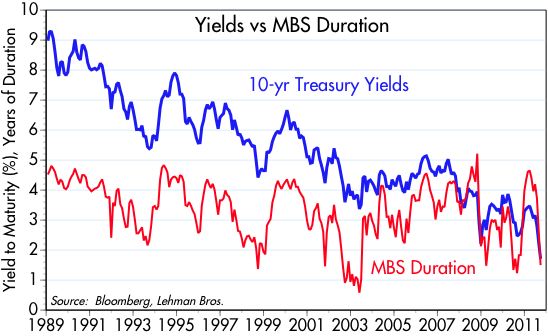

10-yr Treasury yields have never been as low as they are today (1.73% as of this writing). Meanwhile, the effective duration of the MBS market has rarely been lower. The two go hand in hand, since the huge collapse in the duration of MBS (from a high of 4.9 years last April to just 1.5 today, by my estimates) has forced large institutional money managers to buy huge amounts of Treasury notes and bonds in order to keep the duration of their portfolios from collapsing, otherwise they would suffer significant underperformance. Declining MBS duration, in other words, has contributed significantly to the decline in Treasury yields.

The combination today of record-low Treasury yields and almost-record-low MBS duration is like compressing a massive spring: if and when the downward pressure on yields lets up, we will see a massive rebound in yields as the recent process reverses. Managers would be forced to sell massive amounts of Treasury notes and bonds in order to offset the huge increases in MBS duration that will follow any rise in Treasury yields. Thus it is that the mortgage market, which comprises about 28% of the investment grade U.S. bond market, can sometimes be the tail that wags the much larger dog—magnifying greatly the market's underlying volatility during periods of stress. Just a modest nudge from the Fed, in the form of the upcoming Operation Twist, can result—at least temporarily—in a huge decline in yields. And just a whiff of good news could send yields sharply higher. We have seen big reversals before when similar conditions existed (i.e., a big decline in 10-yr yields and a big drop in MBS duration): last Fall, early 2009, the Summer of 2003, and early 1999. The next one could be the mother of all Treasury meltdowns.

The only way that a big increase in yields can be avoided is if the downward pressure on Treasury yields continues. And that can only happen if the economy enters another profound recession, and/or inflation turns negative. Once again we find ourselves on the edge of the same abyss we were staring into at the end of 2008: this market is priced to something akin to the-end-of-the-world-as-we-know-it; nothing less than a catastrophic deterioration from current conditions. No one can rule out a truly worst-case scenario, but to get there requires a whole host of things to go from today's unpleasant to absolutely abysmal. I'm not prepared to bet that the bottom will fall out of everything, so that leaves me bullish compared to where the market is.

8 comments:

Excellent commentary and I hope Scott Grannis is right.

There is a growing school of right-wing conservative, classic economists who contend the Fed must move to "market monetarism" and that is the targeting of nominal GDP levels by the Fed.

Right now, the Fed is seen as floundering, and yet the "do-nothing" policy advocated by some amounts to passive tightening--as we teeter along a recession. The Bank of Japan has tried do-nothing for 20 years with dismal results. Like an 80 percent and ongoing collapse of real estate values. The Nikkei DJ is off 75 percent.

George Gilder warned of the near religious zeal of conservative inflation-fighters, who sometimes forget that prosperity and innovation and growth is the point of the economy, not price stability.

We face such conservatives today, and they will ruin us if they get the upper hand.

The final printing stimulus strategy will be the end game.

"Managers would be forced to sell massive amounts of treasury notes and bonds..."

Where would the money go?

John: Managers can reduce the duration of their Treasury holdings (equivalent to buying or selling Treasuries) in a variety of ways: e.g., sell 10-yr bonds, buy 2-yr bonds; buy 10-yr note or bond futures; enter into swap contracts; or sell Treasuries and buy MBS or corporate bonds.

Personally, I can't imagine putting money into Treasuries that return low single-digit yields...

I assume you are referring strictly to bond managers. As longer term yields rise, (prices fall) I take it they would move the funds back to much shorter maturities.

What I am trying to get at is where is all this money going to find a yield? Not at the short end of the curve. Nothing for them there but price stability. Longer dated bonds would be tanking. They would be facing similar dynamics in corporates.

I suppose most of it would just accept no (or very little) yield. But it seems to me there will be a vast amount of money that will be unhappy with its traditional options. Do you have a feel for how much traditional bond money might be willing to go to riskier assets such as convertible bonds, lower rated bonds, high grade equities, etc.?

Benjamin wrote: "George Gilder warned of the near religious zeal of conservative inflation-fighters..." - and debt fighters, I might add.

I question whether Wall Street titans and S&P 500 executives are huge supporters of inflation-fighting, debt-fighting "conservatives". Throughout their corporate careers they became accustomed to the Federal Reserve / U. S. Treasury "put".

What is seldom mentioned but equally important is the Congressional "put" whereby the Congress attempts (in Keynesian fashion) to act counter to recessions through various stimulus / support programs.

Maybe we are nearing the time when a few Wall Street titans and major corporate executives have a heart-to-heart discussion with Sen. Mitch McConnell, Rep. John Boehner, Sen. Jon Kyl, and Rep. Eric Cantor about the "put" they were expecting.

Post a Comment