUSCONAZISTA E PADANAZISTA QUALE E', LAVA TANTISSIMO CASH DI COSA NOSTRA, CAMORRA E NDRANGHETA, COME PURE RUBATO O FRUTTO DI MEGA MAZZETTE DI LL, LEGA LADRONA, ED EX PDL, POPOLO DI LADRONI ( ORA FORZA ITALIA MAFIOSA). IL TUTTO INSIEME A SUA MADRE, NOTA BAGASCIA SEMPRE PIENA DI SIFILIDE, CRIMINALISSIMA PUTTANA PIERA CLERICO (ANCHE LEI MEGA RICICLANTE SOLDI ASSASSINI, PRESSO MALAVITOSISSIMA FRUIMEX FRU.IM.EX SAS VIA NICOLA FABRIZI 44 10145 TORINO E LOCALITA' SAN CASSIANO 15 - 12051 - ALBA - CN). IL TUTTO IN INFIMA HITLERIANA CONGIUNZIONE CON PROPRIO, FILO MAFIOSO FRATELLO PAOLO COGNO: NOTO PEDERASTA NAZISTA, SUPER LAVA EURO KILLER, VICINISSIMO A FAMOSO " NDRANGHETISTA PADANO" DOMENICO BELFIORE DI TORINO E GIOIOSA JONICA. SON TUTTI SATANISTI, ANZI, SATA-N-AZISTI, CHE HAN INDOTTO AL SUICIDIO ( E SPESSO HANNO "SUICIDATO", OSSIA HANNO AMMAZZATO AND THAT'S IT) TANTISSIME PERSONE. FRA CUI 5 RAGAZZI QUI http://www.ilfattoquotidiano.it/2013/05/29/piemonte-5-ragazzi-suicidi-in-sette-anni-pm-indagano-sullombra-delle-sette-sataniche/608837/

http://www.targatocn.it/2013/05/27/leggi-notizia/argomenti/cronaca-1/articolo/satanismo-dietro-a-5-suicidi-di-studenti-saluzzo-potrebbe-scoprirsi-quella-che-non-sapeva-desser.html

E CHE PARTECIPAVANO AD ORGE DEMONIACHE, QUI

http://www.direttanews.it/2017/03/15/meraglia-orge-sataniche-torino/

CON SATA-N-AZISTE PIERA CLERICO ED ELISA COGNO, ZOCCOLONE MADRE E FIGLIA, CHE PARTECIPAVANO ALLA STESSA ORGIA E LESBICAVANO ALLA STESSA ORGIA. MADRE E FIGLIA, CHE SCHIFO ( D'ALTRONDE, FURONO CENTINAIA E CENTINAIA LE VOLTE CHE LE MEGA MGNOTTE ELISA COGNO E PIERA CLERICO DELLA CRIMINALISSIMA FRUIMEX DI ALBA E TORINO, PARTECIPARANO AD ORGE AD HARCORE-ARCORE, E DI CERTO NON SOLO, DAI PEDOFILI, STRAGISTI SPAPPOLA MAGISTRATI, SEMPRE SODOMIZZATI PAOLO E SILVIO BERLUSCONI

http://www.secoloditalia.it/2015/07/glielo-misi-in-quel-posto-triste-scoop-travaglio-stile-youporn-berlusconi-sodomizzato/

http://www.vnews24.it/2015/07/03/ruby-orgia-berlusconi/

http://www.ansa.it/puglia/notizie/2014/11/27/daddario-ho-sempre-detto-verita_6ba94260-f3d9-48f4-a264-941f7a4a2d9b.html )

LA CRIMINALISSIMA FAMIGLIA COGNO PUO' INTERAMENTE FINIRE IN GALERA DA UN MOMENTO ALL'ALTRO, HANNO PM DI SEI PROCURE PIEMONTESI ADDOSSO. SPERIAMO CHE CI FINISCANO IN CARCERE E SUBITON O FARANNO UCCIDERE DECINE E DECINE DI ALTRE PERSONE. DI QUESTO GRUPPO MAFIOSAMENTE E "SATA-N-AZISTAMENTE" ASSASSINO, FANNO OVVIAMENTE PARTE, PURE, IL GIA' PLURI CONDANNATO AL CARCERE, ACCLARATO PEDOFILO E FREQUENTISSIMO MANDANTE DI OMICIDI, PAOLO BARRAI!

2

IL GIA' 3 VOLTE IN GALERA PAOLO BARRAI DI MEGA RICICLA SOLDI MAFIOSI, CRIMINALISSIMA BLOCKCHAIN INVEST O CRIMINALISSIMA BLOCKCHAININVEST CHE SIA, COME DI CRIMINALISSIMA WMO SA PANAMA, CRIMINALISSIMA WMO SAGL LUGANO, CRIMINALISSIMA WORLD MAN OPPORTUNITIES LUGANO E CRIMINALISSIMA BSI ITALIA SRL DI VIA SOCRATE 26 MILANO, OLTRE CHE DI MEGA TRUFFATORE BLOG MERCATO LIBERO, NOTO IN TUTTO IL MONDO, COME "MERDATO" LIBERO. INSIEME AD UN ALTRETTANTO PEDOFILO KILLER, SEMPRE A BANGKOK A STUPRARE ED UCCIDERE BAMBINI , COME A LAVARE CASH SUPER MAFIOSO DI ROBERTO PALAZZOLO, VERME BASTARDAMENTE SANGUINARIO MAURIZIO BARBERO DI TECHNO SKY MONTE SETTEPANI E MERCATO LIBERO NEWS ALIAS "MERDATO" LIBERO NEWS( ALTRO ASSASSINO SATA-NAZ-ISTA DI ALBA). DEL GRUPPO OMICIDA FA STRA PARTE, PURE, IL NOTO PEDERASTA CHE INVOCA LA PEDOFILIA LIBERA, L'INCULA BAMBINI STEFANO BASSI DI TORINO E DE IL GRANDE BLUFF. ED IL COLLETTO LERCIO, MEGA RICICLA SOLDI CRIMINALISSIMI A ROMA (GIRI SCHIFOSISSIMI DI MAFIA CAPITALE E DELLA EX BANDA DELLA MAGLIANA), NONCHE' SEMPRE CANNANTE IN BORSA, MEGA AZZERA RISPARMI FEDERICO IZZI, NOTO COME " ER ZIO ROMOLO CHE TE FA' PERDE TUTTO QUELLO CHE HAI E TE LASCIA EN MUTANDE" ( SE VI E' UN PO' DI IRONIA, ANZI, PICCOLA SDRAMMATIZZAZIONE, IN QUESTA PARTE FINALE DEL TESTO, VI ASSICURO CHE IL RESTO E' TUTTO VERISSIMO E SERISSIMO)!

Single-payer would actually be pro-growth, because it would enable entrepreneurs to start businesses and not worry about healthcare, and it would give ordinary workers economic mobility to change jobs or re-train with an important safety net. Finally, it would relieve corporations of major financial burdens, and make them even more competitive against foreign competitors.

And if you examine the polls in the political landscape, Trump's base supporters want it. A

The percentage of US GDP going into health care is insane! Single payer is required to get it down to levels akin to other developed nations. Huge win if can do - say dropping the cost from 18 pct GDP to 11 pct GDP. That leaves a lot of money to put into productive investments. I think there's no other choice. Infrastructure currently exists with expansion of Medicaid which is already handling 20% of Americans.

I've been listening to the argument for single payer ad nauseam-and it's a good one. That said it will NEVER happen in the USA. Would require a complete dismantle of the private health care system and subsequent rebuild by the federal govt. Seriously?

Single-payer healthcare is a guaranteed disaster. It would inevitably result in higher costs and poorer service (e.g., waiting lists). It's socialism in disguise, and socialism can never beat the results that free market capitalism can.

To understand this, imagine what would happen if grocery stores became single-payer. If the government paid for everyone's food, what do you think would happen to the quality of food, the variety of choices, the supplies of food, and the service you would expect to find at your neighborhood market? All would deteriorate.

Here's the difference, as I see it. Beyond a very minimal subsistence level, people can decide whether or not to buy food, what kind, how much, etc., and they can buy some food very very cheaply.

The same is not true of health care. First, some people are unhealthy, or are more prone to being unhealthy, for genetic reasons.

Republican Patrick McHenry:

Rep. Patrick McHenry (R-NC), the chief deputy majority whip in the House, told reporters Wednesday that a new proposal that would weaken protections for people with pre-existing conditions is “a bridge too far for our members.”

...

“I was once in the individual market, for a period of time in my 20s, and my family’s medical history is really bad,” he said. “So my understanding of the impact of insurance regulations is real. I believe I’m a conservative, but I remember the really bad practices in the insurance marketplace prior to the ACA passing."

Second, the line between being sick and being healthy can change in an instant no matter what one's genetics are via factors that are outside of our control.

And as a result of increasing technology, healthcare has gotten so expensive that only the very very rich can self-insure.

These factors negate the operation of the free market.

As a result, people need protection that only an entity like the government can offer.

I believe single-payer can do this more efficiently than Obamacare.

Rich: the plight of the disadvantaged and the unfortunate is a legitimate concern which no one can ignore. But to transform the entire healthcare market into single-payer because of the problems of a relatively small percentage of the population is hardly sensible. Better to rely on private charity and something like a voucher, where direct aid is handed out and the spending decisions are left to individuals (similar to the healthcare savings accounts which have been very successful).

The only way to bring healthcare costs down while also improving the quality and the accessibility of healthcare is to move as close to a free market as possible. Individuals must be the ones controlling how their money is spent, not the government or the insurance industry.

I recently heard a local Republican leader here in Pennsylvania making the point that healthcare and tax reforms may have to be delayed until Trump's (or his successor's) next term. What I read into the statement is that ultra-conservative Republicans would rather put off healthcare reform and tax reform to avoid any compromises. This person said that the goal of Republicans "must be" to repeal Obamacare, Medicare, and Social Security "once and for all." His position on taxes was that corporate tax reductions should be handled separate from individual tax reforms. Just wondering if readers here share those views?

Love these graphs. Especially the swap spreads. We'll have to keep a close eye on the euro spreads.

The perfect federal social health program to test voucherization on is…the VA.

The VA is federal hospitals on federal land, staffed by federal employee doctors, nurses and administrators, for the benefit of former federal employees, all no co-pay and all financed by income taxes levied productive citizens. The VA medical program is distilled communism.

The GOP (which now controls all three branches of the federal government) could put vets on vouchers, shut down the VA medical system, and we could see the results in the real world, better or not.

I join Scott Grannis is in calling for voucherization of federal medical programs.

What about Treasury yields -- should investors ignore this measure?

https://www.wsj.com/articles/flatter-yield-curve-in-2017-shows-growth-concern-lingers-1491048017

The flattening of the yield curve in the past month or two is one of many signs that investors are losing confidence in Trump's ability to pass meaningful tax reform, and that the economy is somewhat weaker than investors were hoping. Stocks are down on the margin, the dollar is weaker on the margin, and gold is up. In other words, the "reflation trade" has been partially unwound.

Benj,

Sorry, my friend, the Republican Congressmen cannot even tie their shoes. What a pathetic group of grumbling incompetent near-do-wells. I'll be really impressed if DT gets half his agenda passed, and I hope he gets all of it. I am for ramping up economic growth in the USA.

Benj

Its time to test the economy and that means the fed is going to have to raise rates. Time for home speculation and market speculation to be reigned in. The housing market is 40% overpriced and these specs need to feel some pain.

lets see the real economy not the fake fed economy.

roll the dice

Post a Comment