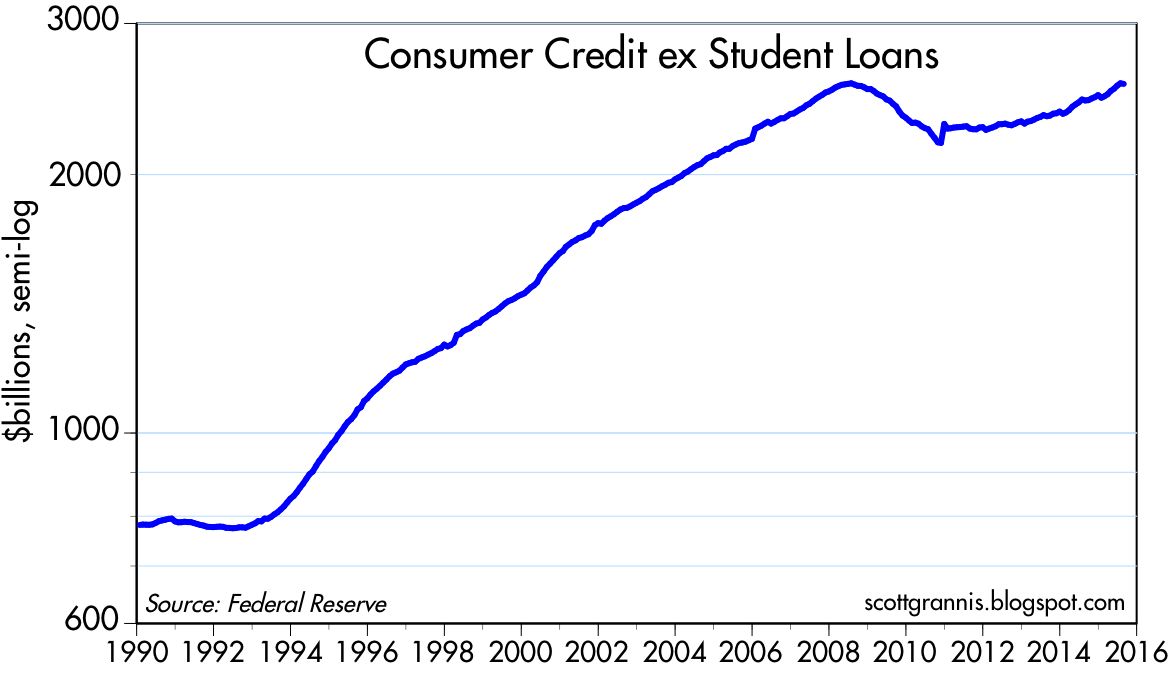

Even as evidence mounts that households have undergone significant deleveraging in recent years, student loans continue to expand at strong double-digit rates (student loans are up almost 14% in the past year). As I wrote three years ago, the higher education bubble continues to inflate. Just as the housing crisis was fueled by government demands that banks make it easier for buyers to get a mortgage (e.g., no down payments, floating interest rates, interest-only mortgages, stated income), now we have the emerging student loan/higher education crisis that is being fueled by government demands that students have easier access to credit to finance their education.

In the chart above, we see that student loans started growing explosively in early 2009, after being essentially unchanged for the previous eight years. All of the increase in student loans since the end of 2008, almost $800 billion, was issued by the federal government, which has now essentially co-opted the entire student lending industry. The government has taken over and the mandate is to increase loans no matter what. Consumers in aggregate are deleveraging, but students are leveraging up, and many in a big way. As a percent of consumer credit, student loans are exploding skywards: up from 5.5% at the end of 2008 to almost 27% today.

This will inevitably end in tears for taxpayers, as well as for the students who have taken on onerous levels of debt. Colleges and universities will also suffer, since federal largesse in the form of a flood of new loans has enabled education costs to reach levels that are way out of line with the rest of the economy. Sooner or later, when the student loan plug is finally pulled, colleges and universities will find themselves forced to undergo the same painful restructuring and cost-cutting that devastated the residential construction sector some years ago. Meanwhile graduates are finding themselves burdened by huge levels of debt that many will not be able to service. Politicians are already greasing the wheels of a taxpayer bailout, rest assured. Debt forgiveness will take many guises, but in the end it will just be more "free stuff" that politicians promise in order to buy votes from the ignorant.

14 comments:

As usual, the full picture is much more nuanced than can be conveyed by pulling national totals.

The growth in student debt is all about the for-profits: http://goo.gl/qe4Gi5

The elephant in the living room is the federal government that agrees to lend almost willy-nilly, without regard for a student's ability to repay the loan. That for-profits allegedly have a poorer track record in producing students able to repay their loans does not absolve the government of its irresponsible lending behavior. This situation will not improve until student loans once again come under the control of the private sector. Those who are on the hook for defaults should be the ones making the lending decisions, not politicians or bureaucrats.

The costs of college are out of hand. What ever happened to spartan facilities and jobs for college students? At many colleges, the cooks and janitors and gardeners used to be college students, and they were glad for the work. I love libraries. But does a college today need a library? Textbooks?

The VA has been effectively funding very dubious "colleges," some which have shut down. That particular market has become a racket.

I agree, get the federal government out of education.

I might be tolerant of specific hard-nosed vocational training, with programs largely designed by the industries that then employ the graduates.

I do wonder why, after all these years, Silicon Valley---which always pleads worker shortages---has not created hard-nosed software programing schools, in which the curriculum is constantly adjusted to industry needs. One to two-year training programs, with tough exit exams. I guess there is no market.

OT--from a newsletter I get:

"Today’s $21 billion auction of new 10-Year Treasury Notes went well; solid demand, the 10-year closed at 2.06%. Interesting change in the foreign buyer profile. Central Banks (especially China) were big buyers in recent years. In recent months, as the commodities plunge hit emerging market currencies hard, many Central Banks are selling treasuries to prop up their home currencies. But foreign private investors have dramatically increased their buying searching for a safe haven. Much attention was paid to the recent 3-Month Treasury auction with a yield of 0%, indicating more safe haven sentiment. Many of these buyers do not want to be holding cash from their home currencies, definitely a risk-off trade. Last week’s jobs report puts the Fed in a further quandary as data is still mixed with some fear that a hike too soon may shock the system, but they are also concerned that the Fed risks losing credibility if they wait too long."

0%?

People are lending money at 0%?

This is not a capital glut?

DATE 5 YR 7 YR 10 YR 20 YR 30 YR

10/01/15 0.24 0.42 0.59 0.99 1.23

10/02/15 0.14 0.33 0.51 0.93 1.18

10/05/15 0.17 0.36 0.56 0.99 1.23

10/06/15 0.12 0.31 0.53 0.97 1.20

10/07/15 0.15 0.33 0.53 0.95 1.19

Wednesday Oct 7, 2015, 4:19 PM

Treasury Real Yield Curve Rates. These rates are commonly referred to as "Real Constant Maturity Treasury" rates, or R-CMTs. Real yields on Treasury Inflation Protected Securities (TIPS) at "constant maturity" are interpolated by the U.S. Treasury from Treasury's daily real yield curve. These real market yields are calculated from composites of secondary market quotations obtained by the Federal Reserve Bank of New York. The real yield values are read from the real yield curve at fixed maturities, currently 5, 7, 10, 20, and 30 years. This method provides a real yield for a 10 year maturity, for example, even if no outstanding security has exactly 10 years remaining to maturity.

---30---

The above is what the Treasury calls "real yields."

http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyield

These seem lower than what others say are the "real interest rates."

http://www.wsj.com/articles/price-tag-of-bernie-sanders-proposals-18-trillion-1442271511

Don’t worry Bernie will cover that! Free college, free healthcare, better infrastructure, expanded social security! Wow, just think!

All kidding aside, the student loan problem will prove to be a large political issue. The true default rate is already hidden by the active promotion of income based repayment (IBR) and pay as you earn (PAYE) repayment programs. 150% of the federal poverty income level, adjusted for family size, is not subject to student loan payments. 15% and 10% (IBR and PAYE) above that amount is subject to payments. Top this off with public service loan forgiveness (PSLF), which allows for governmental forgiveness after 10 years of consecutive payments while working for the government or a nonprofit.

This is the correct sector to focus on in private debt formation. Government provided, guaranteed, and ultimately ending in forgiveness for many. I have read some articles about “helicopter money” to loosen monetary policy. Student loans meet the definition. I would much rather see FICA tax cuts.

Solutions? Start by repealing BAPCPA. This made it nearly impossible to discharge student loans in bankruptcy. It also altered the way derivatives are cleared in bankruptcy by exempting them from the company’s asset freeze. Both of these provisions implemented in 2005 will prove to have long standing implications in the U.S.

An interesting chart would be to show the amount of student loans juxtaposed over the instructor-to-administrator ratio. It's the liberals which the students love so much that are responsible for their massive life choking debt. Poor kids, so stupid.

OECD October 2015 - Outlook of moderating growth in most major economies

08/10/2015 - Composite Leading Indicators (CLIs), designed to anticipate turning points in economic activity relative to trend, show signs of a moderating {slowing} growth outlook in most major economies.

The CLI for the OECD area as a whole points to growth easing {slowing}, with a loss of growth momentum anticipated in the United Kingdom and the United States....and signs of a more moderate easing of growth in Canada and Japan.

In Germany and the Euro area as a whole, stable growth momentum is anticipated while in France and Italy the outlook is for firming growth.

Among the major emerging economies, CLIs continue to point to a loss of growth momentum in China, and weak growth momentum in Brazil and Russia. Firming growth is expected in India.

BOTTOM LINE: Growth is projected to slow in the worlds three largest economies: the USA, China and Japan.

http://www.oecd.org/std/leading-indicators/CLI-Oct15.pdf

http://www.marketwatch.com/story/oecd-growth-in-us-china-japan-to-slow-2015-10-08

I eagerly wait more finance notes and comparisons as requested from the other readers here. I think that even if the students aren't too bothered about the effect of this student loan bubble, the law-setting bodies should be!

Running a spell checker, it points out possible mistakes. Have you noticed the limits of this kind of spell checker? Well, there is a new kind of online software that is a spell checker and more. See more grammar check online free english

[url=http://www.avanse.com/education-loan]Students Loan[/url]

Ask if there's a burglar alarm system (bonus!) and check that the doors are adequately secured – particularly that the main door to the building has secured entry.

Student accommodation in Preston

Thanks for the blog very nice keep going.

sell my macbook prosell my macbook pro

Post a Comment