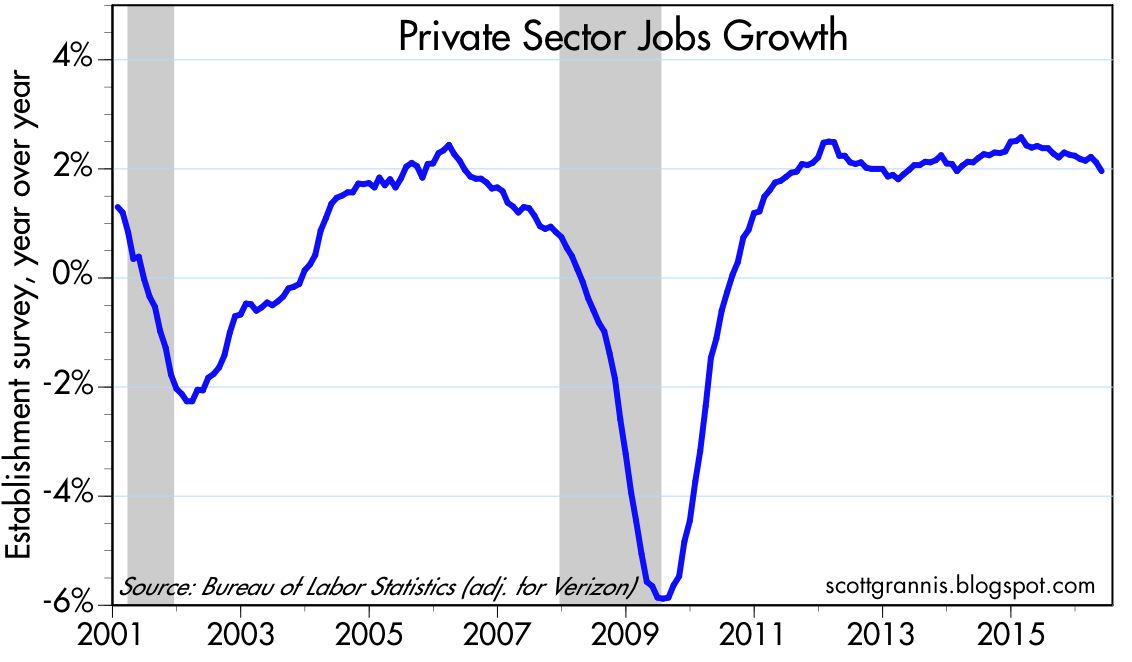

The June employment report was much weaker than expected (+38K vs. +160K), but it's not necessarily the case that the engine of economic growth has virtually shut down. We've seen a half dozen very weak numbers like this over the past 5-6 years—it's the nature of this beast to be very volatile on a month-to-month basis. The monthly payroll numbers are simply not reliable enough to make confident judgments about the health of the economy, and, moreover, they can be revised significantly in the future.

What the report does tell us is that there is no sign of any fundamental improvement in the economy or the jobs market. There had been hints of improvement in past reports (e.g., a rise in the labor force participation rate and a quickening in the growth of the labor force), but they've been largely reversed now. As a result, it's likely that the economy is still plodding along at a miserably slow pace and will continue to do so unless and until there is a meaningful change to fiscal policy.

The Fed will find it hard to raise rates given the lack of any fundamental improvement in the jobs market, but the market fully understands this and rates are priced accordingly (no rate hikes expected for at least a few months, 10-yr yields at 1.7%, very close to their all-time low of 1.4% which was registered in July '12). Inflation expectations remain subdued (at around 1.5%), notwithstanding today's jump in gold prices and drop in the dollar. Meanwhile, liquidity is abundant (2-yr swap spreads are still very low) and the market exhibits little or no sign of any systemic stress. All eyes remain glued to the presidential elections for clues to the future, few of which have been forthcoming to date.

One reason to suspect that the June numbers were artificially low—and thus likely to be reversed in coming months—is the ADP report for June, which estimated private sector job growth to be 173K. These two series have tracked each other pretty well over the years, with the BLS series typically much more volatile. If the past is any guide, we'll see surprisingly strong jobs growth in the BLS numbers in coming months.

16 comments:

The US economy has grown tepidly since 2000, with two recessions, the 2008 being a doozy.

But is this a matter of U.S. fiscal policy? The global economy has been on much the same track, with the exception of mainland China, and even there is growth is slowing to 5-6% range.

In addition, there are abundant state and local impediments to growth, from minimum wage laws, to extensive and stipulative NIMBYism and no-grwoth property zoning, from Newport Beach to Santa Monica to Boston.

It may be with the NIMBYism, the US is more hostile to development, including business development, than ever before. We make it impossible for people to live where they want, near work.

As I have stated before, Newport Beach could become Las Vegas-Miami Beach on steroids, if they would go to no property zoning at all, and legalize gambling (get a pass from state law). But the residents of Newport Beach do not want development or business growth. In a sense, they are very anti-business. The residents of Newport Beach are not outliers, but I would say in the new norm of Americans.

On the other hand, in the 1960s, the top tax rate was 90%, the labor force was heavily unionized, and banking, transportation and telecommunications were much more regulated than today. The economy boomed! Property zoning was less stimulative, though. Monetary policy was more pro-grwoth.

There is a constant through much of this, and that is the growing "central bankers movement." The Bank of International Settlements, and a growing conviction (to the point of dogma) among central bankers that they should be independent, and should target very low rates of inflation, or even no inflation. Any rate of inflation above 2% is considered blasphemous.

The US, btw, flourished from 1982 to 2007, with average real growth just north and inflation just south of 3%. That's a 25-yeat stretch in real, recent history, not a theory.

Today we have un-transparent central bank in Europe, the ECB, totally insulted from democratic accountability. Growth is dead. Yes, they regulate and tax everything too, and that plays a role.

Central banks in Japan and the US have a dash of more accountability, and perhaps better growth.

I am not calling for inflation in double digits, or even in high single digits.

Would a 3% inflation rate kill anyone?

In addition, there is a growing and welcome movement in the hard-core right=wing that espouses that central banks should embrace nominal GDP targeting, not inflation-targeting. Scott Sumner and David Beckworth, both "Market Monetarists" are now (or soon will be) employed at the libertarian-ish Mercatus Center at George Mason University in Virginia, the right-wing redoubt.

We can hope the "money everywhere should always be tighter" wing of the GOP will soon fade away. The Dems are clueless too btw.

Personally, I would like to see a 10-year moratorium on all property zoning, and an aggressive, pro-growth monetary policy.

I like prosperity.

Main Street USA is in a tailspin -- I see no path to a Main Street recovery that does not entail revolution -- the battle lines between Main Street and Federalism have not been worse since the US Civil War -- the establishment folks from both parties will likely win the day -- but at what cost?

PS; The abandonment of Main Street USA is akin to the abandonment of the American Indians -- the damage to the USA will be incalculable -- the price of maintaining the establishment will be dire...

PPS: Main Street USA remains mired in economic depression as evidenced by long-term declines in real working wages, real home values, and the employment to population ratio.

SCOTT, you have argued for years that the Federal Reserve is not "printing money"; it's simply meeting a great demand for cash in saving accounts. And I accept your argument. Still the Federal Reserve says that it wants to encourage inflation to rise to their magical 2%.

It seems to be common wisdom that a central bank's "printing money" causes inflation. As examples, Argentina and Brazil have rising inflation which is said be to due to actions of their central banks.

So my question is: why doesn't the Federal Reserve go ahead and "print money" to raise the US inflation rate to 2%?? And what would "printing money" look like? What would the Federal Reserve need to do to "print money"?

I'm puzzled by this issue. Thank you

http://www.marketwatch.com/story/how-stock-buybacks-have-become-wall-streets-new-drug-2015-07-17

Those that think stock buybacks have not played a significant role

are badly informed.

This has become the drug of choice for all too many COE, with the

COMPLETE approval from their cowardly board of directors; mutual fund

owners and shareholders as well.

The high level of "free" stock awards to the corporate elites plays

a major role in this form of shareholders abuse and reduced returns.

Today's COE want to become multi-millionaires or more. Greed has replaced

pride and accomplishment.

I will add, even Head Start graduates know, that stock buybacks at near highs

are a poor deployment of capital.

Dr McKibbin, real estate prices are 17% short of their record

highs.

Williams says the following: "SCOTT, you have argued for years that the Federal Reserve is not "printing money"; it's simply meeting a great demand for cash in saving accounts. And I accept your argument."

https://www.federalreserve.gov/aboutthefed/section16.htm

"1. Issuance of Federal Reserve notes; nature of obligation; where redeemable

Federal reserve notes, to be issued at the discretion of the Board of Governors of the Federal Reserve System for the purpose of making advances to Federal reserve banks through the Federal reserve agents as hereinafter set forth and for no other purpose, are hereby authorized. The said notes shall be obligations of the United States and shall be receivable by all national and member banks and Federal reserve banks and for all taxes, customs, and other public dues. They shall be redeemed in lawful money on demand at the Treasury Department of the United States, in the city of Washington, District of Columbia, or at any Federal Reserve bank."

[12 USC 411. As amended by act of Jan. 30, 1934 (48 Stat. 337). For redemption of Federal reserve notes whose bank of issue cannot be identified, see act of June 13, 1933.]

So Williams, if the Central Banks does not print, then the only one

that does are the commercial bankers.

Re "why doesn't the Fed go ahead and print money?"

The Fed is limited in what it can do. It's most basic function is to buy government debt and issue "bank reserves" in exchange. These reserves can then be used by the banking system to support money issuance. Banks are the only ones who can "print money" since they can make a loan to someone just by creating a deposit, as long as they have enough reserves to support a larger deposit base. (In our fractional reserve banking system, banks have to have roughly 1 dollar of reserves for every dollar of deposits.)

Prior to 2008, bank reserves paid no interest, yet banks had to hold them to collateralize their deposits. Naturally, the banks tried to minimize their holdings of reserves. Now, however, bank reserves do pay interest, so banks don't mind holding them, as long as the interest they pay is, on a risk-adjusted basis, competitive with the interest they can earn on making loans.

For years now the Fed has undertaken to expand massively the amount of bank reserves, but the banks have not similarly expanded their lending activities. So the amount of money in the system hasn't grown enormously. Given the fact that inflation has been low and stable, we can assume that somehow the Fed and the banks did the right thing: the Fed gave the banks plenty of leeway to print money but in the end they printed just as much as the world wanted. When money supply and demand are in balance, inflation should be very low or nonexistent.

As I've explained many times, QE was not really an attempt to print money, or to encourage banks to print money. It was about transmogrifying notes and bonds into T-bill substitutes. Bank reserves function just like T-bills: they carry a floating interest rate, and they are default-free. Bank have been under enormous pressure (thanks to Dodd-Frank) to become much more solid, to clean up their balance sheet. Holding more bank reserves accomplishes that. Banks' demand for risk-free, interest-bearing assets was intense, and there weren't enough T-bills to go around, so the Fed fixed that with QE; it gave the banks what they wanted.

So far, the banking system seems to be happy with all their reserves. But should that change, then we could see inflation or deflation consequences. If banks decide they would prefer to make loans rather than hold trillions of excess reserves, then we could see "money printing" that would exceed the world's demand for money. In other words, if banks' demand for money (in the form of bank reserves) should decline, then money will become in excess supply and that will support higher inflation. If the public's demand for money should decline, the same result should apply. Strong money demand to date has been a function of risk aversion; weaker money demand would follow from a decline in risk aversion and a rise in confidence.

That's why I've been arguing that the Fed's worst nightmare is a rise in confidence. Rising confidence would oblige the Fed to take offsetting action to either reduce the supply of bank reserves and/or increase the demand for those reserves by increasing the interest rate they pay. Will they be able to do this in a timely fashion and by just the right amount? Who knows? We've never been down this road before.

One way the Fed might force higher inflation is to suddenly declare that bank reserves no longer pay interest. That would leave banks with trillions of assets that suddenly become less attractive to hold. Banks would presumably choose to increase their lending in order to hold more interest-bearing assets (i.e., loans) and that could fuel an over-supply of money and higher inflation.

Thank you very much Scott.

Scot, what are your views about the UK's impending referendum on staying in or leaving the EU ? I assume since you hate big government and all of its strangulating red tape and inefficiency, not to mention the EU's shockingly undemocratic and unaccountable Brussels headquarters, that you would be a strong proponent of "Brexit". Thanks in advance for your thoughts.

Rob, re "Brexit." You are correct, I don't think the EU is necessary or beneficial. The UK would probably be better off leaving. Just knowing that UK Labour Party leader Jeremy Corbyn is in favor of remaining in the EU is reason enough to favor Brexit. George Will elaborates:

https://www.washingtonpost.com/opinions/britain-too-is-infected-with-political-silliness/2016/06/03/77560a20-28e8-11e6-b989-4e5479715b54_story.html

scott, on this business of the prolonged cycle of low rates: If average, unsophisticated savers/investors cant get a spendable return on fixed income assets, is the negative effect of not having that spending in the economy quantifiable? If it is quantifiable, is it a figure that could at least partially explain the abnormally slow economic growth of several years?

Brian Wesbury has a nice take on the Brexit issue here:

http://www.ftportfolios.com/Commentary/EconomicResearch/2016/6/6/brexit-is-freedom

steve, re low rates: This is a chicken/egg question. Are low rates causing slow growth, or is slow growth causing low rates? I'm in the latter camp. The economy is facing serious headwinds which have depressed growth: high tax rates, a tax code riddled with preferences, huge regulatory burdens, and a general anti-business climate emanating from the White House. This raises the bar for investments and many companies and individuals are discouraged from investing. So the demand for investment capital is low and that is depressing growth and keeping rates low.

Besides, consumer spending, even that which is fueled by fixed income investments, is not what creates growth. Growth requires investing in something that enhances the productivity of the economy, and that in turn requires risk and hard work.

scott, i must disagree. at a very basic level consumer spending impacts all revenues (tax receipts, corporate, sales, etc.) Overall, corporate revenues have declined steadily. I maintain that the pool of fixed income interest money "normally" spent (but not this time) in the business cycle is sorely missed. can it be quantified? You rightly say that growth requires investment. But appetite for investment is inhibited when the revenue is not there to justify that investment.

As a result, it's likely that the economy is still plodding along at a miserably slow pace and will continue to do so unless and until there is a meaningful change to fiscal policy. resume service chicago

Post a Comment