... contrary to what you are hearing in the press, which loves to sensationalize things.

There is abundant evidence that inflation pressures are cooling: Non-energy commodity prices are soft (see my last post for lots of charts). Oil is down over 25% in the past four months. The dollar is very strong. Inflation expectations are relatively low and stable (averaging about 2.6% for the past 2 ½ months). Housing prices and new mortgage applications are falling because mortgage rates have doubled so far this year (this means Fed rate hikes are getting lots of traction). Rents are still on the rise, but they are a lagging indicator (rents rise about a year after prices rise, so they will likely begin to stabilize about 6-9 months from now, because prices started falling a few months ago).

Yes, on a year over year basis, it looks like consumer price inflation is still on the rise. But on a 6-mo. annualized basis, which is best for picking up changes on the margin, inflation is falling.

Above all, I can't emphasize enough that this inflation flare-up was not caused by a Fed policy error: it was caused by the federal government's attempt to soften the blow of Covid lockdowns with massive, deficit-financed transfer payments that inflated the money supply. That mistake ended over a year ago, and M2 money supply growth has since decelerated significantly. So the fundamental reason for our current inflation has long since begun to fade in importance.

I've been saying for months now that inflation pressures have peaked, and I still think that's the case. But I've also said that inflation would remain uncomfortably high, probably through year-end, because of all the inflation "in the pipeline" which takes awhile to work through the economy. So we need to be patient.

What this means is that the Fed is not going to have to tighten much more than it already has. A 75 bps hike at next week's FOMC meeting might be enough. That in turn implies that the market is overly-concerned about the downside risks to the economy. This is no time to panic. Are you listening, Chairman Powell?

Chart #1

Chart #1 is an update of a chart I featured some months ago. It is critically important because it shows that the huge increase in the M2 money supply coincided exactly with a huge increase in the federal budget deficit, which in turn was caused by multiple trillions of dollars of Covid-related transfer payments. This is no longer happening.

Chart #2

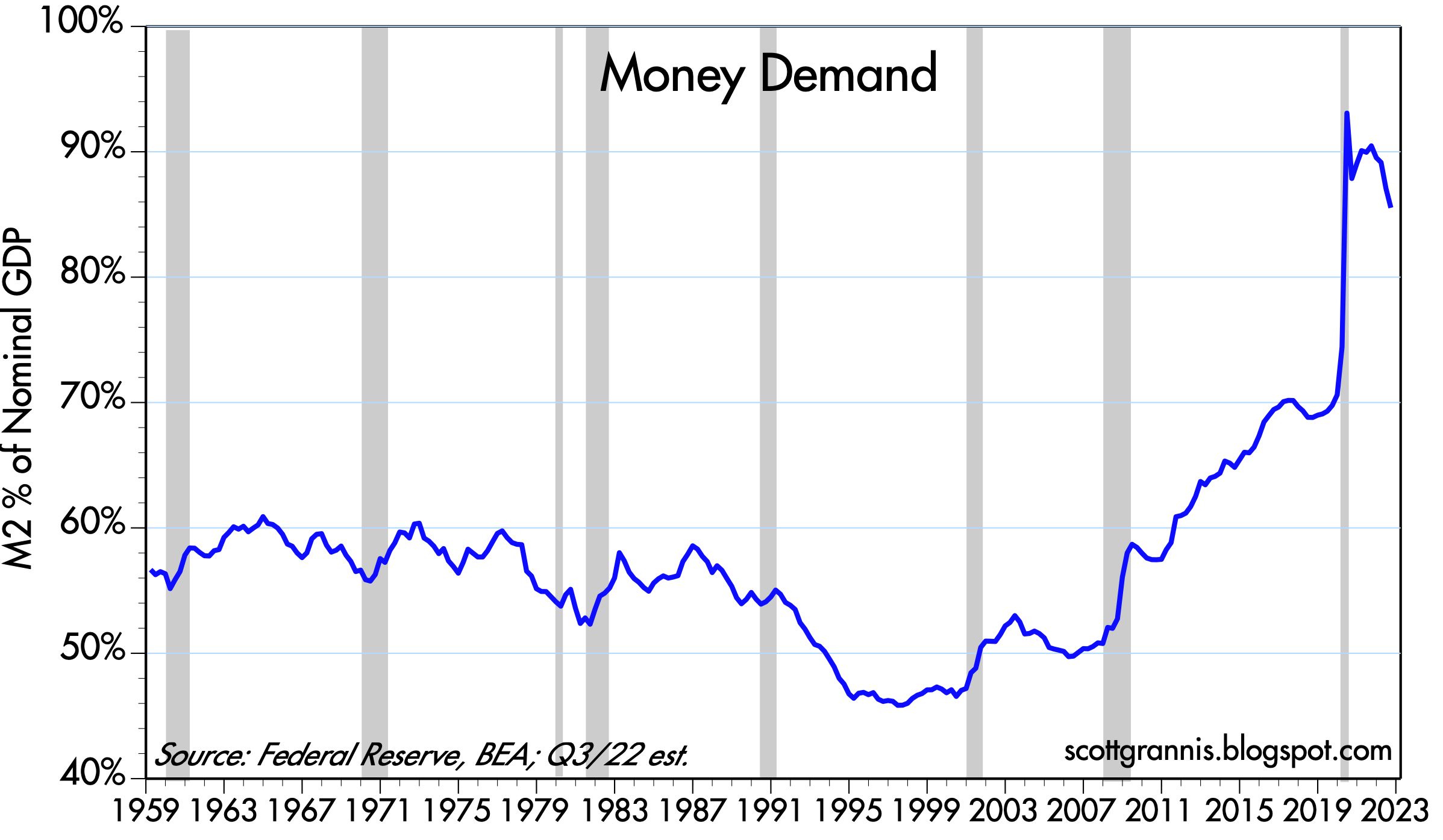

As Chart #2 shows, the problem all this extra money created (inflation) is resolving itself as people spend down their extra (unwanted) money balances. Crushing the economy with tight money now is not the solution. What the Fed needs to do is to simply raise rates by enough to slow the decline in the demand for money. They have already done that, as evidenced by all the market prices that are softening everywhere. Higher interest rates work directly to increase the demand for money (and by inference to decrease the demand for borrowed money). This is the way monetary policy works in an era like today, which began in late 2009 when the Fed decided to pay interest on bank reserves. Before, the Fed had to raise interest rates indirectly by creating a scarcity of bank reserves, and while that worked to increase the demand for money it also created a shortage of liquidity, which can have many collateral and damaging effects in the financial markets.

If money balances (represented in the chart by the ratio of M2 to nominal GDP) don't decline dramatically, the economy can gradually absorb extra money as inflation declines moderately. And along the way, sudden attacks of panic like we saw yesterday work to increase the demand for money, thus minimizing the inflationary potential of extra M2.

Chart #3

Chart #3 compares the 6-mo. annualized change in the CPI vs the 6-mo. annualized change in the Core CPI (ex-food and energy) through last month. By this measure, inflation in both series has peaked.

Chart #4

Chart #4 compares the 6-mo annualized change in the CPI and the ex-energy version of the CPI. Energy prices are by far the most volatile component of the CPI, so using this version helps see through the noise. Again, by either measure inflation looks to have peaked a few months ago.

Chart #5

Chart #5 shows the 6-mo. annualized change in the Producer Price Index vs the Core version of the same. Here again it looks like inflation has peaked. This is significant, because producer prices capture inflation earlier in the pipeline than the CPI. The same story is playing out in the commodity markets, where prices have been declining for months; sooner or later those declines will be passed through to the consumer in the form of more stable and possibly lower prices.

Chart #6

Chart #6 shows the level of real and nominal 5-yr Treasury yields and the difference between the two, which is the bond market's expectation for what the CPI will average over the next 5 years. I note also that the blue line (the real yield on 5-yr TIPS, currently about 1%) is a proxy for the average inflation-adjusted level of the Fed funds rate over the next 5 years. We haven't seen such a high level for a long time. Real yields were much higher in the late 1990s and through much of the 2000s, but that was because the economy was a lot stronger than it is today—a sustained, high level of real yields requires a sustained, high level of real growth. It's tough to see real yields moving much higher than they are today given all the headwinds the economy currently faces: rising tax and regulatory burdens, expensive energy, geopolitical turmoil, and uncomfortably high inflation.

Of course, if the Fed were to aggressively tighten by pushing real yields to, say 2%, then that would likely cause a recession. Recall that all recessions in the past 50 years or so have been preceded by very high real interest rates which were the direct result of Fed tightening actions. Very high real yields accompanied by an inverted yield curve and very high credit spreads are the basic ingredients for a recession. Today we only have one of those ingredients present: an inverted yield curve. That's why I'm reluctant to say that the economy is in a recession.

Chart #7

Meanwhile, 2-yr Swap Spreads remain my go-to guide for how much the economy is suffering as a result of stresses in the financial markets. As Chart #7 shows, these spreads are somewhat elevated, but not nearly as much as we have seen in past episodes of great financial and economic stress. Note how swap spreads tend to rise in advance of recessions and in advance of recoveries; they are great leading indicators. In a "normal" world, you would expect to see swap spreads range between 10 and 30 bps. (See my swap spread primer for more background.)

19 comments:

Excellent analysis, as always. But Scott what makes you think the Fed will stop with just one more rate hike of 75bps? Powell has been very clear that there will be additional rate hikes in coming months. The risk to the economy and the stock market of a Fed policy error is very high.

all goal seeking charts, analysis and cheerleading. pangloss is back in the saddle full time.

Scott - thank you for your insight.

During previous Fed hiking cycles, has the Fed ever stopped raising short-term rates while they remain below the rate of inflation? My concern is that the Fed will continue to hike even as inflation recedes, and probably won't stop until well after inflation (the economy) is crushed.

I think I agree with Scott Grannis on this one, which may not provide any comfort to Grannis, but the ways of the world are mysterious.

My guess is we are near "one (more)and done" with the Fed.

The US and globe has shot itself in the foot with the C19 response, and in some ways the Fed perhaps groped along about as well as could be expected. I think they overdid accommodation, but hindsight is perfect. Other reserve banks, in Australia, Europe and India, seem to have been behind the curve as well.

I am still not sure why the QE hoard has to be sold. I see little effect on inflation from the bond sale, but a large re-leveraging of taxpayers.

A side thought: Europe is discussing a buyer's cartel for natural gas.

I wonder why, in all these years of suffering from repeated OPEC-induced oil crunches, the consuming nations did not form an oil-buyer's cartel.

Buyers cartel for energy- not sure how that would work, but for the US, such cartels would not be necessary if the government regulations would allow the market to work. There is plenty of energy available in the ground for the US.

My guess on the Fed, rates, recession, GDP, etc. They will "over shoot", "pivot", and cause something like a mild recession. The stock market may have a big problem during all of that, e.g. S&P bottom around 3000.

The Fed doesn't have an easy job. People forget about the time lag, so their target is always moving, and during rate changing parts of the cycles, the target is moving very fast.

Good luck to all.

Inflation is broad based. Demand is outstripping supply. The surge in the money stock is unparalleled in U.S. history. AD is incalculable. Not only is the roc in money flows historic, but at the same time, so is money demand. So, stagflation will be with us for a long time.

Larry Summers doesn’t know what secular stagnation is. It is not an imbalance between savings and investments. The increase in the supply of loanable funds was driven by the FED's QE – in direct response to the impoundment of savings in the payment’s system (decrease in the transaction's velocity of funds).

I.e., an increase in bank-held savings shrinks gDp. It’s stock vs. flow (as predicted by Dr. Leland J. Pritchard, Ph.D. Economics Chicago 1933). See: “Should Commercial banks accept savings deposits?” Conference on Savings and Residential Financing 1961 Proceedings, United States Savings and loan league, Chicago, 1961, 42, 43.

Scott - I think you are underestimating your ability to predict the 30% of the CPI which is housing/shelter. Averages shouldn't always inform our modeling. Housing unit have been grossly underbuilt since about 2010 and Millenials are at the household formation peak for the next 4 years, and immigration is out of control. People will be able to afford less but they will still need more housing, proper building is still not happening and so your prediction of housing slowing down in 12 months is probably true BUT not to the extent of not still rising appreciably. As single-family and multi-family boots on the ground see first hand. The demographics and housing stock on hand does NOT support an average peak in housing costs. We might have peaked but thinking inflation is headed to 2% anytime in the next 24 months is laughable to me. Great if I'm totally wrong, but I'd gentleman wager anyone willing to over under 4% over the next 5 years. Also energy is out of control and made illegal (hydrocarbons & nuclear) so this energy crisis will continue at least at a higher price and for longer than folks at modeling. I loved Smead's comparison of Big oil to Big Tobacco in the 80's.

The U.S. dollar is in a self-reinforcing upward spiral. Export countries are selling Treasuries to defend their exchange rates, adding to supply, and the E-$ is contracting, removing demand.

inflation would be much worse if the dollar remained at a stable price. so inflation, especially in the oil markets is vastly understated.

mkt goes to 3400 next. we'll reassess after that. fed continues to raise through year end because raising rates is about the slowest method for attacking inflation that was caused intentionally be govt's that crushed supply chains, inflation will persist far longer than most pundits expect imo.

great data!

If you want to know how to stop inflation, look no further than Bernanke. Bankrupt-u-Bernanke drained required reserves for 29 contiguous months.

The 2-year rate-of-change, RoC in M*Vt (which the FED can control – i.e., the RoC in N-gDp), peaked in the 2nd qtr. of 2006 @ 12%. Bernanke let it fall to 8% by the 4th qtr. of 2007 (or by 33%). N-gDp fell to 6% in the 3rd qtr. of 2008 (another 25%). N-gDp then plummeted to a -2% in the 2nd qtr. of 2009 (another – 133%). That’s what created the cry, epitomized by Scott Sumner, for targeting N-gDp.

Lending by the banks is inflationary. Lending by the nonbanks is noninflationary, other things equal.

The correct response to stagflation is the 1966 Interest Rate Adjustment Act. “while the aggregate of time and demand deposits continued to increase after July, the proportion of time to demand deposits diminished. Whereas time deposits were 105 percent of demand deposits in July, by the end of the year, the proportion had fallen to 98 percent. These were all desirable developments.” – L.J.P.

I.e., you drain the money stock, while increasing the transaction’s velocity of funds.

I am interested in views, commentary, and charts regarding the de-dollarization movement being led by the BRICS alliance -- any help much appreciated.

Scott, I am confused. You say "this inflation flare-up was not caused by a Fed policy error: it was caused by the federal government's attempt to soften the blow of Covid".

This seems just wrong. The Fed financed the government's spending by buying the treasuries. The Fed is supposed to be independent, i.e. not do necessarily what the government wants. The Fed chose to help the government by financing this debt. It is their responsibility then. I don't understand.

Richard

go substack please... blogger doesn't send notifications anymore...

livermore: Is there an easy way to transfer this blog to substack?

Post a Comment