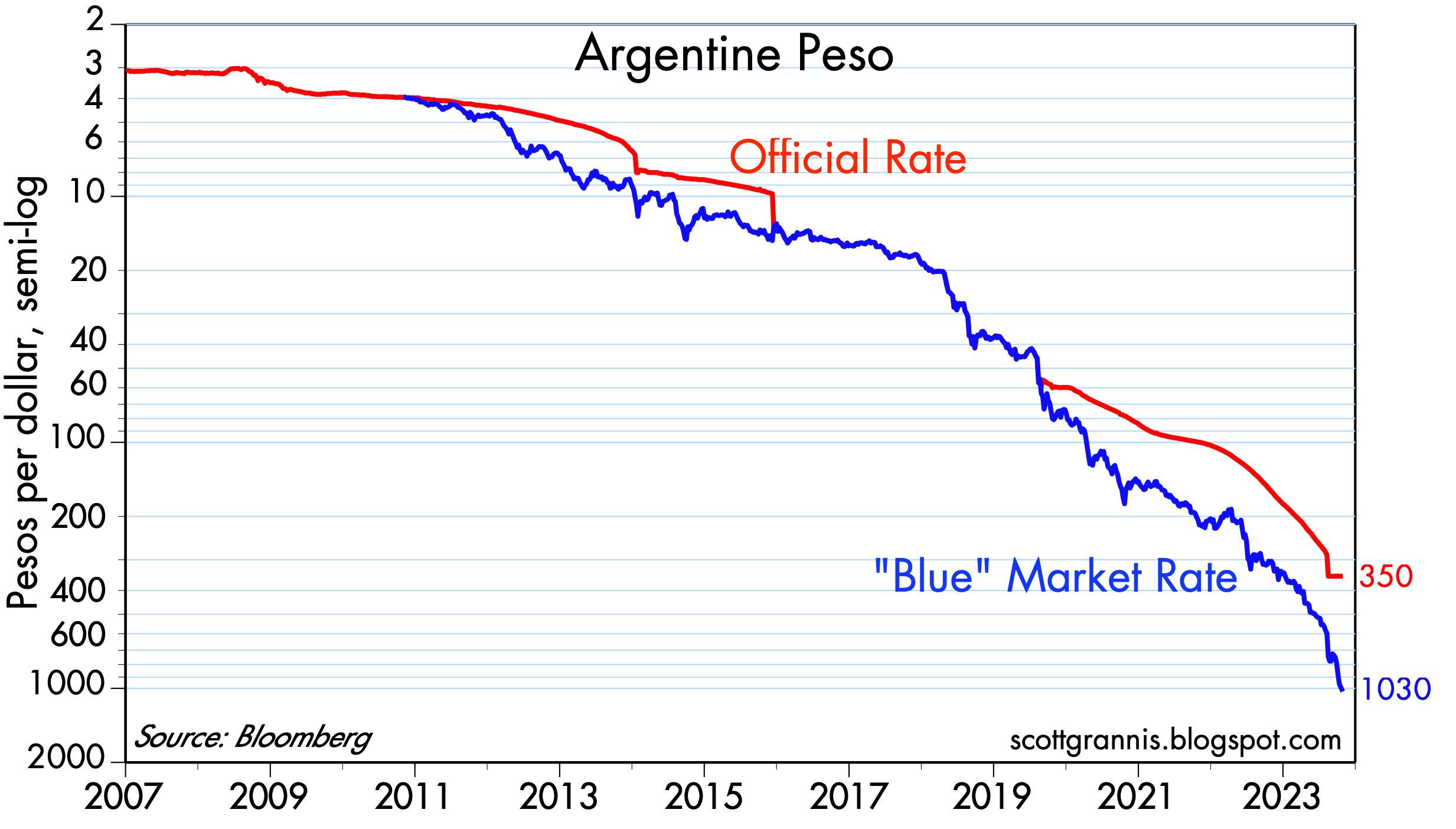

I've been an observer of the Argentine economy ever since I first went there in 1970 to visit my soon-to-become wife. So I am compelled to make this brief post as Argentina's currency passes a key marker: today, Argentines must now come up with 1000 pesos to buy just one dollar. Actually, if Argentina had never taken multiple zeros off its currency several times since 1916, when the exchange rate was 2 pesos per dollar, today it would take 10,000,000,000,000,000 (ten quadrillion) of those original pesos to buy a dollar!

The spark behind the latest peso plunge is Sunday's presidential election. The front-runner, Javier Milei, promises to ditch the peso and dollarize the economy. Which, in my opinion, is the only sensible thing to do, though it might prove tricky to implement. The Argentine government has been resorting to the printing presses to finance its profligate spending for far too long. People know that every day you hold a 2,000 peso note (the largest note in circulation!) in your pocket you are losing money at the rate of 150-200% per year—i.e., the current rate of inflaton. So the demand for pesos has plunged and the demand for dollars has soared. No wonder Argentines are demanding radical change—this has gone on for far too long.

The lesson in this for the U.S. is that our government seems to have abandoned any concern over deficit spending. The budget deficit for the just-finished fiscal year was about $1.700,000,000,000, which is over 6% of GDP. It only exceeded that level during WW II, the 2008-09 Great Recession and its aftermath, and the 2020-22 Covid shutdowns. Today it's sky-high despite the fact that the economy is relatively healthy. Federal debt is now about 94% of GDP, and annual interest payments on that debt are about $1 trillion and rising. We were flirting with Argentine-style inflation a few years ago, when the M2 money supply increased by $6 trillion (40%) in less than two years, thanks to $6 trillion of Covid-related deficit spending.

Chart #1

11 comments:

“ Today, auditors told Congress as much as *$2.5 trillion* of the $5 trillion the US spent on COVID relief went to China and its allies through fraud.

That’s enough to fund the entire Chinese military for 8 years. Keep that in mind when you hear how great our COVID response was.”

Although I do agree the Covid response by US and around the world was a cluster, I doubt anyone objectively believes the take that it went to China, Ai. No, it went straight into American’s pockets, and spending it the past two years like drunk sailors is why we’ve had such high inflation until it started coming back down 2nd half of this year.

Oh how these conspiracy theorists love to believe anything they read. 50% of the covid money going to China? C'mon now. Why stop there... I just heard it was 84.3%. Watch this thread be the one that starts conspiracy theorists believing this new percentage.

Thank you, Scott, I have some Argentinian family members and do hope they all get a new start.

Any current thoughts on yields?

Scott, long long time follower and your macro insights have been an excellent dampener for what at times seems like doom and gloom in the markets and my portfolio. On a a side note, we are leaving Mendoza tonight after three weeks in Argentina, spanning BA, Bariloche, Mendoza and places in between. I took your advice on the Western Union transfer and on Oct 1, the Blue Dollar rate was 867. We discovered you can just walk into WU with a fresh Franklin and we have been getting exchange rates from 980 to 1010. After many many conversations with the locals, we hope they do something. It appears when talking with middle aged Argentinians, they seem to favor Patricia Bullrich, yet every single “younger” person, I’d say 30, seems to be on the Millae train. Must be those Pork Chop sideburns. Thanks for your work and the inputs from the brain trust.

My cousin is editor for one of the largest and most respected newspapers in Argentina. A lot of uncertainty … and trepidation about Milei. What surprises me most is the nervousness I sense. You’d think after a century of upheaval there would be a glimmer of hope that radical change (of the right type) MIGHT be good. But that’s not what I sense.

Meanwhile back in the US, CPI has increased to 3.7% over 3 consecutive months after dropping to 3%. Furthermore underlying inflation measures have reaccelerated.

Roy, re current thoughts on yields: my read of the tea leaves suggests that the Fed is finally on the sidelines, so that source of rising yields has dried up. What we are left with, however, are global uncertainties (i.e., wars) which put everyone on edge. I continue to believe that inflation pressures have abated significantly; with inflation at 2% or less, the current level of yields is generous. For that matter, real yields of 2.5% on 5-yr TIPS are quite attractive. It's not often you get government-guaranteed real yields that high. TIPS are thus not only attractive for their real yields, but also for their ability to hedge against rising inflation and as a way to profit from an unexpected economic slump (because economic weakness would elicit Fed easing, which would show up as falling real yields and thus capital gains on TIPS holdings).

Mark: our friends and family members in Argentina tell me the same thing. Older people prefer Bullrich (she has the right ideas but not Milei's radical solutions) while younger people love Milei. Those supporting Massa are addicted to Peronist perks and handouts. This election will be one for the history books.

ShlepRock: thanks for the WU info—I didn't know that they would exchange Franklins!

Verily, balance the federal budget.

OK, no go on that. The two major political parties are not on board.

I hate to say it: But should the Fed reduce...or add to its balance sheet?

And stop paying interest on bank reserves?

In other words, some moderate inflation, and also debt relief via Fed bond buying might be the best of bad options.

If you are holding your breath for either party to balance the budget...

Post a Comment