Borrowed Growth "How much of 2011 growth [will be] borrowed from 2012?"

Rosenberg is correct in noting that since the payroll tax cut and bonus depreciation allowance are only temporary measures that expire this December, this is likely to result in some activity being brought forward to this year at the expense of next year (temporary tax cuts are always ineffective). But that doesn't mean the outlook for next year will be bad. There are a lot of things that could happen this year that could improve the long-term outlook (e.g., a de-funding of ObamaCare—or maybe even a partial repeal; a reduction in corporate income taxes; a broadening of the tax base in exchange for lower marginal income tax rates; meaningful reductions in federal spending; and a general shift to more growth-favorable fiscal policies). Just a few of those changes, coupled with the positive feedback of the ongoing forces of recovery and economic adjustment taking place already, could overwhelm (positively) the "borrowed growth" problem. In the meantime, and as I have been noting here in many posts, there are many signs that the economy is continuing to improve.

Higher Energy Prices "If oil breaks above $100 and gasoline prices approach $3.50/gallon then expect the consumer to sputter. Every penny at the pumps drains $1.5 billion out of household cash flow."

Higher oil prices are not necessarily a significant drain on the U.S. economy, because oil producing countries can't spend their windfalls immediately on consumption goods—most of the extra money we spend on oil gets recycled back into the U.S. economy by oil producers in the form of investments. Paying an extra dollar a gallon for gas does not result in that dollar disappearing down a black hole. The way higher oil prices do hurt our economy is by making economic activity prohibitively expensive. Intolerably high energy costs can result in shuttered factories, cancelled projects and investments, and workers who have to turn down jobs because it becomes too expensive to commute. So the real issue here is whether gasoline at $3.50 or even $4 a gallon is going to result in a significant change in consumer or corporate behavior. I doubt it.

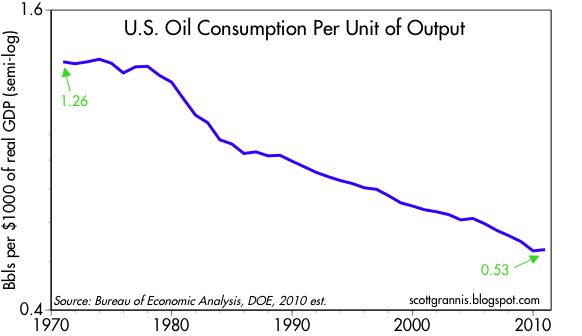

It's true, of course, that in real terms, oil prices today are a bit higher than they were in the early 1980s, but even then historically high energy prices failed to prevent the economic boom which began in 1983. I note also that thanks to more efficient technology and an impressive increase in overall energy efficiency, the U.S. economy today requires less than half as much energy as it did 30 years ago to produce a unit of output. The combination of these developments means that energy today consumes less than 6% of consumer spending, compared to 9% in the early 1980s. Energy is simply much less important today. As a result I think gas prices would probably have to rise to $4.50 or $5/gallon before energy became expensive enough to materially slow the U.S. economy.

Spending Cuts "The GOP-led House is pressing for $100 billion of spending cuts for this year. If enacted ... this could cause GDP estimates to be trimmed."

It is amazing to me that so many economists and commenters automatically accept the proposition that a cutback in federal, state, and local budgets will hurt the economy. It apparently never occurs to anyone to challenge that assumption, even though everyone worries so much about the rising deficits that result from higher spending. Yet if it were true that less spending is bad for the economy, then the $1 trillion of extra spending last year should have sent the economy through the roof. But of course it didn't, and there is no evidence to suggest that the "stimulus" did anything at all to help the economy, especially since it consisted primarily of transfer payments and inefficient spending projects.

Simple logic says that transfer payments (taking money from A and giving it to B) cannot create growth, because they don't increase aggregate demand or supply, and they create perverse incentives (i.e., rewarding people who don't work and penalizing those who do). The public sector is notorious for spending money less efficiently than the private sector, and any money spent by the government must either be taxed away or borrowed from the private sector, which then has less money to spend on things that could be more productive.

Indeed, there are good reasons to believe the stimulus spending probably hurt the economy, since it a) drained significant resources from the more efficient private sector, b) spent those resources wastefully and inefficiently, and c) created real fears of a surge in future tax burdens, thus discouraging private sector investment. If fiscal "stimulus spending" is unproductive and probably even bad for the economy, logic drives you to the conclusion that fiscal cutbacks ought to be a good thing. Bring them on, please!

Obama Might Get Re-elected "Obama just enhanced his 2012 re-election chances by appointing Daley as his chief of staff. Either he is really going to move to the center, or he is trying to cement the next election."

If, under the likely pro-growth guidance of Daley, Obama moves to the right by enough to improve the economy's prospects, then I would have no problem accepting his re-election. The biggest problem we have faced over the past two years is Obama's woeful lack of understanding of how free markets work, and his almost total lack of appreciation for the entrepreneur and the power of incentives. He's been about as anti-growth as anyone could have possibly imagined. If he can overcome those deficiencies and promote growth-oriented policies as a result, then he would deserve re-election and the nation likely would breathe a great sigh of relief.

Improving Jobs Market "Everyone believes that a better employment picture will brighten the stock market’s prospects even more but in fact the opposite will happen as margins get squeezed by rising labour costs."

For the past two years, unit labor costs have been declining, and this has likely contributed to stronger corporate profits. Unit labor costs typically rise over the course of an economic recovery cycle, but we are still in the very early stages of the growth cycle. It could take a long time before unit labor costs rise by enough to squeeze corporate profits. Meanwhile, wages typically lag inflation, and until the swollen ranks of the unemployed are thinned meaningfully—a process that could take several years—it will be difficult for many wages to rise significantly. Plus, corporate profits today are at all time highs—there is plenty of room to absorb higher labor costs. In any event, this is a problem for the future, not a problem for this year or even next year.

The major impact of quantitative easing to date has been to erase the specter of deflation that was haunting markets, and that is clear from the 100 bps increase in forward inflation expectations embedded in TIPS prices. Beyond that, it has done little or nothing to stimulate growth, and little or nothing to boost the supply of money in the economy or the amount of new borrowing. Instead, it has created an additional source of uncertainty for markets that worry about the prospect of higher inflation and the lack of clarity surrounding the Fed's endgame. It has helped keep the dollar weak, and has likely contributed to driving gold and non-energy commodity prices to new highs.

No QE3 "I am hearing that the Fed is moving further away from entertaining the notion of a QE3 program in the second half of the year. [The second quarter is when] the concern list will likely start to grow; lagged impact of China tightening shows through, big European refinancings, signs of no more QE, and the debt-ceiling issue hitting its peak."

The major impact of quantitative easing to date has been to erase the specter of deflation that was haunting markets, and that is clear from the 100 bps increase in forward inflation expectations embedded in TIPS prices. Beyond that, it has done little or nothing to stimulate growth, and little or nothing to boost the supply of money in the economy or the amount of new borrowing. Instead, it has created an additional source of uncertainty for markets that worry about the prospect of higher inflation and the lack of clarity surrounding the Fed's endgame. It has helped keep the dollar weak, and has likely contributed to driving gold and non-energy commodity prices to new highs.

Canceling or failing to renew QE2 later this year may rekindle deflation concerns, but those could easily be offset by a stronger economy. But no QE3 would most likely be welcomed by financial markets since that would reduce inflation anxieties. Already there are many, in addition to myself, that are arguing that QE2 is no longer necessary.

As for China, the degree of monetary tightening that has been implemented so far is relatively puny and poses little or no threat to Chinese growth. Since China remains pegged to the dollar, the biggest factor influencing monetary policy conditions in China is Federal Reserve policy, and it remains extremely accommodative. China's revaluation of the yuan to date has been relatively tiny, and not nearly enough to offset the general weakness of the dollar or the Fed's super-accommodative policy stance.

As for European debt problems, the market has had plenty of time to understand and price in the likely outcome of sovereign debt restructurings (e.g., by driving down the price of Greek debt). Meanwhile, the Euro and the European stock markets show no sign of any impending catastrophe despite the growing likelihood of default. We've seen huge sovereign debt defaults and restructurings many times in the past (Argentina comes to mind) without there being any meaningful disruption to global growth. The sub-prime mortgage crisis of 2008 was a very different animal, since at its core were many thousands of securities, worth many trillions of dollars, and backed by tens of millions of individual properties that were extremely difficult for the market to understand, value and trade. That is not the case with the handful of countries that are high on the likely-to-default list today.

As for the federal government's debt ceiling, the federal deficit is clearly a very big problem since it is symptomatic of out-of-control spending and an unprecedented growth of the public sector which ultimately threatens the health of the private sector. It must be addressed somehow; not addressing it at all would be the worst possible outcome. Cutting spending to lower the deficit is not a problem for me (see above), but raising taxes in an attempt to lower the deficit would be. In that regard, the November elections sent a very clear mandate to Washington to cut spending and not raise taxes. I would be shocked and very disturbed if the new Congress were to ignore that message.

8 comments:

I appreciate you addressing divergent views.

addendum: I regularly read Rosenberg's thoughtful views although with so many accessible viewpoints over the Internet it's hard to choose a dance partner!

Your two charts on oil consumption per Unit of output and energies share of personal consumption actually prove that the output per unit of oil for consumers has no relation to cost.

The unit of output has increased significantly while the cost as a % of income for consumers has barely budged in 40 years.

Since our economy is 70% consumer based I would say the average person has suffered significantly all along the way. On the other hand, your average large corporation tightly linked to the banks and hence the Fed are doing quite well.

Isn't that what we are witnessing in reality too?

I personally believe you underestimated the last time oil hit a peak and will probably do the same again. We are in a weaker position and IMHO we do not need to hit $140/barrel to put the brakes on growth again.

Rosenberg a long long time ago

said you should never marry your forecasts

....over the last couple of years

he has chosen to wear a wedding dress....

What is remarkable about the USA's dramatic increase in the efficient use of oil is that most of the increase occurred at a time of cheap oil--but even with mild incentives, the private-sector just gets better and better at everything it does (in stark contrast to the public sector--think Post Office, USDA or Pentagon).

A high price regime will result in incredible private-sector reductions in the use of oil.

The new Chevy Volt is a marvel. 40 miles on plugged in power, then another 400 miles at 40+ mpg.

At $6 a gallon, Americans will buy Volts. The Peak Oil doomsters never heard of the price signal, or the incredible innovations found in the private sector.

BTW-

Just an idea here.

Okay, John Taylro gushed about Japan's use of QE. And, when Japan ceased QE, they sank back down into perma-recession, and deflation.

Is it possible that Japan must sustain QE operations to maintain prosperity?

Why would the USA be so different?

Well written and balanced set of views. I would add that we did see a self-correcting force in energy prices at $140/bbl because when gasoline in the US hit $4 miles driven dropped for the first time in a long time.

In aggregate the demand for energy and oil may never go down but our efficiency always gets better. Higher prices just accelerate the trend. I don't think it results in more than a short adjustment which allows the markets to re-sync.

Post a Comment