Over the past month, the growth rate of savings deposits still appears to be slowing, bank lending to businesses is still booming, and the Fed has tapered further its bond purchases. Inflation remains low and the economy is likely recovering the strength it lost to bad winter weather. So far so good, but this is a topic that bears considerable attention, so I offer some further commentary here.

As I've noted before, the Fed's QE bond purchases have consistently failed to deliver on one of their stated purposes, which was to reduce the level of long-term interest rates. (It's this apparent failure which actually bears witness to the success of QE, as I explain here.) As the chart above shows, 10-yr Treasury yields rose significantly during each QE episode (i.e., the price of the 10-yr Treasury fell). Massive purchases of bonds by the Fed not only failed to boost the prices of bonds, they appear to have depressed the price of bonds. Similarly, the Fed's Operation Twist (OT) failed to cause the yield curve to flatten, since 10-yr yields were unchanged after over a year of the Fed buying 10-yr bonds and selling shorter-maturity bonds.

I've explained before that what this shows is that the Fed has no ability to unilaterally affect interest rates with maturities beyond that of a few years. The market is a far more powerful force. I think yields rose during each QE episode because the market saw QE bond purchases as a positive for the outlook for growth. By buying bonds and swapping them for bank reserves, the Fed was satisfying the world's intense demand for safe, short-maturity assets, and by doing so the Fed was avoiding a shortage of safe assets and providing much-needed liquidity to the markets, and this helped facilitate economic growth. Better growth prospects drove yields higher.

Bond yields fell sharply after QE1 and QE2 not because of anything the Fed did or didn't do, but because both the Fed and the market were blindsided by the sudden rise in Eurozone sovereign default risk that occurred during those periods. A big increase in the risk of a Eurozone disaster understandably resulted in a big increase in the demand for dollar liquidity (i.e., a flight to dollar-based quality), at precisely the time the Fed decided to not supply more. Concerns about the prospects for growth drove yields lower.

I think it's significant that 10-yr yields have only declined marginally since the tapering of QE3 started, and swap spreads here and in the Eurozone remain low (see chart above). Looking ahead, it's not unreasonable for the market to expect QE3 to end this year, so the relative stability of 10-yr yields tells us that tapering is not problem and the prospects for growth have not deteriorated despite Fed tapering.

Since the beginning of QE3 in early 2013, the Eurozone has emerged from its recession and eurozone financial markets have stabilized; swap spreads are almost down to normal levels, and the Euro Stoxx index is up over 20%. The countries that appeared on the brink of disaster (Greece, Italy, Spain, Portugal) are now in recovery mode. Things are likely getting a bit better both in the U.S. and in the Eurozone, although boom times are still out on the distant horizon.

As the chart above shows, the growth rate of savings deposits has been declining for the past four years. Since the end of 2013, savings deposits have grown at a 5.1% annualized rate, after growing at an annualized 11.6% rate from the end of 2008 to the end of 2013. In the past six months, however, the growth in savings deposits has been a mere 3.6% annualized. If savings deposits had instead grown at an 11.6% annualized rate, today they would be $270 billion higher than they currently are. Reflecting this decline in the demand for safe assets, gold prices are down over 30% in the past few years.

As the chart above shows, gold prices have fallen in line with a fall in the price of 5-yr TIPS (shown here as a rise in real yields), and that counts as more than a coincidence in my book. 5-yr TIPS are a unique kind of safe asset since 1) they are default-free, 2) don't have much interest rate risk, 3) carry a government-guaranteed real yield, and 4) provide protection from inflation. From 2009 until late 2012, gold and TIPS told us that this recovery was the most risk-averse ever. Since early last year, they've been telling us that risk aversion is being slowly replaced by more confidence.

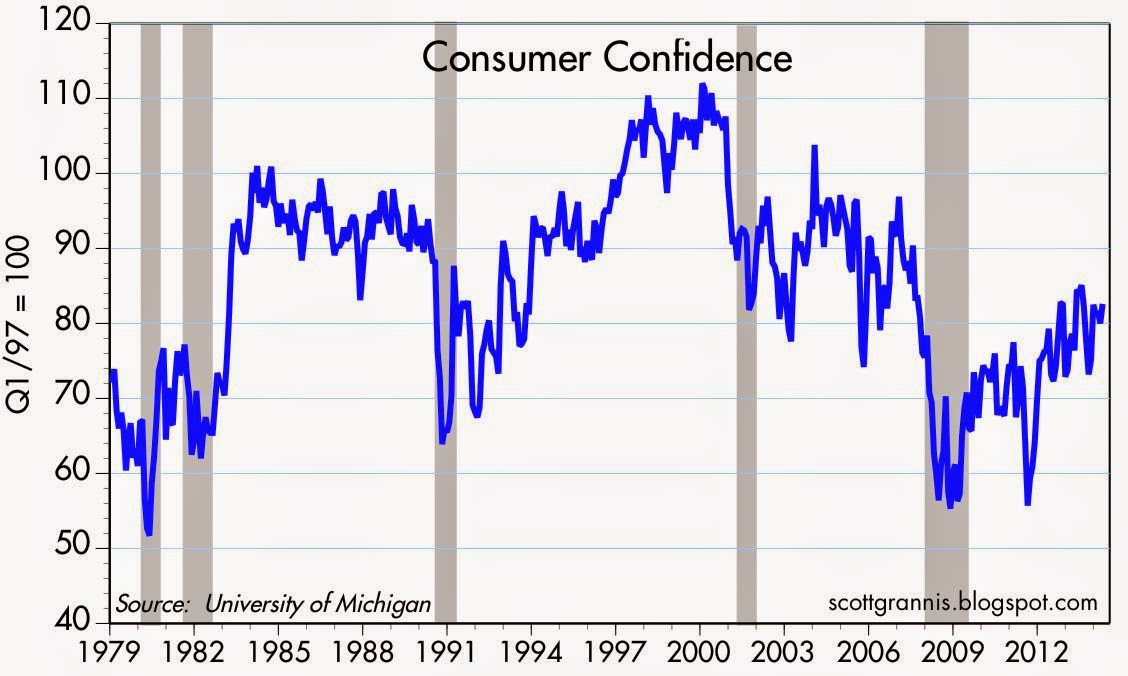

The world is becoming less fearful and that's why the demand for safe-haven assets is declining. This is part of the long healing process that was necessary after the Great Recession and the near-collapse of global financial markets in late 2008. It's a sign that confidence is slowly returning, and it's corroborated by surveys of consumer confidence (see chart above).

The two charts above show the level and the rate of growth of Commercial & Industrial Loans, which are a good proxy for bank lending to small and medium-sized businesses. Beginning around the first part of last January, banks rather suddenly became more willing to lend and/or businesses became more willing to borrow. Since mid-January, C&I Loans are up about $70 billion relative to their trend growth of the past year or so. That's a sign of increasing confidence no matter how you slice it. It's also a reflection of a declining demand for money. Banks have far more reserves than they could ever hope to need (excess reserves currently total $1.92 trillion), but until recently they were apparently quite content to accumulate excess reserves because they wanted to improve the health of their balance sheets in anticipation of more stringent capital requirements, and because they were generally reluctant to lend. That now appears to be changing. An increased willingness to lend reflects banks' reduced willingness to accumulate excess reserves, which are a functional substitute for the gold standard of risk-free money (i.e., T-bills). Similarly, businesses' increased willingness to borrow is a direct reflection of a reduced demand for money, because borrowing is the opposite of owning money.

In just the past several months, the magnitude of the decline in money demand (as reflected in the recent $70 billion surge in C&I Loans and the $270 billion slowdown in savings deposit growth over the past six months) is an order of magnitude larger than the Fed's $30 billion in tapering to date. It's still small potatoes compared to the size of the global economy (over $70 trillion), but it's an important change on the margin that could prove troubling.

This all bears watching because if the demand for money continues to decline, then the Fed will need to increase the pace of its tapering and sooner or later begin to 1) reduce the supply of bank reserves and 2) increase the level of short-term interest rates. If they don't do this in a timely fashion, then we could begin to see inflation move higher.

3 comments:

The world passed through peak prosperity on Thursday April 10, 2014, with the failure of credit in the Eurozone; investors no longer trust that the monetary policies of the ECB or the US Fed will stimulate investment gain.

The dynamos of creditism, corporatism and globalism are winding down as investors are derisking out of debt trades and currency carry trades.

Humanity has passed from the age of credit, which produced prosperity, into the age of debt servitude, where the new normal is austerity.

All fiat investments, whether they be real estate, stocks or bonds, will for ever be going forever lower, as the cost of money, that is the Benchmark Interest Rate, $TNX, will be going higher, from 2.72%, as investors have concluded that the world central banks monetary policies can no longer stimulate investment growth.

On Monday April 21, 2014, Small Cap Nation Investment, IFSM, traded lower as Russia Small Caps, RSXJ, Vietnam, VNM, Singapore, EWSS, Emerging Europe, ESR, and Mexico, EWW, traded lower.

Gold Mining Companies, GDX, Silver Mining Companies, SIL, and Industrial Miners, PICK, traded lower, as Commodities, DBC, led by Agricultural Commodities, RJA, CORN, SOYB, WEAT, JJG, and Spot Gold, $GOLD, traded lower to $1,290.

Gold is in an area of strong resistance. It being both a commodity, and a currency, has been traded lower with the commodity currencies the Australian Dollar, FXA, the Brazilian Real, BZF, as well as the Emerging Market Currencies, CEW.

A portfolio of Inverse Market ETFs could serve as collateral; this might include STPP, XVZ, JGBS, GLD, PPLT, PALL, EUO, YCS, SAGG, DTYS, DNO, as well as HDGE, SBB, SBM, DDG, EFZ, YXI, SZK, SDP, KRS, REK.

The chart of the Gold ETF, GLD, shows that it entered an Elliott Wave 3 of 3 Up in January 2014. Short Side Of Long posts Gold Has Outperformed Other Asset Classes In First Quarter 2014. ETF Daily News posts Phantom Gold Inventories: has the Comex already defaulted?

Some think gold mining stocks are a good investment; yet it’s hard to justify an investment in Gold Miners, such as AEM, with its forward PE of 37. Something more reasonable might be Allied Nevada Gold, ANV, with a forward PE of 24; yet this is quite high for a starting point to build an investment.

One should not be invested in paper gold, such as the Gold ETF, GLD. One should take possession of the genuine article, that is gold bullion, as it will be trading awesomely higher, as in the age of the failure of credit, it and diktat of regional sovereigns, are the only two forms of sustainable economic activity.

New sovereigns for a new age. Under liberalism, the speculative investment community provided seigniorage through money manager capitalism. Under authoritarianism, regional leaders provide seigniorage through the word, will and way of their diktat, a case in point being the Troika’s management of the Greek economy and the terms of assistance to Ireland. Ongoing policies, coming through the singular dynamo of regionalism, will be the basis for trust in diktat money to provide for regional security, stability and sustainability.

Very solid post, per usual, by Scott Grannis.

For now, I would like to see the Fed worry more about prosperity than inflation. A long, long boom is what the USA needs, and if we have 3 percent inflation, that would not concern me.

There have been a large number of structural changes in the USA economy that make it far less inflation-prone than decades back. No unions, lower MTRs, deregulated transportation, finance and telecommunications, the Internet, better retailing, globalization of manufacturing markets.

Show me anybody who has pricing power.

In fact, given the level of competition, and flat unit labor costs, where will inflation come from? Is demand pull inflation a thing of the past, when the supply side is global? I think so, nearly.

How does, say, demand for autos in USA rise so high that global automakers cannot supply the cars? The Big 3 has been replaced by the even Bigger 8 or so.

This is all good news. Corporations have money to invest, lots of labor slack, lots of places to buy inputs.

The Fed should let it rip to the moon.

Post a Comment