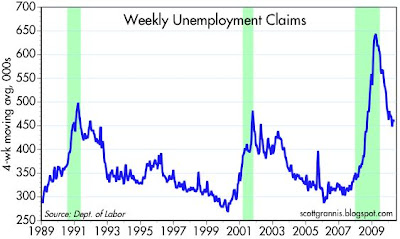

There's nothing here to suggest any deterioration in the employment picture. The rate of decline in claims has slowed in recent months, but this is not unusual for this phase of the business cycle, as I think the chart shows.

Does it really matter if your analysis about Greece is technically right if traders simply decide it's a new global financial crisis and sell everything? What if all these countries are really bankrupt?

They are NOT all bankrupt. Germany is as solvent as anybody. Except maybe Switzerland. Swedwen and Norway are fine as are most others, despite what you might hear from the various chicken littles.

The ECB has been waiting for the politicos to get their acts together and then they are going to act. All this talk about the Euro going down the toilet is BS. The bears use it as an excuse to cram prices down so they can buy cheap. I have seen this over and over again. Panic the weak holders and buy low. And lower. And lower again. In '98 it was the Russian default. In '84 it was Mexico. In '01 it was Argentina. Why do you think Warren Buffet is so successful? He LOVES it when the crowd is scared out of their minds. He is BUYING. You will never get the low tick. But if you buy when the 'public' is frightened, and KNOW what you own, you increase your odds of success immensely.

Few can do this. But those who can and do, do very well. I have seen this movie many times. It always ends the same.

It is no different than buying distressed commercial real estate. Owners are overextended and HAVE to sell. The buyer waits, and waits, and waits some more, then he comes in and bids on HIS terms. In the stock market it happens faster and is more unpredictable on the timing. But bargains can be had if you know in advance what you want and an approximate price you are willing to pay. All the Euro BS is simply the catalyst that freightens the weak holders out (I know because I have BEEN one of those before..more than once). You yourself had the spirit the other day when you wanted to buy BP after the fall. I said 'no, not for me'. But it still may have been a good deal for someone who knew the company well and was a longer term investor. "Know what you own" and find a time when you can buy cheap is a strategy employed by many many investment champions. Its very hard and I'm not saying I am immune to the the fears - I have posted before that I was hiding under my desk in a fetal position in March of '09 when we were crashing (AGAIN) - but I was buying and pukeing over and over the whole way down. No one knows more than me how hard it can be but the best buys I made were the ones that hurt the most when I bought. The harder it is to buy, the better the deal you get. It almost ALWAYS goes lower after you buy but in time it rebounds and then rebounds more and more. My American Express purchase in March of '09 was one of my all time best buys.....but I only bought a little... I was too scared. But I still have it and will for a long time.

This has gone on longer than I wanted it to. I know its cheap conversation, but hey. I LIKE you guys.

Marginal human capital became unemployed during the recent down turn by surviving firms. Firms that did not survive discharged marginal as well as core human capital.

The surviving firms can be categorized as core survivors and marginal survivors. That is, there are companies doing very well indicated by record earnings. Other firms are still struggling e.g. commercial real estate, telecom, etc..

The surviving firms find their remaining core human capital to have skyrocketing productivity rates as demand increases on the margin.

Several items worth noting:

(1) the firm would rather employ current remaining core human capital for additional hours due to the average work week having been below 40 hours for an extended period of time,

(2) when the work week approaches 40 hours, the firm offers and the human capital accepts overtime,

(3) the firm is facing so much uncertainty from current economic policy or lack there of economic policy that the firm fears expanding employment. The remaining current core human capital at the firm accepts the overtime as the less than 40 hour work week which has persisted for some time gives the human capital the opportunity to make up lost ground in the form of overtime wages,

(4) if the firm must increase its pool of human capital due to sustained demand, the firm has a pool of unemployed core human capital available to hire from firms that did not survive the downturn. Hence the firm selects the unemployed core human capital available in the labor pool,

(5) the new expanded human capital (being once displaced core human capital from non-surviving firms) is then offered over time, as well, if the demand dictates, going back through the scenario in #3 above, causing expanded employment to be ever so slow as overtime is perceived as more valuable than expanded employment by the firm,

(6) meanwhile, unemployed marginal human capital of surviving and non-surviving firms remains idle. This marginal human capital remains unemployed for extended periods. The extended period of unemployment can cause the marginal human capital to become even more marginal in nature due to job skill becoming out of date,

(7) other firms faced with unionized work forces are forced into rehiring marginal human capital. The least marginal first to the most marginal last. These firms have less of an ability to seek core human capital readily available in the labor pool. The re-hiring of marginal human capital then affects productivity rates vs. the productivity rate that would have been available if the firm was free to select readily available core human capital. Hence the future hiring rate is hampered (decreases at an increasing rate) by marginal productivity of the re-hired marginal human capital.

I am sure Scott will be blogging on this shortly but the jobs number was IMO quite good. The uptick in the rate to 9.9% is being reported as more optimistic workers entering the workforce.

I made a post yesterday alluding to ECB action when the politicos had passed their respective authorizations.

I have read this AM of a rumor of a multi HUNDRED BILLION Euro loan to various european commercial banks by the ECB. The term is 1% for one year. I repeat this is a rumor but it sounds like something the ECB would do.

I reiterate that IMO the crisis is manageable in the short term. The Euro should weaken further but for now the currency is fine - no collapse like many bears are saying.

I added small positions to my XLK, XLF, and TEVA this AM. I may well be early. I frequently am. Fear is always impossible to predict but I am seeing good values in high quality names.

BTW, no way our Fed raises our rates into this panic. A rate hike may be off the table for this year.

12 comments:

Everything is trending the right way--except for the Dow in recent days. Ouch.

I sure hope Greece is not a reflection in a distant mirror--the USA in 20 years, when we face the same debt wall.

Because governments around the world have on-boarded all the risk.

That doesn't mean the risk magically disappeared.

It is time to sharpen the old pencil and look to add or establish long positions. I am more bullish than I have been in months. Some I am looking at,

Home Depot HD

Altria MO

Intel INTC

BHP Billiton BHP

Teva Pharmceutical TEVA

Spyder Financial XLF

Spyder Technology XLK

Just some thoughts.

Scott,

Does it really matter if your analysis about Greece is technically right if traders simply decide it's a new global financial crisis and sell everything? What if all these countries are really bankrupt?

Bill,

They are NOT all bankrupt. Germany is as solvent as anybody. Except maybe Switzerland. Swedwen and Norway are fine as are most others, despite what you might hear from the various chicken littles.

The ECB has been waiting for the politicos to get their acts together and then they are going to act. All this talk about the Euro going down the toilet is BS. The bears use it as an excuse to cram prices down so they can buy cheap. I have seen this over and over again. Panic the weak holders and buy low. And lower. And lower again. In '98 it was the Russian default. In '84 it was Mexico. In '01 it was Argentina. Why do you think Warren Buffet is so successful? He LOVES it when the crowd is scared out of their minds. He is BUYING. You will never get the low tick. But if you buy when the 'public' is frightened, and KNOW what you own, you increase your odds of success immensely.

Few can do this. But those who can and do, do very well. I have seen this movie many times. It always ends the same.

John-

I admire your nerve. I suspect you are right.

You where French Fries originated from?

Greece.

Benj,

It is no different than buying distressed commercial real estate. Owners are overextended and HAVE to sell. The buyer waits, and waits, and waits some more, then he comes in and bids on HIS terms. In the stock market it happens faster and is more unpredictable on the timing. But bargains can be had if you know in advance what you want and an approximate price you are willing to pay. All the Euro BS is simply the catalyst that freightens the weak holders out (I know because I have BEEN one of those before..more than once). You yourself had the spirit the other day when you wanted to buy BP after the fall. I said 'no, not for me'. But it still may have been a good deal for someone who knew the company well and was a longer term investor. "Know what you own" and find a time when you can buy cheap is a strategy employed by many many investment champions. Its very hard and I'm not saying I am immune to the the fears - I have posted before that I was hiding under my desk in a fetal position in March of '09 when we were crashing (AGAIN) - but I was buying and pukeing over and over the whole way down. No one knows more than me how hard it can be but the best buys I made were the ones that hurt the most when I bought. The harder it is to buy, the better the deal you get. It almost ALWAYS goes lower after you buy but in time it rebounds and then rebounds more and more. My American Express purchase in March of '09 was one of my all time best buys.....but I only bought a little... I was too scared. But I still have it and will for a long time.

This has gone on longer than I wanted it to. I know its cheap conversation, but hey. I LIKE you guys.

Nite, Ya'll

Marginal human capital became unemployed during the recent down turn by surviving firms. Firms that did not survive discharged marginal as well as core human capital.

The surviving firms can be categorized as core survivors and marginal survivors. That is, there are companies doing very well indicated by record earnings. Other firms are still struggling e.g. commercial real estate, telecom, etc..

The surviving firms find their remaining core human capital to have skyrocketing productivity rates as demand increases on the margin.

Several items worth noting:

(1) the firm would rather employ current remaining core human capital for additional hours due to the average work week having been below 40 hours for an extended period of time,

(2) when the work week approaches 40 hours, the firm offers and the human capital accepts overtime,

(3) the firm is facing so much uncertainty from current economic policy or lack there of economic policy that the firm fears expanding employment. The remaining current core human capital at the firm accepts the overtime as the less than 40 hour work week which has persisted for some time gives the human capital the opportunity to make up lost ground in the form of overtime wages,

(4) if the firm must increase its pool of human capital due to sustained demand, the firm has a pool of unemployed core human capital available to hire from firms that did not survive the downturn. Hence the firm selects the unemployed core human capital available in the labor pool,

(5) the new expanded human capital (being once displaced core human capital from non-surviving firms) is then offered over time, as well, if the demand dictates, going back through the scenario in #3 above, causing expanded employment to be ever so slow as overtime is perceived as more valuable than expanded employment by the firm,

(6) meanwhile, unemployed marginal human capital of surviving and non-surviving firms remains idle. This marginal human capital remains unemployed for extended periods. The extended period of unemployment can cause the marginal human capital to become even more marginal in nature due to job skill becoming out of date,

(7) other firms faced with unionized work forces are forced into rehiring marginal human capital. The least marginal first to the most marginal last. These firms have less of an ability to seek core human capital readily available in the labor pool. The re-hiring of marginal human capital then affects productivity rates vs. the productivity rate that would have been available if the firm was free to select readily available core human capital. Hence the future hiring rate is hampered (decreases at an increasing rate) by marginal productivity of the re-hired marginal human capital.

Expect unemployment claims to tick higher in the next few weeks, lots of margin calls made today.

I am sure Scott will be blogging on this shortly but the jobs number was IMO quite good. The uptick in the rate to 9.9% is being reported as more optimistic workers entering the workforce.

I made a post yesterday alluding to ECB action when the politicos had passed their respective authorizations.

I have read this AM of a rumor of a multi HUNDRED BILLION Euro loan to various european commercial banks by the ECB. The term is 1% for one year. I repeat this is a rumor but it sounds like something the ECB would do.

I reiterate that IMO the crisis is manageable in the short term. The Euro should weaken further but for now the currency is fine - no collapse like many bears are saying.

I added small positions to my XLK, XLF, and TEVA this AM. I may well be early. I frequently am. Fear is always impossible to predict but I am seeing good values in high quality names.

BTW, no way our Fed raises our rates into this panic. A rate hike may be off the table for this year.

Post a Comment