The big news today was not the 0.2% decline in the the September CPI. It was this:

Some 65 million retired and disabled Americans are about to be hit with a double whammy -- the Social Security Administration announced Thursday there will be no annual cost-of-living benefits increase in 2016 but there may be an increase in Medicare costs.

This happened because the year over year change in the CPI in the 12 months ended September was zero. But the real news is even worse, because inflation next year is very likely to be 2%. Why? Because it's averaged about 2% per year for the past 1, 5, 10 and 13 years, if you exclude energy prices from the calculation. Oil prices have fallen by more than half since mid-2014, and that is the primary factor driving CPI inflation to zero over the past year. Barring another big decline in oil prices—which looks unlikely given the 62% decline in active oil drilling rigs in the U.S. over the past year—the CPI is likely to continue growing at its long-term trend rate next year. If for no other reason than that the Fed wants the CPI to increase by at least 2%.

As the chart above shows, food and energy prices have contributed a tremendous amount of volatility to the CPI over the past decade or so, compared to the more stable "core" CPI.

The chart above plots the CPI ex-energy on a semi-log scale from early 2003 to the present. With the exception of a few years prior to and just after the Great Recession, prices by this measure have increased about 2% every year.

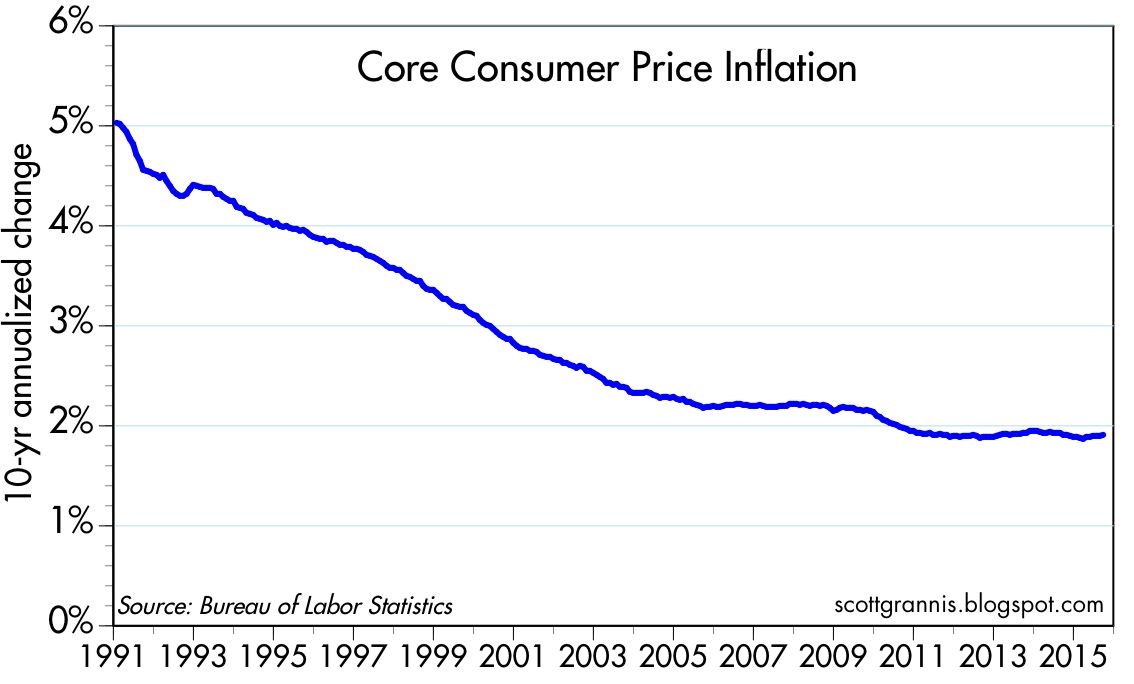

Going back to the core CPI, and calculating its annualized rate of increase over rolling 10-yr periods, we find that by this measure inflation stopped falling several years ago and is now averaging just about 2% a year. It may be premature to say this—especially since it goes strongly against the grain of current inflation expectations—but it's possible that the big secular decline in inflation that began in the early 1980s has run its course.

One reason the CPI is almost surely going to rise next year is the past behavior of housing prices. As the chart above suggests, the BLS' calculation of Owners' Equivalent Rent (which makes up about 25% of the CPI) tends to follow the rise in housing prices (as tracked by the Case Shiller index) with a lag of about one and a half years. The fact that housing prices are up 4-5% over the past year thus suggests that the OER will make a substantial and positive contribution to the overall CPI for most of next year.

So for those who depend on social security and disability payments for the bulk of their incomes—in addition to those who live on the near-zero interest rates on cash—2016 is very likley going to be a tough year, since their spending power is going to decline by about 2%.

Memo to Fed: it looks like you've been doing a pretty good job of targeting 2% inflation. No need to worry about raising rates whenever you feel like it. After all, savers could use some relief.

16 comments:

The Fed could raise Fed fund rates, but that would only lower interest rates on long-term bonds. So which savers would benefit?

The trend to lower interest rates and lower inflation has been going on for 30 years and is evidently global in nature. We now see Europe and Japan deflation or close to it, and now China is trending that way also.

Central banks have been tight for decades and continue to be tight. How else to explain these long-term secular trends?

There now appears to be growing appreciation that a nominal interest rate is not a good indicator of monetary policy.

Like all public organizations, central banks are slow to react to changes in market situations. Central banks have been fighting the last war.

We may be entering an era in which quantitative easing will have to become conventional policy. However there are a lot of good aspects to this, including the possibility of lower tax rates.

As for housing, we will see less expensive housing in the United States when local communities decide to deregulate single family detached housing policies.

When the City of San Clemente, for example, embraces free enterprise in land use, we can expect deflation in housing costs. The problem is, that ain't going to happen.

The CPI thus overstates inflation at least from the monetary perspective.

benjamin, long term bonds go to the beat of their own drummer and most certainly NOT short term rates as set by fed. I suspect what you mean by this is that by raising rates the fed is in a small way trying to stave off inflation and thus long rates may mitigate. that said, consider that long rates are lower now without and "disaster" than they have ever been! no, the long term government bond trades primarily based on perceived future inflation and that is clearly quite low.

"Why does the Fed prefer PCE over CPI? Societe Generale's Aneta Markowska explained in a June 19 research note:

... The official switch from CPI to PCE occurred in 2000 when the FOMC stopped publishing CPI forecasts and began to frame its inflation projections in terms of the PCE price index. This shift, announced by Alan Greenspan during his testimony to Congress, came after extensive analysis done by the Fed. The conclusion was that the PCE has several advantages over the CPI, including (1) the changing composition of spending which is more consistent with actual consumer behavior, (2) the weights, which are based on a more comprehensive measure of expenditure, and (3) the fact that PCE data can be revised to account for newly available information and improved measurement techniques. In that same testimony, Greenspan said that the FOMC “will continue to rely on a variety of aggregate price measures, as well as other information on prices and costs, in assessing the path of inflation.”

As you can see in the chart above, the composition of PCE and CPI are very different. Shelter inflation is a notably smaller component of the PCE index than it is for CPI. Markowska explains:

... the projected divergence is consistent with the historical spread between the two inflation measures which has averaged at 0.5% over the long run. The spread is driven in part by composition effects, with the CPI basket being fixed and the PCE basket allowing for substitution effects which generally favor cheaper goods and services.

The closely linked scope and weight effects also play an important role. Whereas the CPI reflects out-of-pocket expenditures of all urban households, the PCE also includes goods and services purchased on behalf of households. For example, medical care outlays have a much greater weight in the overall PCE basket relative to the CPI index given that it includes premium payments made by the employers and by the government. The PCE also includes the imputed cost of financial services furnished without payment which are not included in the CPI. The expanded share of these two components in the PCE necessarily shrinks the weight of other goods and services (see chart 18 for details). Importantly, the share of housing is just 15% in the PCE vs 31% in the CPI. Since this is one of the key drivers of inflation in our forecast, it also contributes to a widening gap between the two inflation measures."

Are the changes made to the CPI or any other indexes subject to peer reviews?

Are there any papers published to support these changes?

Why are not taxes included in any index? (because they never decline?)

The modifications does not present real life living costs..The FRB is living in

a fantasy world not reflecting true costs of operating a household.

All indexes used by governmental units, understates the real inflation

because it serves their budget requirements.

Just another example of the fox guarding the hen house..

The quote above came from Business Insiders - (2014)

Hear is Mish's take on housing costs used by

governmental units.

http://globaleconomicanalysis.blogspot.com/2015/10/hooray-huge-rent-hikes-coming-how-will.html

Can we all basically admit that, from a monetary policy perspective, we're at the end of the road? Oh, we can still converse about whether or not 2% inflation should be a goal. Or whether one should look at CPI or PCE. Or many other detailed points. But, basically, inflation is not a problem that would be appropriately addressed by rate hikes. Nor does the economy seem particularly prone to improvement based on more QE. Fiscal policy: a lonely nation turns its eyes to you! And on this score, I think it's tough to make the case for optimism, at least for the next 15 months and likely well beyond that.

Every once in a while, Scott will post something that elicits opinions on fiscal policy. I've noticed that every single time this happens, a bunch of prescriptions are offered, none of which have any plausible chance of becoming law in a any meaningful time frame. They turn out to be a laundry list of "shoulds" rather than anything that has a snowball's chance in hell of passing.

I think we continue to slog along with crappy economic growth (but growth) and just-ok credit (which is not the disaster scenario some predict). Animal spirits stay contained, rates stay low, multiples don't change all that much, and earnings growth slogs along somewhat in line with crappy economic growth. Nothing about this will be fun but nor is it a reason to go to bottled water and canned goods.

My eyes remain peeled for signs of optimism and for signs of a credit crack-up. I don't see either one at this point.

Steve-- I mean that a central bank cannot tighten its way to higher long-term interest rates. Milton Friedman said so and he is right. So the Fed tightening now or raising rates would only cause long term rates to go down. People will get less income on their bonds. So what savers do we help by raising short-term rates?

Matthew-- quantitative easing will work. Japan is having success with quantitative easing, and the US had success with quantitative easing. The Fed should have kept on with QE. Japan tried federal deficit spending and it does not seem to work.

A constitutional ban on local property zoning would probably help, but that ain't going to happen.

Lower taxes due to QE - you mean that Fed monetized debt will lower taxes?

I would say the ultimate tax is lost productivity gains - i.e. wealth lost. Doesnt matter how goverment gets its hands on capital - it will for sure be misallocated

matthew hit the nail on the HEAD! with these pinheads that the american voters put into office repeatedly nothing of substance will change.

Matthew: I sympathize with most of what you say. It doesn't look like anything is going to change for the foreseeable future. But my experience has taught me that it is dangerous to extrapolate a continuation of the status quo when it has been in place for a long time and it is not optimal. I think there are seeds of discontent brewing which may bring about positive change next year. Call me an optimist, but I think it still pays to be optimistic.

Terex: Yes, the central bank appears to be able to monetize debt without negative consequence.

I thoroughly concur that the federal government should be reduced in size, with the interim goal at 15% of GDP.

Federal transfer payments are bad enough, but the real waste is federal agency spending.

Scott wrote very wisely: "But my experience has taught me that it is dangerous to extrapolate a continuation of the status quo when it has been in place for a long time,"

Very true, but the next phase of economic activity could go Scott's "optimist" way as it has for 6 years; OR it could go a more "pessimist" way. The US Federal Government is grid locked and that is very unlikely to change because the American voters are about evenly split 50% - 50%.

In any case, the political environment doesn't change the structural issues of the "Greying" of many developed economies: the low growth in working age population of about 0.5% annually the past 3 years; and low productivity the past few years of about 0.5%. When one adds roughly 1.8% inflation in the US, the nominal growth in GDP becomes 2.8% which is the average USA growth in GDP the past few years.

What could possibly change these structural issues in the USA - or for that matter, even worst structural issues in Euroland and Japan?

One must face the reality of QE: low interest rates have lead to over investment in many factories and natural resource projects; and almost ZERO yields for savers, especially the conservative elderly in many societies. And it has resulted in major stress for conservative, long term investors like life insurers; annuities; private and State pensions plans, etc.

Global growth rates and exports have been slowing for 3 -4 years. The World Bank, the Federal Reserve, the IMF and the OECD, etc. continue to lower their estimates of individual country's growth rates and global GDP growth - in spite of central banks "stimulative" efforts. On all major continents the central banks are attempting to stimulate faster economic growth utilizing extraordinary means that have never been used before.

And what is the result??

William-

If QE made interest rates go down, how do you explain the 30 years of falling inflation and interest rates before QE?

http://nreionline.com/multifamily/don-t-expect-multifamily-rents-alone-catalyze-higher-inflation

The link above suggest more deflation ahead, due to softening apartment rents. The CPI minus shelter is very low. The shelter component of the CPI is mystifying, as it includes homeownership and the waving of magic wands to determine what is inflation.

The PCE core minus shelter may be a better indicator of inflation, and it is dead.

The truth is that shelter inflation stems from ubiquitous local land regulation. Every city I know restricts the supply of housing and retail space.

You can't build 40-story condo towers in the City of San Clemente, despite the fact that consumers want 'em, and investors would make good money building them. Free enterprise is not welcome in the City of San Clemente.

What the citizens of San Clemente (and nearly all other cities) want is: 1) To restrict the supply of housing 2) restrict the supply of retail space 3) good economic growth 4) And no inflation.

Got that?

Benjamin that you for pointing out my error. I should have written:

"One must face the reality of zero interest rate policy:"

William--

Some economists are suggesting what do United States really needs is negative interest rates. I believe Switzerland has tried this.

I think there is too much cash in circulation in the United States for negative interest rates to be effective. People will just migrate even more to cash.

Quantitative easing still strikes me as the best policy at this point in time.

The Fed has also not normalized interest on excess reserves. Before, the Fed did not pay interest on reserves, but it has been since 2008.

Real inflation is much higher than 2%, housing costs are thru the roof. This is so counties, states, cities can recoop pension money lost via taxation of the resident. Health care thru the roof, Food costs thru the roof.

The fed is evil personified. They so far have done nothing for Americans and everything for the banking cartel. Pigmen act this way..

Being optimist doesn't mean you need to stick your head in the sand to the issues every american without a saving account (68%) is experiencing. We are being led down a path to no return by men with degrees from Yale or Harvard. The same degrees that led to the 2nd great depression by assuming risk was just a game played on a board.

Quit making excuses for the lousy job the fed, treasury, wall street and government has propped up housing prices so the rich can get their pottervilles...

The risks are still there now 5X as worse

Benjamin - Not sure if you have seen anything about banks not wanting corporate cash, but it is a pretty interesting dilemma.

http://www.wsj.com/articles/big-banks-to-americas-companies-we-dont-want-your-cash-1445161083

Bank fees can essentially take interest rates negative. Seeing this is some smaller personal checking accounts. Fees for individuals without xxxx total amount deposited, without direct deposit, ect. The set interest rates do not necessarily have to be negative in order to create a net negative nominal interest rate environment.

Post a Comment