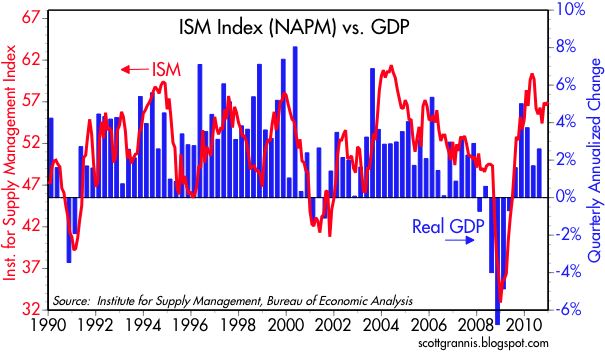

The December ISM manufacturing index came in about as expected, but it continues to point to stronger-than-expected economic growth. As this chart—one of my favorites that I have been using for more than 10 years—suggests, the recent behavior of the ISM index is pointing to GDP growth of 4% or more, leading me to expect that Q4 GDP will be much stronger than the 2.5% reported for Q3.

The Prices Paid component of both ISM indices continues to point to the absence of deflationary pressures and the persistence of inflationary pressures. Some of this could be explained by the rising price of crude oil, as the second chart suggests, with the rest being explained by rising commodity prices, a cheap dollar, a relatively strong global economic backdrop, and accommodative monetary policy.

The Employment component of the ISM index dipped in December, but remains at what is a relatively lofty level. Altogether, the ISM report continues to paint a picture of a relatively strong, ongoing recovery in the manufacturing sector, and this strength is likely to spill over into other sectors of the economy as the year unfolds.

No comments:

Post a Comment