Markets appear to have over-reacted to hints that the Fed would taper its QE3 bond purchases sooner than expected. We are still months away from any actual tapering, and at least a year or two away from any meaningful Fed tightening that might threaten the recovery. In the meantime, sensitive and timely indicators show no sign of any deterioration in the economy, and that suggests that risk asset prices are likely to recover.

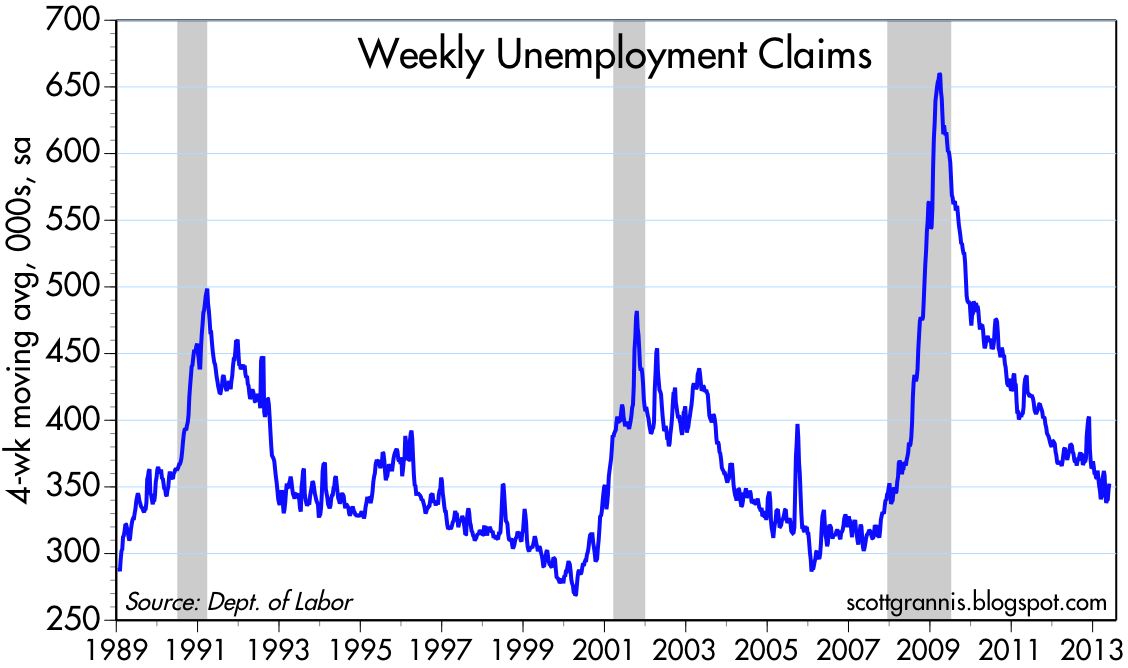

Seasonally adjusted claims, shown in the chart above, are continuing to decline, down almost 9% from a year ago. On a nonseasonally adjusted basis, the actual number of new claims for unemployment last week fell to its lowest post-recession level, 293K, down almost 10% from a year earlier. No sign here of any deterioration in the labor market, and that in turn strongly suggests that the economy is still growing.

Over the past year, the number of people receiving unemployment compensation has dropped by over 1 million, or about 19%. Since the peak in early 2010, the number has declined by 6.9 million. On the margin, about 750,000 people have dropped off the unemployment rolls in just the past three months. These are very significant changes that increase the likelihood that the economy will continue to expand, because a substantial number of people have an increased incentive to find and accept a new job.

Announced corporate layoffs have been low and relatively stable for almost two years. Businesses are not tightening their belts, and that's another good sign that the economy is still growing.

2-year swap spreads are excellent leading indicators of the health of financial markets and the economy. They remain unusually low, which means markets are very liquid and systemic risk is very low. They show absolutely no sign of any distress that might lead to an economic slowdown.

Credit default swap spreads have jumped in the past few weeks, in line with the correction in equities (and particularly those that are sensitive to rising interest rates), but the magnitude of the jump is not nearly big enough to signal a big problem. The level of spreads continues to reflect a market that is cautious and skeptical, but the increase in spreads on the margin is almost insignificant from an historical perspective.

Similarly, the increase in broader measures of credit spreads in recent weeks is almost imperceptible. Recent developments in credit markets reflect caution, not deterioration.

The above chart of 5-yr real yields on TIPS shows the market's most dramatic reaction to the hints of Fed tapering. Real yields have jumped significantly all across the TIPS curve. But they are no higher today that they were at the beginning of last year. What stands out here is not the recent rise in real yields, but the degree to which real yields had fallen earlier this year. That was a clear sign that the market was worried that the prospects for economic growth were dismal. Real yields now reflect much less concern about the health of the economy going forward. Real yields are still orders of magnitude lower than they would be if monetary policy were tight enough to threaten a recession.

As the chart above shows, the rise in real yields is also telling us that inflation expectations have dropped. But expected inflation is still in line with the norms of the past, and there is no sign here of any deflationary threat that we might expect to see if the Fed were indeed expected to become so tight as to threaten the recovery.

The Vix index (an excellent proxy for the the market's fear and uncertainty) has jumped of late, but from an historical perspective this is only a minor tremor.

8 comments:

There wasn't much of a correction.

This latest gyration affirms the importance of the Fed sending a clear signal to markets: It has resolve in its quest for economic growth.

The market is concerned that the Fed will buckle at the slightest hint of inflation. And the Fed has in recent history, including, famously, 2008.

That market uncertainty is exacerbated by undisciplined loose cannons, such as FOMC member Richard Fisher, who launch into sweat-drenched hysterics about inflation every time they are in the public eye.

Inflation right now not even in single digits--it is in decimal points, as in 0.7 percent for last 12 months, PCE.

Let us hope the Fed realizes the 1970s are over, I loved Sonny and Cher too, but time to move on....

I know you fancy yourself a market guru but many have tried and virtually NONE have succeeded at this endeavor. I repeat; you're either an investor or not. Do not try to time stocks.

The latest media narrative is that the recent equity rally is all fed driven. Mr. Grannis' excellent work shows this is not at all the case. Stocks have gained on an improving economy and profits, which real rates confirm. But this false narrative will probably take us through the summer months, until one day rates AND stocks will go up enough for this narrative to be dismissed.

You write We are still months away from any actual tapering, and at least a year or two away from any meaningful Fed tightening that might threaten the recovery.

I respond,the bond vigilantes have already started calling the Interest Rate on The 10 Year US Debt, ^TNX, higher to 2.12%, and have control of the bond marke,t as the 10 30 US Sovereign Debt Yield Curve, $TNX:$TYX, has steepened, as is seen in the Steepner ETF, STPP, steepening.

And you write sensitive and timely indicators show no sign of any deterioration in the economy, and that suggests that risk asset prices are likely to recover.

I respond that risk asset prices are not dependent upon deterioration in the economy but are driven by currency carry trade investment and by toxic credit investment.

On Thursday, June 6, 2013, World Stocks, VT, US Stocks, VTI, and Emerging Market Stocks, EEM, bounced higher, as the US Dollar, $USD, UUP, traded strongly lower, to 81.52, taking Major World Currencies, DBV lower, as the Japanese Yen, continued strongly higher. The Swiss Franc, FXR, the British Pound Sterling, FXB, and the Euro, FXE, rose parbolically higher to new rally highs. Today was a risk on currency carry trade day driving a number of sectors higher; these included, ITB, IBB, IGN, PKB, and PJP. Aggregate Credit, AGG, rose, on higher Junk Bonds, JNK.

Despite today’s stock market rally, the chart of the EUR/JPY, seen in ratio of FXE:FXY, communicates that the direction of the stock market is inexorable down. The significance of today’s stock rally action is that the plunge protection team and currency traders joined in a rally of the Euro, FXE, despite the WSJ report In Europe, angst fills sovereign bond gap.

A day is coming soon, when the currency traders will gain the upper hand and call the Euro, FXE, significantly lower, and the Yen, FXY, higher, resulting in deleveraging investors out of currency carry trade and toxic debt supported stock market investments.

And you write, the increase in broader measures of credit spreads in recent weeks is almost imperceptible; recent developments in credit markets reflect caution, not deterioration.

I respond that in as much as the Interest Rate on the US Ten Year Government Note, ^TNX, has risen to 2.12%, credit died in May of 2013, causing the death of fiat wealth. Debt deflation, that is currency deflation, currency volatility, and unwinding currency carry-trades, have turned Nation investment, EFA, and Small Cap Nation Investment, IFSM, as well as World Stocks, VT, strongly lower.

The failure of the monetary policies of the world central banks means the death of both credit and money as they have been known. Falling currencies and rising interest rates means the fast destruction of wealth and the banking system as it is has been known.

Debt deflation, is now stalking the globe, devouring who ever it may, destroying both the investment value of credit investments but also stocks investments as well. It’s only a matter of time before the national sovereignty of democratic states gives way, and regional alliances form, as forseen by the 300 illuminaries of the Club of Rome in 1968, as organized by the Morgenthau Group, for the purpose of establishing ten regional zones for mutual security, stability, and sustainability.

Governance and moneyness will no longer be exercised rewarding investment choice as it was under Liberalism. Now, under authoritarianism, rule will come from regional statist leaders exercising diktat.

Thank you,Scott. Excellent analysis and very helpful to all investors.

If the market isn't propped up by Fed intervention, then let's remove the QE and see what happens. I think everyone knows what will happen.

Scott: good analysis. It has been apparent for some time that there is inflation roiling in the US economy...and it's in the stock market. Investors are no different than other hogs at the public trough: instinctively they may know in the quietness of their thoughts that QE needs to go but with it they fear goes the trough. With this in mind, the market will be unsettled for a while until the new reality (normal?) set in that QE dole is gone. It's time to man up the old fashioned way.

Post a Comment