For the past several years the economy has been disappointingly weak (the weakest recovery ever), and the stock market has periodically worried that things would get worse. The one reassuring constant in recent years has been 2-yr swap spreads, which have been low and relatively stable, thus casting doubt on the validity of the market's concerns. Nothing much has changed of late.

The chart above shows how peaks in the market's level of fear, uncertainty and doubt (as proxied by the ratio of the Vix index to the 10-yr Treasury yield) have coincided with lows in stock prices. As fears rise, stock prices decline, and vice versa, as the market "climbs walls of worry." I've now labeled the fits of fear/walls of worry, to help with the analysis. The latest bout of fear has centered on the fears surrounding a possible UK exit from the European Union (aka Brexit). As polls and betting markets show the probability of a Brexit declining, markets have breathed a sigh of relief and stock prices have bounced.

If a Brexit spells bad news for the U.K. and the rest of Europe—I'm not convinced it does, but the market thinks it does—it stands to reason that a Brexit would hurt the Eurozone economy more than the U.S. economy, since U.S. exports to the Eurozone are a small fraction (~10%) of our total exports. And as the chart above shows, Eurozone equities have suffered significantly in the past year, whereas U.S. equities are relatively unchanged. In fact, it's not just a Brexit that is weighing on the fortunes of the Eurozone, it's long-term economic stagnation. I note that Eurozone equities have been underperforming their U.S. counterparts for quite a few years: since mid-2010 the S&P 500 is up almost 50% relative to the Euro Stoxx index. This alone suggests that the UK might be better off if unconstrained by EU shackles.

The chart above compares the price of gold to the price of 5-yr TIPS (using the inverse of their real yield as a proxy for their price). Both are go-to investments for those worried about rising inflation, geopolitical risks, and the end-of-the-world-as-we-know-it. Gold is impervious to the elements, and TIPS are not only impervious to inflation, they are the only security that offers a U.S. government-guaranteed real rate of return. Both prices have jumped in the past 5-6 months, no doubt encouraged by Brexit worries, general economic slowdown worries, terrorist attacks, and rising geopolitical concerns. But in the great scheme of things, prices of gold and TIPS are still lower than they were in 2011-2012, during the height of the PIIGS crisis. Things are bad, but not that bad.

The real yield on 5-yr TIPS is not only a measure of the market's inflation general instability concerns. As the chart above shows, real yields tend to follow the trend growth rate of the U.S. economy. When the economy was chugging along at 4-5% rates of growth in the late 1990s, TIPS carried a monster real yield of about 4%. With the economy growing at 4-5% per year, TIPS had to compete by offering a real rate that was somewhat less (because it is guaranteed). Now that the economy has been growing just over 2% per year for the past several years, TIPS real yields are trading at about 0%. You can lock in a zero real rate of return with TIPS, or you can take your chances with an economy that only promises to deliver 2% (which presumably sets a reasonable expectation for real returns on stocks). Not much has changed in this picture of late.

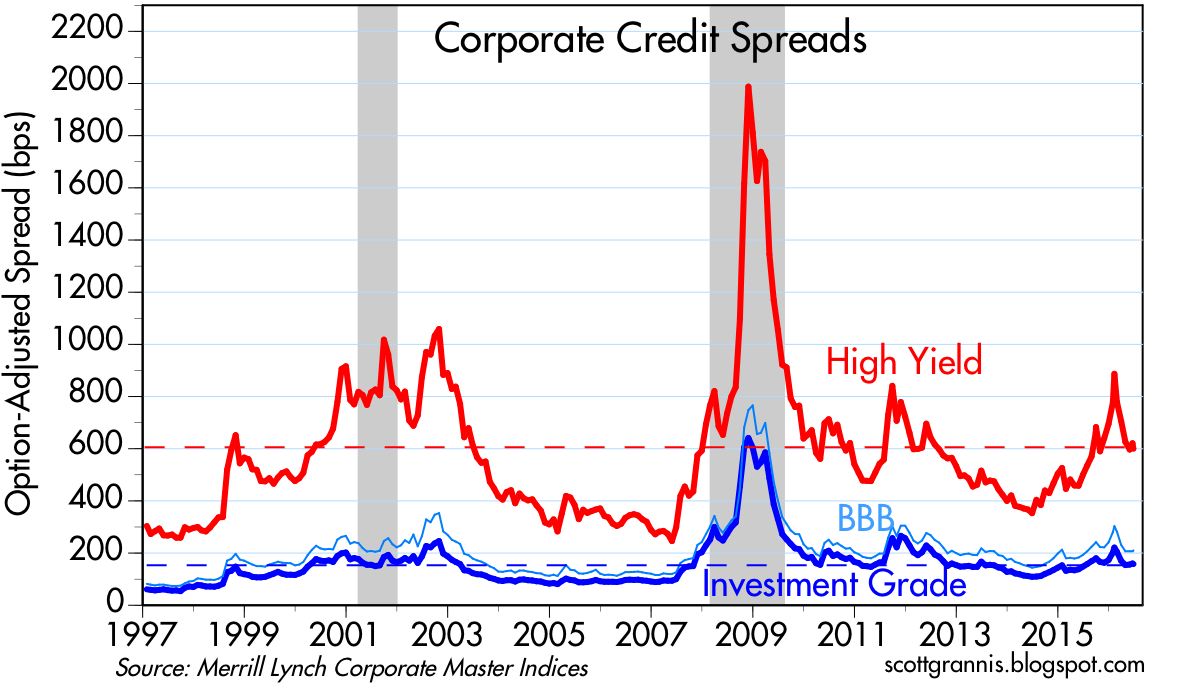

Bouts of fear are also reflected in credit spreads, which hit all-time highs in 2008, and lower highs during the PIIGS crisis and the recent collapse in oil prices. They are still somewhat elevated, which suggests the market is still concerned about a weak economy getting somewhat weaker. But they are far from panic levels. Oil prices are up, oil patch credit risk is way down, and the U.S. economy still appears to be growing, albeit still slowly.

The chart above is one I've showed many times over the past 7-8 years. It compares 2-yr swap spreads to high-yield credit spreads. I think it shows that swap spreads are good leading indicators of credit spreads and the health of the economy. They rose prior to the past two recessions, and declined prior to the start of the past two recoveries. They tend to rise before other credit spreads rise, and they tend to fall in advance of a decline in other spreads.

Throughout the recent oil-price-collapse crisis, swap spreads have remained quite low. I argued several times in the past six months that the message of swap spreads was very encouraging. Low swap spreads are indicative of healthy financial conditions—lots of liquidity and very low systemic risk. Healthy financial markets serve as a shock absorber for the real economy. Functioning and liquid markets facilitate the myriad adjustments that market participants make while coping with changing economic realities. The swap spread market was telling us all along that the crisis in the oil patch was going to be resolved without great calamity, and indeed that looks to have been the case.

Finally, the chart above, which compares U.S. and Eurozone swap spreads. U.S. markets are in somewhat better shape than their Eurozone counterparts, but neither market is pointing to a significant negative event on the horizon. That further suggests that the Brexit fears will eventually pass, and the market will successfully climb one more wall of worry.

11 comments:

Great write up, terrfic charts.

One quip for bald guys out there. "Geopolitical concerns"?

Jeez, I can remember when the Soviets had missiles in Cuba and hinted at using them. Our Joint Chiefs advocated a first strike on Moscow. 1962.

Don't let the federales scaremonger you. The world is far less dangerous today, especially forced Americans, than ever before.

Thanks for these greats posts scott.

Thanks for these greats posts scott.

Scott - possibly a dumb question but do you think swap spreads might also indicate the higher creditworthiness of the banking system due to more capital, Dodd-Frank, etc?

Andy: good point. I would say that everything has helped: QE provided the safe assets and liquidity that the banking system wanted and needed. Higher capital requirements mandated by Dodd Frank have made the banking industry fundamentally safer, but at the cost of less risk-taking on the part of banks, which in turn translates into slower growth in lending and a slower recovery than we might otherwise have seen.

There is no free lunch when it comes to imposing new regulations and restrictions on the banking industry.

Scott, thank you for another great post.

On a micro level, there seem to be walls of worry that AAPL needs to overcome in order to break loose and grow again. I know you've been bullish on AAPL in the past.... do you still like AAPL long term?

Would love to see another post on AAPL since it has come under a lot of scrutiny of late.

Keep up the great work!

Quick take on AAPL: The stock currently trades with a trailing PE of 10.7 and a forward PE of 11.6. If you adjust that PE ratio for Apple's enormous holdings of cash (about $200 billion), most of which is offshore, and you assume that it is all brought back minus a 35% tax rate and paid out to shareholders, then Apple's PE is around 8. There's a simple calculation that gives this value: after tax cash is about 25% of Apple's current market cap of $525 billion, so if you subtract 25% from the current price of $95 and divide by 12mo trailing earnings, you get roughly 8. A PE of 8 is equivalent to an earnings yield of 12.5%, which is huge relative to risk-free alternatives; from that it follows that the market is assuming that future earnings will be significantly less than current earnings. How much less? If earnings fell by 50% and stayed there, Apple's cash-adjusted PE at current prices would be about 16, which is substantially less than the market's average PE of 19+. So you might say that the market is pricing in a 50% drop in earnings. That gives you a flavor for how pessimistic the market is these days. I'm not nearly that pessimistic, which is why I still like Apple.

Full disclosure: I am long AAPL at the time of this writing.

Thank you for the reply.

The general sentiment in silicon valley is that VR is hear to stay and will only get much better with time. It will be mainstream in less than 5 years.

The other big trend that is picking up a head of steam is AI. In the next 5 years or less, the #1 job in America (truck drivers) will disappear in favor of autonomous self driving trucks (same for uber/lyft drivers, taxi drivers, etc.). Last time I looked, there are 1.25 million annual deaths (globally) due to automobile accidents.... AI will vastly reduce this number.

My only concern for AAPL is that they are far behind Google, Facebook, Magic Leap and many other players in VR/MR. They are also far behind Google when it comes to AI. These factors may weigh on AAPLs ability to grow in the long term.

Barring any big changes, I'll likely exit my position when the market finally decides to fairly value AAPL, which I hope happens in the next 4-24 months.

Apple has never been at the vanguard of new technologies. But when they do enter a market, they more often than not do it with great style and ultimately with success. I hope that pattern continues.

And of course the advent of AI will be very disruptive to many industries. Most people view this with dread, but history teaches us that new technology invariably leads to higher living standards for everyone, no matter how hard it seems to imagine that that could be the case. What will all those unemployed truck drivers do? Who could have imagined what all the unemployed farmhands would do with the advent of mechanized farming? The future is hard to imagine in all its fullness, but I'm willing to bet that it will be better than most people fear. If you haven't already, be sure to read Matt Ridley's "The Rational Optimist."

Post a Comment